(EViews10): ARDL-VECM and Causal Inference

ฝัง

- เผยแพร่เมื่อ 18 ก.ย. 2024

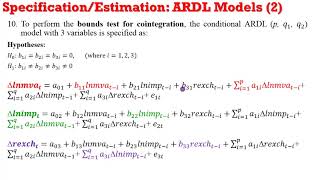

- A statement such as “X causes Y” will have the following meaning in different scenarios and disciplines such as X leads Y, X is the only cause of Y, X is only one of the possible causes of Y, X must always lead to Y (that is X determines Y), the occurrence of X makes the occurrence of Y more probable, X is a probabilistic cause of Y, X must occur either before or simultaneously with Y, but not afterwards, past values of X forecasts future values of Y. But Regression analysis deals with the dependence of one variable on other variables, it does not necessarily imply causation. In other words, the existence of a relationship between variables does not prove causality or the direction of influence. But in regressions involving time series data, the situation may be somewhat different. Short-run causal effects: through the F-statistics and the statistical significance of the regressors. Long-run causal effects: through the statistical significance error-correction term (applicable to VECM only). Joint causal effects: through the F-statistics and the significance of the independent variables and the statistical significance error-correction term (applicable to VECM only). Unidirectional causality: occurs from X to Y if the set of estimated coefficients of the lagged X are significantly different from zero and the set of estimated coefficients of lagged Y are not significantly different from zero. Bi-directional causality: occurs from X to Y if the set of estimated coefficients of the lagged X are significantly different from zero and vice-versa. Independence: occurs from Y (X) to X (Y) if the set of estimated coefficients of the lagged Y (X) are not significantly different from zero. Using EViews10, this video shows you how to perform causality tests in four different ways within a ARDL-VECM framework and interpret the results.

Follow up with soft-notes and updates from CrunchEconometrix:

Website: cruncheconometr...

Blog: cruncheconomet...

Forum: cruncheconometr...

Facebook: / cruncheconometrix

TH-cam Custom URL: / cruncheconometrix

Stata Videos Playlist: • (Stata13):Estimate and...

EViews Videos Playlist: • (EViews10):Interpret V...

TH-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, support my Channel with your subscription and sharing my videos with your cohorts.

Bosede Ngozi Adeleye Apologies I understand now the playlist is in ascending order .. was little bit confused as I am used to descending playlist . Everything is now consistent and have a flow. Thanks a lot . Thanks once more.. May Allah reward you for the good work

thank you so much for such a great tutorial specifically using eviews 10 which is still rare on TH-cam

U're welcome, Jy! 💕 Kindly share my videos with your friends and academic community too!

I am little bit confused please make it clear that, if dependent variable is stationary at level and independent variables are mixture of I(0) and I(1) then we can apply ARDL model or not.

Please refer to Pesaran papers on ARDL model for clarification.

thanks teacher

liiban ali mohamud U're welcome, Liiban! Please tell others too about my TH-cam channel. Share my links and videos with your social media community and academic networks. Thanks!

Thanks a lot

U're very welcome, Ghada! 💕

Thank you! It was really helpful for my master thesis

I'm glad you find my content very helpful. Keep blazing the trail, Andrea!!! Please share my videos with your colleagues...thanks!

Professor, I believe we theoretically set the direction of causality before running the ARDL model unlike in VAR where the directions are determined later. Then, could you please explain why we need to run the Causality tests in ARDL? Thanks.

Mohammad, I explained the essence of causality in the introductory video. Kindly watch it. Thanks.

good day, please after running bound test and confirming a long term relationship, is it appropriate to use VECM to estimate the model

Watch my videos on ARDL and Bounds Cointegration Test. Detailed to address your query. Thanks

Hi mam, How do we fix the lag for ARDL model(dependent and independent variable) and also for granger casuality?

Hi Vishnu, I covered lag selection on my ARDL videos. Also, watch my videos on CAUSALITY. Thanks

hi.. your videos area lifesaver... can you make a video on NARDL ....I have viewed many youtube videos and still confused. Would like to know how you would do the Nardl analysis in Eviews 10.

I'm not familiar with the technique, yet but I will learn and make videos on it. Please may I know from where (location) you are reaching?

@@CrunchEconometrix Hi I am from India

Should the value of Speed of Adjustment be less than 1?

Mukti, as explained in my videos the ECT lies between 0 and -1.

How we decide which one forecast is better depends on the basis of root mean squared error (RMSE), mean absolute error (MAE), and the sum of the forecast errors (SUM). Can you think of possible reasons why this is the case?

Sami, is your query related to this video?

Hello, first of all thank you for your explanation, but I have a question and I hope you answer me. What is the table that i should take for the short term results:

Is the first one at the start of estimation? Or the table where the ECT is located.

Thanks in advance

Hi Sawcen, the table with the ECT.

@@CrunchEconometrix thank you for your reply 🙏

I found an ARDL (1,0,0) afterward when I do ECM the table only displays the constant and the CointEq (-1).

In this case where I find the signs of the short term variables please 🙏

Sawcen, ARDL(1,0,0) implies the explanatory variables do not have any short-run relationship with the depvar.

You can get a million views but problem is finding which video is preciding which ? Like I can’t know which video is ARDL 1 ,2,3,4 etc the video seem random that’s the only challenge

Hi 2J, comments well taken. Kindly go through the EViews or Stata Time Series Playlists to find what you need.

Hello and thank you.

My question: Do we need to reverse the sign of the long-run coefficients, like we do for the VECM? Thanks.

Hi Michael, sign reversal is at the Johansen normalization (watch my video on Johansen cointegration) not VECM.

Hello! I performed ARDL Bounds Test for my equation with 4 variables and I found that all were cointegrated. However, upon performing the CUSUM test, there are one or two points that are beyond the 5% significance line. Does this mean that my model is unstable? Can you advise what may be the cause of the problem and how I could address it? Thank you!

Hi Dino, you have identified the problem. Proceed to engage structural break analysis.

Hi Professor, thank you for the video that helped me a lot, but can i ask you some questions? in ARDL, if the model proven to be cointegrated in the long run, do we need to ensure the independent variables to be significant still? can we use the insignificant variables in our estimation if the model is already cointegrated in the long run?

Airel, I don't quite understand your question.

@@CrunchEconometrix my question is, do we still need to make sure our independent variables are significant even though our model already has a cointegrating relationship?

You want to estimate the model without independent variables? Please follow what I did and adapt. In addition, read any of the resources listed at the end of the video for more details about ARDL. Thanks.

@@CrunchEconometrix Thank you Professor :)

Good Day Prof. Thanks so much for lectures. My question is if an equation has six variables of order I(0) and I(1) and the ARDL Cointegrating Bounds Test showed that when each of the variables when taking as a dependent variable, three variables were cointegrated and ther other three were inconclusive. Am I to do ARDL-ECM or ARDL-VECM? Please advise

Hi Godman, my video showed what to do. All you need is to adapt the knowledge to your study. Perform ECM on those with cointegration and ARDL on those without. Regards.

@@CrunchEconometrix Thank you so much ma. I am very grateful to you. Happy New Year

if i have 5 independent variable, then how i do ardl bound test/?

Same way I showed how to perform Bounds test. Number of variables is immaterial.

Thank You,Ma'am.It's really helpful to run the models.But Can i get your analysis and explanation in a written form? i am having problem to understand your explanations.

Hi Meher, thanks for the positive feedback. Deeply appreciated! You may need to play back the video for get the explanations. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix Sure, I am from Bangladesh , Ma'am.

Is it necessary to take each variable as dependent variable or if my dependent variable is say x... Can I perform ardl by checking it only on x as dependent variable and others as independent variable.. Why to take each variable as dependent? Plzz answr mam

Hi Dr. Mearaj, no to the 1st question and yes to the 2nd. I explained the reason why I used each variable as a dependent variable. You may need to watch the video again. Thanks.

Mam can u plzz tell. Me one thing.. Once my ardl test indicates cointegration.. Then either in my thesis or research paper should I show only long run causal results or both short run and long run or only short run... Plzz clarify my doubt....

Advisable to show all the results.

Please madam, can i send my work for you to interpret? I am using time series analysis

Hi Vitalis, no. I don't get involved in personalized tutoring due to time constraints and my busy schedules.

Hi there. can I ask, why RIR and LNINV is disappear when you regress short-run analysis? I realised there is only ECT(t-1)? It happened to several of my independent variables in my analysis

Hi Farah, that's the way the EViews algorithmn reports. You'll observe that the short-run estimates are shown first, so always note them and use to generate your results table.

Good day Prof., please i wanted to know if the max lag you used for both the dependent and regressor variables when conducting the test for the ARDL model was based on the lag length criteria from the previous video on how to test for lag length criterion.

Hi Nissi, did you watch the PREREQUISITE videos as suggested? If yes, then you already know the lag structure used. Kind regards.

Good afternoon my valuable prof and here is camara from Guinea. I've submitted one of my papers to emerald insight journal for publication where i used ARDL and VECM simultaneously. The reason for this choice is due to the fact that all the variables used in the study showed a cointegration relationship as dependent variable. Therefore, i used ARDL model for short run and the VECM for long run as stated by one of your tutorial videos on the relationship between ARDL and VECM model. However, reviewers from Emerald Insight journal are not happy with it and they are asking me for justification so can you please help me? Thank you in advance for your prompt reply.

Camara, pls watch my video again to understand what I did and the justification I gave for doing it. I always give clear explanation. Thanks.

@@CrunchEconometrix Thanks for your time Prof. Indeed, you explain well but i still need the exact link of the video in relation with the simultaneous use of the ARDL and the VECM to back my paper. Since yesterday, i looked for it in your tutorial videos but no success so please help me...

But you claim to have watched this same video... search through my Channel with "ARDL". Thanks

@@CrunchEconometrix Yes i did but longtime ago...

MAM IF THERE IS NO COINTEGRATION BUT THE ECM COEFFICIENTS ARE SIGNFICANT , WHAT DOES IT IMPLY?

Hi Apica, if no cointegration why perform ECM? Didn't you watch the prerequisite videos and listen to the explanations I gave in this clip?

Mam can you please clarify if I have presented a research paper in a conference and want to publish the same paper in a journal.Can I do that??

Oh yes, Zoya...you can.

@@CrunchEconometrix Thank you for the clarification..

I have an extra variable shown in the error correction form of the ARDL model in first difference form and significant! what can I say about this?

Short-run coefficient.

@@CrunchEconometrix

Hi. When we use the johanson cointegration test to find out the existence of cointegration we come across the normality of the coefficients what is the essence of that? And can that be used?

Hi Khalid, I gave the interpretation in the Johansen Cointegration test video. Kindly watch it.

Estimate the ADL(2,2) model GIPt = α + β1GIPt−1 + β2GIPt−2 + γ1GCLIt−1 + γ2GCLIt−2 + εt , and show by means of an F -test that the null hypothesis that β1 = β2 = γ2 = 0 is not rejected. Then estimate the ADL(0,1) model GIPt = α + γGCLIt−1 + εt and use this model to forecast GIP for the five years from 2003-2007. data are send through email. thanks

Sami, my videos are well-explained showing you "what to do" and "how to do". Kindly follow, Thanks.

Thank you so much for lectures.

Can I use ARDL for all I(1) variables? At first I tried to use VECM but the result shows that the optimum lag is 1. While the vecm model use lag-1, so I cannot use VECM. Is it right?

Can I use ARDL instead?

Thank you in advance.

Yes Azizah. But know that using ARDL or VAR also depends on your study objectives not ONLY on the stationarity of the variables.

@@CrunchEconometrix I see. But I'm confused with the study objectives. May I know what kind of study objectives so that ARDL can be used?

Azizah, objectives are study related.

@@CrunchEconometrix Thank you so much for your replies.

How can we extract the long run and short run results from ARDL model using EViews 10?

You obtain short-run results from the "ARDL" syntax, and long-run results from the "Bounds test and long-run form" syntax.

@@CrunchEconometrix thanks

As per your recommendation i have run an ARDL, however i cannot seem to find the option to perform a bounds test?

Watch my videos on the Bounds test.

Hi Prof, is the VECM performed on the level form of the variables or first difference?

Hi Hildah, VECM (if you are referring from the VAR model) is performed on the 1st difference of the series.

Madam, I am confused that for ARDL model we should use the natural data or the data which already taken first differences?

Hi Yen, there's no need to be confused. I've explained over and over on threads related to ARDL modeling. You can estimate in 1st differences but I'm comfortable with using the raw form with the ARDL algorithm and using the 1st difference with the OLS algorithm. Hope this clears.

@@CrunchEconometrix Thanks madam for always helping me to solve my question ^^

Mam can u tell me how to interpret the different lag values of variables under ARDL model and how we can put it in table.suppose my lag selection value is 3 for all the variables.So how do I interpret this.I had to include only the significant values.For instance,my FDI value of lag 1 is significant whereas the lag 2 and 3 values are not.so how do I put it in the table.whether I have to mention the lag value or simply put FDI and write the values of it??

Hi Zoya, the best approach is to pick any published ARDL paper (see my COMMUNITY TAB for articles) read the SECTION 4 and adapt both the interpretation and presentation of results. Thanks.

@@CrunchEconometrix mam I have read several articles related to ARDL model but they haven't mentioned the different lag values.They have simply put the values of variables

Not quite. You may need to read my papers bases on the ARDL technique.

Mam please provide the link of your paper

Please see the COMMUNITY TAB of my Channel for the papers and link to access them. Thanks.

Hai prof. I want to ask if there is cointegration but the CointEq(-1) value is signifacnt but has positive value, then how should I interpreted it? Thank you prof

Aina, there's no long-run reversion to equilibrium. Model diverges. It is explosive.

@@CrunchEconometrix Prof does it means that the short run in ARDL do not converge to long run equilibirum?

Aina, YES.

@@CrunchEconometrix I understand. Thank you very much prof ☺

@@CrunchEconometrix Prof, if there is no short run converge to long run, the long run variables obtained from the long run estimations are still valid right prof? So I can conclude that the variables that have long run relationship are GDP, CPI. However, there is no long run convergence in the model. Is it correct?

do you think the speed of adjustment could

Yes, but not lower than -2 (see Loayza and Ranciere, 2006). May I know from where you are reaching me?

thanks for your reply and i am from ethiopia.

@@brhanetesfay7997 Awesome! Kindly spread the word about my videos to your students, friends and academic community in Ethiopia 🇪🇹 for awareness. They'll learn some useful tips and skills too...thanks 😊

OK don't tell me about It this all my In sharing your videos and thank-you for helping us through sharing your knowledge of economics

honey can you please provide subtitle...???

Not possible at the moment, Mahfujur. Maybe in the near future.

Lentamente per favore...silvo plea no parlez rapidamente

Thanks, Ghada! 💕 😊

U r excellent but u speak too fast..i am tired of following u ..and my heart ❤ beats faster than u .please be slower ...mas despacio my dear

Sincere apologies Ghada, I'm naturally a fast talker but I try to be as clear as possible. Please always ⏸ and play ▶ the clips to get the best of me (lol). Thanks for watching and sharing too! 💕 😄

@@CrunchEconometrix how do you interpret a negative coefficient that is significant?

@@cmkalumbu It implies that X has a negative impact on the depvar, Y. Depending on the functional form of the model (see Wooldridge or any basic econometrics textbook), the interpretation is: a unit/percentage change in X will result in a unit/percentage decrease in Y, on average, ceteris paribus.

@@CrunchEconometrix so what could I have possibly done wrong if the variables signs are showing the opposite of the theory.? Like the relationship between GDP and saving supposed to be positive but the model shows a negative relationship.

@@cmkalumbu Yeah, some models are like that and several factors could be the cause: scope of the data, control variables (CV) used. Experience has shown that CVs exert some influence on the sign of the key regressor. Performing Monte Carlo simulation on the same key regressor using different CVs will result in different signs of the regressor. Try it out.

teacher tell your name

Hi Liiban, it's shown in the video... towards the end with all the links to my website and Facebook Page.