CFA Level II: Derivatives - Pricing and Valuation of Swaps -Part I (of 15)

ฝัง

- เผยแพร่เมื่อ 13 ต.ค. 2016

- FinTree website link: www.fintreeindia.com

FB Page link : / fin. .

We love what we do, and we make awesome video lectures for CFA and FRM exams. Our Video Lectures are comprehensive, easy to understand and most importantly, fun to study with!

This Video lecture was recorded by our popular trainer for CFA, Mr. Utkarsh Jain, during one of his live CFA Level II Classes in Pune (India).

#CFA #FinTree

Probably one of the best videos I've come across for swap pricing. Covers from the basics. Trust me , even people working in the industry for years do not understand how to arrive at a swap Rate and swap price from the basics.

Thank you again!

Thank you. This man broke down the concept beautifully. Bless you!

I remember starting on the swaps desk at First Chicago (now J.P. Morgan) in 1991 and a letter was sent to me, Simon Rogers, on the S.W.A.P.S desk. Someone thought it stood for something, like Special Weapons And Products (!). It only means you are "swapping" cash flows. Always draw them out to make sure you are using the correct side of the bid/offer spread.

You were born to be a teacher!!! Thank you so much for breaking it down like I was learning how to write ABC

Sir, I appreciate the clarity of concepts and way to explain. It's really nice. Keep it up.

Thank you again Mr. Utkarsh Jain, You have a gift for teaching!

You turn complicated concepts into simple/logical flow for students.

This demonstrate your mastery of knowledge! you are amazing.

Awesome Teaching! I love the way you explain concepts and formulas. It is very clear and easy to understand even you have some accent. You gave me an inspiration that I can also become a good speaker even I have an accent! Thanks a lot!

Thank you so much! You're absolutely amazing at explaining concepts that would've been difficult :)

Thanks.. the concept got easy after your explanation. Please post more videos.

Detailed, Simple, explained in a way it becomes intuitive - Amazing explanation Utkarsh.

Bohot badiya sirji ❤…It clears all my doubt regarding SWAP

this was amazing!!

Best video on IRS valuation on TH-cam 😃

You are such a great teacher , your explanations are so graphic and clear, congratulations and a lot of thanx to u!!. . Please post more videos so we can learn well about derivatives.

Superb Explanation. Thank you.

Thank you so much for this explanation

Excellent

Excellent video!

Very intuitive, well done!

Fintree converges to real life propulsion on time value of money.

Duration impacts could have been added in this, that how portfolio duration will shorten / lengthen in above case and how these swaps can be used to change portfolio duration! Awesome teaching skills.. Kudos

Now it's easy sir........

Superb explannation!!

Hi.. Lectures are very good. But one computational error was committed. When different yields are present at year 1,2,3 &4, while taking PVF with yield rates of 10%,11%, 12% and 18% in the lecture for Year 2 1/1.11^2 was taken instead of [1/1.10] x [1/1.11^2] and similar errors gone in the computation for years 3 & 4. Approximate swap fixed rate (SFR) would be closer to the arithmetic mean of the floating rates ie [10+11+12+18]/4 ie 12.75% and not 16.4%. Except the above error, rest all superb... I enjoyed the session.

Super! amazinnng!!!! thanks alottttt

You are such a great teacher,thanks for sharing this concept. You make the harder one so easy.

Thank you so much

Great video , where is the other videos in this series?

Which software do you use for your blackboard?

13:30 How are we determining value of bond? Through discounting of cash flows or something else. Please clarify

Where are the other parts of the video please

Please, Please, Please elaborate when you use terms like “YTM” etc and formulas.

Please remember we are novice and don’t have to watch these videos if we are experts.

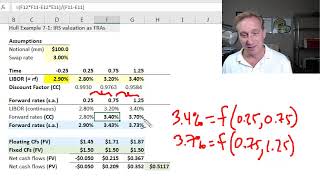

In thé CFA curriculum they use different computation for the discount factors (DF) when computing the swap fixed rate in fixed income vs derivatives. In fixed income they use thé same Logic as describe here but in Derivatives they use 1 / (1 + DAYS/360). So if we compute the 2nd year DF its 1 / (1+720/360) and not 1 / (1+ x)^2. What is the logic ?

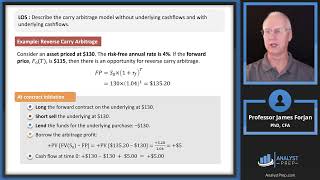

See what you are saying is a complete arbitrage,the total after the total lead time over the arbitrage has been calc. Thus we obtain the most coveted inversere which is more then the ARB percentage is low and vice versa.

what are those spot rates that you have taken for 4 years.

I have the same question

How to value floating coupon bond

how you get the spot rates?

spot rates we get it from market?

Watching this in 2024,

Only where i could find swap pricing equation (rfix) formula derivation.

If an interviewer asks you “how do you price an IRS?” and you answer with the solution presented in this video, the interviewer will laugh and tells you “that’s what you learn in the book, no one prices swap that way since 2008”. Industry standards use dual curve bootstrapping, if you don’t know what it is, don’t even hope for a quant job on a fixed income desk.

Yes you are right.

But he is teaching for the CFA program.

He has to follow the curriculum and teach it in a way so that questions can be answered correctly.

I guess first principles are necessary at the foundation level.