3 years after also there are no such playlists related to time series that match to your level as far as i found. I think that itself makes this playlist most valuable. thank you so much. love to see more playlists from you.

I have never in my life seen such a good teacher before. When he says some weird shit he explains what it is and why it’s important / why we need it. Thanks for these vids

These are great videos. Keep it up! This is very helpful for many graduate students. Can you do another one discussing the differences between the DCC-GARCH, CCC-GARCH, and VCC-GARCH?

agreed.. when I was in ECON grad school... GARCH was our final exam... (the trick is taking a 2nd regression on the error terms themselves)..Adv Econometrics 4....this video (and your effortless explanations) reminds me of what a beautiful art form this level of mathematics is...well done, sir

This video is so helpful I understood the basics in just 10:24 minutes. Although I was reading about it for the past 2 weeks and was still confused. Thank you for making this video.

Another question, just to make it clear: you said that ARCH(1) model retrives bursty volatility data. However, this only happens due to the specification of ARCH(1), ritght? An ARCH(p) model with, lets say, p=5, would be as capable as an GARCH(p,q) model to describe "volatility clusters", even though such ARCH(5) model could be very hard to estimate its parameters, correct?

You're the BEST! I passed my stochastic models exam and it included a very long exercise on which we had to analyze and comment the fitting of a model to a time series. Your videos helped me so much in understanding the differences between the models etc. I'll never thank you enough!

Top notch videos! I have one query if u could please explain. What is the difference between squared errors of lagged series and variance of lagged series in GARCH.

Ananswered question - what is E (errors) is it from ARMA model errors (for instance it is in CFA institute book, level 2 2014 p. 494, we hahe to model ARMA, get residuals from model and then create ARCH)? Variance - is that variance from time series values or errors?

Thanks so much for your videos.you have a very easy and concise way to explain these complex models. I am immensely grateful with you because these videos have finally helped me understand this topic! :D

This playlist is helping me so much to prepare for a possible future interview on forecasting. This provides so much conceptual clarity. Thanks a lot. Had a small question, just as ARCH explains a bursty time series while GARCH adds an additional element to the ‘burstyness’ that once it bursts, it stays there for a while. Is there a similar graphical analogy for AR and ARMA model?

So thankful. I have a question. If we want to explain the relationship between GARCH(1,2) and a ARMA model, why does it bring me back to an ARMA(2,2) and not a ARMA(1,2)? I'd have a Alpha2*Et-2 that is the second autoregressive coefficient.

Great and compact video! It would be great if you could make a video about a multivariate Monte Carlo Simulation. I havent found any useful videos explaining (why we do) the Cholesky Decomp ect...

Thanks for the video, but still confused. I watched your ARCH model, and it looks like the Y we modeled is the residuals (actual movie tickets sold - predicted movie tickets sold), but here it seems the a_i that the ARCH and GARCH are modeling refers to the original values (i.e. # movie tickets sold)?

Checking back the ARCH model video, there is an inconsistency about the ARCH model. The formula is different. As it is hard to type a formula here, can you have a look?

That's what I noticed, too! He mentioned in the arch video that the model was on the error but here he said the value of the time series itself? I'm confused

Does it backtest well? Are you actually trying predict the future volatility level or the direction if it? On a somewhat unrelated note: how do you determine the right timeframes for long term volatility?

Hi!, Could you please clarify a few things about GARCH? : Many tutorials and books use GARCH and ARCH on the innovations/u(t)/error of the time series and not on the time series itself. However you are modelling GARCH on the time series itself. I'm very confused and would love to get this cleared by you

Were these books written by idiots? ... I experienced same confusion!!! In CFA book (level 2) we have to use ARMA model to find errors fo ARCH process. But in some books I also find that i have to square surplusses of time series itself!!!

I thought the ARCH(1) was supposed to predict the volatility of today based on volatility of yesterday. But in this lesson, your ARCH(1) equestion now predicts the time series value of today based on yesterday value.

Great videos, learned so much! thank you Is your ice cream example not a poor example for GARCH? If there is a period of high ice cream sales, then volatility will jump from low season to high season, but then drop down again as the sales are consistently high... until it jumps again down to low season . Rather than having a consistent period of high volatility.

Sir, this video was very helpful, your time series talk videos are very easy to understand and great it helped me alot. And can you please create a short video on GARCH- M model.

Thank you for the great explanation. I want to ask, does it correct that the ARCH model resembles more of an autoregression (AR) than a moving average (MA)? I would really appreciate it if you could answer my question. Thank you in advance

@@sissic2565 Hey Xixi, I think I may have figured it out. The ARCH version he made is universally true, but he makes the assumption that the mean of the error is 0 and the standard deviation is 1. This leads to us replacing it with returns!

![F.HERO Ft. JSPKK x ลำไย ไหทองคำ x M-PEE - ไม่สนิทบิดหมด (Thai Riders Anthem) [Official MV]](http://i.ytimg.com/vi/kPJZ0UihBfk/mqdefault.jpg)

![[Full] 4 ต่อ 4 Celebrity EP.922 | 10 พ.ย. 67 | one31](http://i.ytimg.com/vi/zmV5HRIxIBI/mqdefault.jpg)

Im gonna recommend this channel to every moving being i cross by

hahaha thanks!

100% agreed

especially to average moving beings I guess

Bro, I have taken time series 3x and you have done the best at explaining these concepts better than all my teachers. Great work!

Indeed

I have just found your channel and finally I understood the GARCH model! Bless you, all your ancestors and future offspring 🥳🥳🥳

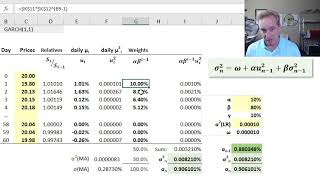

Practical Aspects

www.bucketscene.com/post/generalised-autoregressive-conditional-heteroskedasticity-1-1-approach

Generalized AutoRegressive Conditional Heteroskedasticity - GARCH

- Auto: "self"

- Regressive: "act of going back"

- Hetero: "different; other"

- Skedasticity: "scattering; dispersal" (referring to σ)

Thanks 👍

3 years after also there are no such playlists related to time series that match to your level as far as i found. I think that itself makes this playlist most valuable. thank you so much. love to see more playlists from you.

Waaaay better explanation compared to my professors during my Masters degree. Thanks !

You're very welcome!

Few times I've seen more clarity in explaining these models. Thanks for uploading

I have never in my life seen such a good teacher before. When he says some weird shit he explains what it is and why it’s important / why we need it. Thanks for these vids

YOU ARE AMAZING. Took all offline and online ways to learn, this is the best! Keep going

These are great videos. Keep it up! This is very helpful for many graduate students. Can you do another one discussing the differences between the DCC-GARCH, CCC-GARCH, and VCC-GARCH?

Thank you man 4 the perfect explanation of arch and garch. I'm studying for statistics method for financial markets exam and without you I'd be lost.

I feel you mate❤

I'm studying in Germany and I'm doing a statistic exam tomorrow. Your videos save me! Very well explained

You failed or not?

@@ahmadabdallah2896 no I don't :-) I passed the exam!

God bless you for these teachings, why can I have teachers like you in my life :)

You have done great job in explaining time series. Easier to understand and concise.

Great explanation! Succinct. Nice that you had just about all the equations already written and then needed to add only the volatility. Great format.

So far the best explation i had ever hear in my life about time series

Wow thanks!

your videos are amazing! you make things super easy to understand by explaining it better than my uni lecturers!

Happy to hear that!

This is one of the most well explained tutorials out there! Thanks ..

Wow! this is really helpful to understand the concept of ARCH, GARCH. Thank you so much !

glad it was helpful!

The way you explain the concepts of the models very intuitively is awesome. Keep the great work. Tks from Brazil.

Glad you like them!

You're an angel, may god bless you and your loved ones! Thanks a lot!!!

THANK YOU!!! Wow, bringing these concepts down to earth like that, how refreshing and helpful, thx a lot mann!!!

agreed.. when I was in ECON grad school... GARCH was our final exam... (the trick is taking a 2nd regression on the error terms themselves)..Adv Econometrics 4....this video (and your effortless explanations) reminds me of what a beautiful art form this level of mathematics is...well done, sir

Literally the best explanation out there. Thank you!

You're very welcome!

a pure talent of teaching.. impressive

as a beginner, I am happy with the explanation. So helpful.

Very nice method of teaching. Helped!

This video is so helpful I understood the basics in just 10:24 minutes. Although I was reading about it for the past 2 weeks and was still confused. Thank you for making this video.

A well explained video with some crystal clear presentation, congrats.

thank you for the video! everything is well explained! much better than my lecturer!

You're very welcome!

Great job explaining these time series terms.

thanks!

very short and informative.. found it useful ..this is great to see the simple way of ARCH and GARCH model

Glad it was helpful!

Thanks for existing!

Very simple and understandable at its easiest way. Good work and keep on.

Wow! You are really really good at this! Thanks a lot for your contribution. Great resource!! I am sure you are helping a lot of lives.

Hi! I really learn a lot from ur videos. You explain things very clearly.

Thanks for breaking it down into a much simpler form

Best explanation ever seen!

very well explained. This video has really come in handy through my time series course.

Great Explanation Ritvik. Good job!!

Thanks a ton

Very helpful videos! Thank you so much!!

Glad it was helpful!

Thank you so much for condensing it like this !!! so intuitive! May God bless your service to students. In the name of His Son Jesus Christ. Amen

Whatever school you teach at I need to enroll, you are really good at making this digestible!

I have been studying time series for 6 months, and you perfectly explained this concept in 10 minutes, hats off

Fantastic explanation. Thanks for preparing me for my final tomorrow!

You made it so easy. Thank you.

You're welcome!

Another question, just to make it clear: you said that ARCH(1) model retrives bursty volatility data. However, this only happens due to the specification of ARCH(1), ritght? An ARCH(p) model with, lets say, p=5, would be as capable as an GARCH(p,q) model to describe "volatility clusters", even though such ARCH(5) model could be very hard to estimate its parameters, correct?

You're the BEST! I passed my stochastic models exam and it included a very long exercise on which we had to analyze and comment the fitting of a model to a time series. Your videos helped me so much in understanding the differences between the models etc. I'll never thank you enough!

Congrats on passing your exam! Your kind words mean a lot to me :)

@@ritvikmath thank you so much!!! You're amazing. I wish my professore were more like you! 🥰

Practical Aspects

www.bucketscene.com/post/generalised-autoregressive-conditional-heteroskedasticity-1-1-approach

Thank you for these great videos!

Great job on your videos! Explanations are super clear.

Nice explanation, very simple and understandable!

Thanks!

Top notch videos!

I have one query if u could please explain. What is the difference between squared errors of lagged series and variance of lagged series in GARCH.

your explanations are so good, thank you for making these videos

Ananswered question - what is E (errors) is it from ARMA model errors (for instance it is in CFA institute book, level 2 2014 p. 494, we hahe to model ARMA, get residuals from model and then create ARCH)? Variance - is that variance from time series values or errors?

Nicely explained!

Thank you for the great videos.

insanely well explained, ty so much

no problem!

Thanks so much for your videos.you have a very easy and concise way to explain these complex models. I am immensely grateful with you because these videos have finally helped me understand this topic! :D

Very well explained.

Can you also explain the fitting of ARCH and GARCH models?

This playlist is helping me so much to prepare for a possible future interview on forecasting. This provides so much conceptual clarity. Thanks a lot. Had a small question, just as ARCH explains a bursty time series while GARCH adds an additional element to the ‘burstyness’ that once it bursts, it stays there for a while. Is there a similar graphical analogy for AR and ARMA model?

So thankful. I have a question. If we want to explain the relationship between GARCH(1,2) and a ARMA model, why does it bring me back to an ARMA(2,2) and not a ARMA(1,2)? I'd have a Alpha2*Et-2 that is the second autoregressive coefficient.

Great content!

Great and compact video!

It would be great if you could make a video about a multivariate Monte Carlo Simulation. I havent found any useful videos explaining (why we do) the Cholesky Decomp ect...

Thanks! And I'll definitely look into it :)

Great job. Really appreciate it.

tyvm! much much easier than understanding my prof

No problem!

Thanks for the video, but still confused. I watched your ARCH model, and it looks like the Y we modeled is the residuals (actual movie tickets sold - predicted movie tickets sold), but here it seems the a_i that the ARCH and GARCH are modeling refers to the original values (i.e. # movie tickets sold)?

Checking back the ARCH model video, there is an inconsistency about the ARCH model. The formula is different. As it is hard to type a formula here, can you have a look?

That's what I noticed, too! He mentioned in the arch video that the model was on the error but here he said the value of the time series itself? I'm confused

I agree. I have the same question.

Does it backtest well? Are you actually trying predict the future volatility level or the direction if it?

On a somewhat unrelated note: how do you determine the right timeframes for long term volatility?

Great content! Thanks for posting it

Hi!, Could you please clarify a few things about GARCH? :

Many tutorials and books use GARCH and ARCH on the innovations/u(t)/error of the time series and not on the time series itself. However you are modelling GARCH on the time series itself. I'm very confused and would love to get this cleared by you

Were these books written by idiots? ... I experienced same confusion!!! In CFA book (level 2) we have to use ARMA model to find errors fo ARCH process. But in some books I also find that i have to square surplusses of time series itself!!!

I thought the ARCH(1) was supposed to predict the volatility of today based on volatility of yesterday. But in this lesson, your ARCH(1) equestion now predicts the time series value of today based on yesterday value.

Same thoughts

I am so confused with this too.

It predicts only volatility, not the price

@@tanveersingh5287then what does he mean when he says “value of the time series “

This is correct. The volatility of yesterday can be rewritten as a function of yesterday's value

Thank you so much for the great video! I finally understood the basic idea of GARCH model.

Great videos, learned so much! thank you

Is your ice cream example not a poor example for GARCH? If there is a period of high ice cream sales, then volatility will jump from low season to high season, but then drop down again as the sales are consistently high... until it jumps again down to low season . Rather than having a consistent period of high volatility.

that was comprehensive and really helpful!!

I love this channel! Can you please make a video lesson about BEKK-GARCH Model?

Great explanation, make my life a lot easier!

Sir, this video was very helpful, your time series talk videos are very easy to understand and great it helped me alot. And can you please create a short video on GARCH- M model.

Perfect explanation!

brillaint sir

You are my hero

Hi, this a_{t} in ARCH part should actually be the residual or unpredictable part of a interested time series, instead of a time series itself, right?

I thought the same

Thanku soo much for wonderful explanation

Thank you for the great explanation. I want to ask, does it correct that the ARCH model resembles more of an autoregression (AR) than a moving average (MA)? I would really appreciate it if you could answer my question. Thank you in advance

Love your videos! You should think about doing an extension on this to cover the concepts behind eGARCH and/or GJR-GARCH

Awesome explanation man!!!

Great! a concise and clear explanation,thx, hope for more videos.

Thaks for this video, it was really interesting. Could you please create another one where you compare GARCH and FIGARCH ?

really good stuff.. Ritvik - fan of yours. Subscribed too :)

Thanks for the sub!

thanks you for your work. Another great video on time series :)

Thanks !

This is absolutely fantastic!!! Thanks so much. Could you please make some videos on panel data explaining fixed and random effects models?

What is the measure for volatility yesterday in the GARCH model?

great explanation

Why do you solve for error in the ARCH model video and the actual predicted ts value (a-t) for ARCH in this video?

I have the same question!

@@sissic2565 Hey Xixi, I think I may have figured it out. The ARCH version he made is universally true, but he makes the assumption that the mean of the error is 0 and the standard deviation is 1. This leads to us replacing it with returns!

Thank you! This is super helpful!

Glad it was helpful!

Great channel.

how do we calculate white noise: ϵt and ϵt−1 ? is that given by a random generator?

I want to understand the DCC GARCH model of Engle. Any video?

thankyou so much professor!

Thank you!! Very clearly explained.

Best explanation eveeeeerrrrr