Volatility: GARCH 1,1 (FRM T2-23)

ฝัง

- เผยแพร่เมื่อ 5 ก.พ. 2025

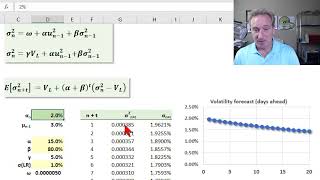

- [my xls is here trtl.bz/2t794bU] The GARCH(1,1) volatility estimate shares a similarity to EWMA volatility: both assign greater (lesser) weight to recent (distant) returns. But the GARCH(1,1) has an additional feature: it models a long-run (aka, unconditional) variance toward which the volatility series is pulled. Discuss this video here in our forum: trtl.bz/2YMnNWZ

Subscribe here www.youtube.co...

to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financial Analyst (CFA), and R Programming!

If you have questions or want to discuss this video further, please visit our support forum (which has over 50,000 members) located at bionicturtle.co...

You can also register as a member of our site (for free!) at www.bionicturt...

Our email contact is support@bionicturtle.com (I can also be personally reached at davidh@bionicturtle.com)

For other videos in our Financial Risk Manager (FRM) series, visit these playlists:

Texas Instruments BA II+ Calculator

• Texas Instruments BA I...

Risk Foundations (FRM Topic 1)

• Risk Foundations (FRM ...

Quantitative Analysis (FRM Topic 2)

• Quantitative Analysis ...

Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

• Financial Markets and ...

Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

• Financial Markets and ...

FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

• FM&P: Intro to Derivat...

Valuation and Risk Models (FRM Topic 4)

• Valuation and RIsk Mod...

Coming Soon ....

Market Risk (FRM Topic 5)

Credit Risk (FRM Topic 6)

Operational Risk (FRM Topic 7)

Investment Risk (FRM Topic 8)

Current Issues (FRM Topic 9)

For videos in our Chartered Financial Analyst (CFA) series, visit these playlists:

Chartered Financial Analyst (CFA) Level 1 Volume 1

• Level 1 Chartered Fina...

#bionicturtle #risk #financialriskmanager #FRM #finance #expertfinance

Our videos carefully comply with U.S. copyright law which we take seriously. Any third-party images used in this video honor their specific license agreements. We occasionally purchase images with our account under a royalty-free license at 123rf.com (see www.123rf.com/... we also use free and purchased images from our account at canva.com (see about.canva.co.... In particular, the new thumbnails are generated in canva.com. Please contact support@bionicturtle.com or davidh@bionicturtle.com if you have any questions, issues or concerns.

After seeing the second video on this topic, I started to get a light grasp! THank you so much for clearly explaining this!

Super clear! Thanks a lot admin

Thank you for watching!

Thanks David ! good explanation as always.

Superb, as usual

Why are the formulas in the 'D' column inconsistent? In the 'D9' cell, you divide current day by the previous day, but in all subsequent cells, you divide previous by current

Its possible to share this spreadsheet? I dont understand what isthe 0.880348% means... its the cel S73 and isnt possible to see... Thank you!

A link to the spreadsheet is found in the description, at the beginning; ie, the XLS is at trtl.bz/2JQufJy . I calculated 0.880348% by applying the "tedious" GARCH(1,1) on the previous day, σ^2(n-1). Thanks!

Thx for the great explanation. There seems to be a typo in the xls. It seems only the first relative (cell D9) is correct - the others are calculated as S(i-i)/Si.

Yes, you are totally correct ... such that the prior returns are negatives of those shown (e.g., -1.63% rather than 1.63%). Although because the first is correct, and the squared-returns are identical, it turns out to have no impact on the rest of the results! But you are still totally correct, great observation ...

Awesome video. Thank you!

Please throw more light on the Long Run Variance. Will it be given directly to us on the FRM exam?

That's my question too.

Can I use GARCH (1,1) for portfolio returns, or GARCH (1,1) just applicable for a single security returns?

Amazing again. Thanks!

great!

Thank you for watching!

Question might be kind of dumb, how did you obtain the volatility for the day prior at 12:35

nvm i watched the the how to calculate historical vol video.

I have the same question

O'Keefe Squares

6:34

How can I calculate the long run variance?

Please someone answer

@@akibnizamify Using eviews i think

Gusikowski Lock