Currently preparing for my masters thesis (not economy related). I hardly had any statistics courses during my studies, but now I need knowledge of time series analysis in order to create a forecasting model. Within just 3 days consuming videos on this channel, my understanding of time series analysis went from virtually 0 to something that at least allows me to read relevant papers and understand the basic concept of the proposed models within. This guy is amazing

You're amazing. I'm taking a time series course and the professor isn't so great at explaining any of these concepts. Really appreciate you and your videos! Please keep them coming.

your videos are great, first I was skeptical because of the style with the marker/ handwritten. But it is awesome !!! Your voice, your style of speaking, your structure in every video from arima to white noise. Very very valuable content !!!!! keep on going adding value to the world !!

These videos are so great! I am really happy I found them and I have to thank you for creating them. I would be greatful if you or anyone from your viewers could suggest me a book on time aeries analysis for referencing purposes. Thank you again 😊

stationerity assumes variance is constant. But hetroskedecity says variance is time specific. But in time series we see present of stationerity and hetroskdecity as well. How is this explained? shd these two not be mutually exclusive

Hi, your video is excellent, making time series much more understandable. But I couldn't find the video specific for Augmented Dickey-Fuller test in your videos. As you mentioned in this video, there is another video on ADF test. Thanks!

Ive been struggling to understand third condition of stationarity until now. I had an intuition it was something like seasonality but it was really not clear for me. Ty.

@@David-bo7zj No, variances never cancel out. For any 2 random variables, X and Y , Var(X+Y) = Var(X) + Var(Y) + 2*Cov(X,Y) and Var(X-Y) = Var(X) + Var(Y) - 2*Cov(X,Y) where Cov is the covariance. When, random variables are independent Cov(X,Y) =0. Hence, Var(e(t) - e(t-1)) = var(e(t)) + var(e(t-1)) - 0 = 2K^2

Good explanation, thanks. However, I am a bit confused with the condition on seasonality and wikipedia says seasonal cycles do not prevent a time series to be stationary. Could you share an example of a stationary time series that is white noise? Arent't f(x) = cos(x) and g(x) = sin(x) stationary?

Thanks for finally making me understand this concept, but im still trying to figure out what effect Stationarity has on my forecasts or how itll influence my forecast?

the models that are used for forecasting rely under the assumption that the time series that we want to model is stationary, without stationarity condition AR, MA, ARMA model cannot be utilized for modelling purposes.

Outstanding video, Any chance there is a video where you code this or solve an example with some values for those constant in the final equation for Z(t) Thanks a lot

Hello Ritvik! I've had this question forever, even after trying to deal with neural networks and Narmax models! I hope you would be able to reply and give me some light. How can we deal with zeros in time series? Modelling is based in events of a time series that Granger cause the one to be predicted but most of it consists of zeros. So far i just remove non interesting events and most of the zeros but should i be doing that or is there another approach? Thank you!

This explanation assumes “ strict sense” stationarity yes? There’s a slightly relaxed definition of stationarity called the “ wide sense” stationarity. I think the white noise process falls under ‘wide sense’ stationarity.

Excellent video!! great and concise explanation! But i just have one question left. What we forecast is the ts after differencing, but do we need to recover the differenced ts back to the original one? Will the forecast be the same? Or there is just no need to convert it back? Thanks in advance!

Stationarity in Time series The models like AR, MA assume our time series to be stationary stationary - mean constant, std dev constant and no seasonality non - lot of fluctuations in the data. first there were immense fluctuations, now less -> different std dev - mean is not constant. of a time chunk - seasonality - periodic trend over time how to check? 1. visually 2. global vs local tests (global mean =|= local mean) 3. augmented duckey fuller test how to make it stationary yt = b0 + b1 t + Et ( mean not constant in the graph) new series Zt = yt - yt-1 Zt = b1 + Et - Et-1 E(Zt) = b1 (mean of new series) (Et and Et-1 are constants from some distribution with mean 0) Var(Zt) =

Thanks for the video! I am just a little bit confused by the example in the end of the video. As the time series has already been modeled by the linear regression model, then why do we need to do the differencing to create a new series for modeling using AR/MA/ARMA? So in the end, to model such series, we need to combine both linear regression and AR/MA/ARMA? Or is it that we use AR/MA/ARMA to substitute the linear regression model? Thanks!

Hey @ritvikmath, I tried using ADF and KPSS on 3 sample datasets, similar to the ones in your video. One dataset violates the constant mean, the other thd constant variance, and lastly one with seasonality. However, it seems that both the ADF and KPSS are returning the datasets to be stationary for both non-constsnt deviation and the seasonality dataset. It accurately tests non-constant mean datasets. Any thoughts as to why that would happen?

I have been watching your amazing teaching videos which are so intuitive. Would it be possible for you to post the sheet notes you work on somewhere? It would be easier for us to make notes on top of those instead of trying to make our own sheets. Thank you!

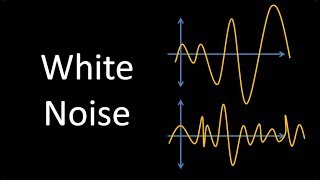

Doubt You said the mean for chart no. 3 is 0, as the local and global means are 0 but, the mean for chart no.3, varies locally depending upon where you take the interval. Eg. for half of the cycle it is different than 1/4 cycle

Why do you say that, in example number 3, the mean rule is not violated? If we look at different intervals, like in example number 2, then the mean will not be constant (for instance, taking the first half of a period and the entire period).

That's a great question! You are right that we can always find two intervals with different means but the idea of stationarity has more to do with whether the mean is consistently getting higher or lower. In the second graph, the mean is consistently rising whereas in the third graph, the mean is centered around 0. Hopefully that helps a bit!

you saved my life in my master study

Is this playlist good for ma eco student?

Currently preparing for my masters thesis (not economy related).

I hardly had any statistics courses during my studies, but now I need knowledge of time series analysis in order to create a forecasting model.

Within just 3 days consuming videos on this channel, my understanding of time series analysis went from virtually 0 to something that at least allows me to read relevant papers and understand the basic concept of the proposed models within.

This guy is amazing

The best test of whether or not our instructor truly understands a topic is their ability to explain it clearly. You PASS, again!

You're amazing. I'm taking a time series course and the professor isn't so great at explaining any of these concepts. Really appreciate you and your videos! Please keep them coming.

Ritvik, this was the most clear explanation of stationary I have ever found. THANK YOU!!!

OMG your visual example and explanation are very clear and easy to follow. Thank you so much for making such a thoughtful video!

Such videos are the reason why I still love TH-cam

Been following since I found your Ridge regression video. You're incredible, keep up the great work!

I appreciate it!

Best math teacher I have ever had the pleasure of being taught by! ❤

I've watched a bunch of videos now, started on SVM. The quality and pedagogy of these videos is superb! Great job!

So nice seeing how to make the time series stationary at end. Much appreciated!

your videos are great, first I was skeptical because of the style with the marker/ handwritten. But it is awesome !!! Your voice, your style of speaking, your structure in every video from arima to white noise. Very very valuable content !!!!! keep on going adding value to the world !!

so easy to understand, I've watched everything on TH-cam but this is where things start to make sense lolllll

Your videos are amazing, you make time series easier. Keep the good work

Thanks!

Seriously amazing, learned more from watching your videos for a hour then countless grad school lectures.

Fantastic Video!! The stationary has been puzzled me for a long time, this is the simplest and easiest video to understand!!

Really wish id discovered this channel before my semester ended

God bless you, man. It is like watching art, when someone can explain and articulate things clearly like you.

Damn, I was struggling to grasp this in my Finance class 8 years ago, and finally it landed!! You nailed it man!! Thnx a lot

no problem !

These videos are so great! I am really happy I found them and I have to thank you for creating them. I would be greatful if you or anyone from your viewers could suggest me a book on time aeries analysis for referencing purposes.

Thank you again 😊

you are seriously a life savor, much love

Never understood statistics any better...keep going please

Very intuitive (and quick) explanation!

Thank you very much for such amazing class !

Really good explanation, thank you man just incredible clear

You're very welcome!

Nice explained! I would like to see one practical example that would further elaborate this matter. Anyway great video and thanks!

Thanks! And good suggestion

Excellent, made time series concepts easier and interesting

Thank you for such a clear explanation!

Glad it was helpful!

Man !

your explanation is a life saver for Me thanks a lot :)

Very concise and clear explanation...

Thanks for clearing up the question about whether we can do a transformation like Zt to make the series stationary.

You are absolutely master piece

Concept of stationarity is nicely explained

Incredible useful for our my masters thesis

U are amazing.. i finally understand what time series are .. keep it up .. 🤩🤩🤩

No problem!

Yeah you are really great hope you continue to make the awesome videos ❤️❤️❤️

This is Amazing,Sir. Thank you!

Thanks this corrected a lot of my misunderstanding!

Great to hear!

Great work, super nice and simple explanations! You rock :D

Where did B1t and B1(t-1) go when you calculated z?

Thanks for pointing out. I also did not understand the expansion that led to the final value of Z.

Very well explained. Can you pl include a video on ADF test and how to interpret the P value?

Can you answer why B1t - B1t-1 = B1?

Found another gem on youtube :)

Thank you for this helpful video

Glad it was helpful!

Hi, please could you share the link to the ADF test?

stationerity assumes variance is constant. But hetroskedecity says variance is time specific. But in time series we see present of stationerity and hetroskdecity as well. How is this explained? shd these two not be mutually exclusive

Just insane! Thank you so much

Well paced. Please keep it up!

Excellent guide, thanks

Hi, your video is excellent, making time series much more understandable. But I couldn't find the video specific for Augmented Dickey-Fuller test in your videos. As you mentioned in this video, there is another video on ADF test. Thanks!

Good video.

Ive been struggling to understand third condition of stationarity until now. I had an intuition it was something like seasonality but it was really not clear for me. Ty.

Damn I need to refresh on some stuff but this helps out so much 🙏

Thanks!

excellent work. Your great sharings save me

hey no problem!

Excellent! Thank you!

perfect video, thanks!

i didnt understand the variance part .how variance of the errors is 2k^2 .Can someone explain it or suggest some reading material

I have the same question.

I also have the same question, would they not just cancel?

@@David-bo7zj No, variances never cancel out. For any 2 random variables, X and Y , Var(X+Y) = Var(X) + Var(Y) + 2*Cov(X,Y) and Var(X-Y) = Var(X) + Var(Y) - 2*Cov(X,Y) where Cov is the covariance. When, random variables are independent Cov(X,Y) =0. Hence, Var(e(t) - e(t-1)) = var(e(t)) + var(e(t-1)) - 0 = 2K^2

Thanks for the video!

Great explanation !

there is seasonality in your example...there's an upward trend, as well as seasonality about the trend

wonderful video

Hi! Thank you a lot. Could you make some videos on cointegration and causality. Concepts are very tricky for me

For the 3rd example, is the mean constant over different time intervals ?

I have the same question!

Good explanation, thanks. However, I am a bit confused with the condition on seasonality and wikipedia says seasonal cycles do not prevent a time series to be stationary. Could you share an example of a stationary time series that is white noise? Arent't f(x) = cos(x) and g(x) = sin(x) stationary?

Thanks for finally making me understand this concept, but im still trying to figure out what effect Stationarity has on my forecasts or how itll influence my forecast?

the models that are used for forecasting rely under the assumption that the time series that we want to model is stationary, without stationarity condition AR, MA, ARMA model cannot be utilized for modelling purposes.

great explanation, thanks

thank you for the video

Thank you very much, love it

Outstanding video,

Any chance there is a video where you code this or solve an example with some values for those constant in the final equation for Z(t)

Thanks a lot

Thank you so much

nice vid, much appreciated

Can you do a practical example of going from the differences back to y, the variable that we really want to forecast.

Hello Ritvik!

I've had this question forever, even after trying to deal with neural networks and Narmax models! I hope you would be able to reply and give me some light. How can we deal with zeros in time series? Modelling is based in events of a time series that Granger cause the one to be predicted but most of it consists of zeros. So far i just remove non interesting events and most of the zeros but should i be doing that or is there another approach? Thank you!

CAN SOMEONE PLEASE EXPLAIN WHY DO WE NEED STATIONARITY FOR ARMA PROCESS PLEASE? WHAT WILL HAPPEN IF IT IS NOT STATIONARY?

This explanation assumes “ strict sense” stationarity yes? There’s a slightly relaxed definition of stationarity called the “ wide sense” stationarity. I think the white noise process falls under ‘wide sense’ stationarity.

Great !

Excellent video!! great and concise explanation! But i just have one question left. What we forecast is the ts after differencing, but do we need to recover the differenced ts back to the original one? Will the forecast be the same? Or there is just no need to convert it back? Thanks in advance!

youre the best!

Can you talk about ergodicity?

Stationarity in Time series

The models like AR, MA assume our time series to be stationary

stationary - mean constant, std dev constant and no seasonality

non - lot of fluctuations in the data. first there were immense fluctuations, now less -> different std dev

- mean is not constant. of a time chunk

- seasonality - periodic trend over time

how to check?

1. visually

2. global vs local tests (global mean =|= local mean)

3. augmented duckey fuller test

how to make it stationary

yt = b0 + b1 t + Et ( mean not constant in the graph)

new series

Zt = yt - yt-1

Zt = b1 + Et - Et-1

E(Zt) = b1 (mean of new series) (Et and Et-1 are constants from some distribution with mean 0)

Var(Zt) =

Thanks for the videos.. could you pls make a video on Dickey Fuller test

Thanks for the video! I am just a little bit confused by the example in the end of the video. As the time series has already been modeled by the linear regression model, then why do we need to do the differencing to create a new series for modeling using AR/MA/ARMA? So in the end, to model such series, we need to combine both linear regression and AR/MA/ARMA? Or is it that we use AR/MA/ARMA to substitute the linear regression model? Thanks!

Brilliant

Good Video. But how is the mean constant in the third sine wave ?

very nice I am happy it

Hey @ritvikmath, I tried using ADF and KPSS on 3 sample datasets, similar to the ones in your video. One dataset violates the constant mean, the other thd constant variance, and lastly one with seasonality. However, it seems that both the ADF and KPSS are returning the datasets to be stationary for both non-constsnt deviation and the seasonality dataset. It accurately tests non-constant mean datasets. Any thoughts as to why that would happen?

I have been watching your amazing teaching videos which are so intuitive. Would it be possible for you to post the sheet notes you work on somewhere? It would be easier for us to make notes on top of those instead of trying to make our own sheets. Thank you!

much better than the professor!!!

Hey! Amazing content! However, I get lost in these formulas. Could you reccommend any course or book to learn more about these formulas? Thanks!

Awsome!!

Aren't we applying same method as in making unit roots to stationary? Is there a relation btn non-stationary ts and a ts with unit roots

Doubt

You said the mean for chart no. 3 is 0, as the local and global means are 0 but, the mean for chart no.3, varies locally depending upon where you take the interval. Eg. for half of the cycle it is different than 1/4 cycle

Sir in the variance step k^2 should cancel other k^2 and should be zero… please clarify!

Very good video, may I know what is Yt here representing?

Why do you say that, in example number 3, the mean rule is not violated? If we look at different intervals, like in example number 2, then the mean will not be constant (for instance, taking the first half of a period and the entire period).

That's a great question! You are right that we can always find two intervals with different means but the idea of stationarity has more to do with whether the mean is consistently getting higher or lower. In the second graph, the mean is consistently rising whereas in the third graph, the mean is centered around 0. Hopefully that helps a bit!

great job! thx

nice content

hello, could you please elaborate a little bit more on the 2K2, 8:56. Thanks

Would have been cool if you provide a way to download the scanned paper

tx sir

would not seasonality make the global mean being to equal to the local mean/s (depends on the chunk of series we take for a comparison?