TH-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, help me stay online.

Hello Professor, Already subscribed and watched twice to understand the method in better way. Kindy refer few research papers to interprete the findings in correct way.

Thanks Kushwaha for your subscription, deeply appreciated!. These papers use CUSUMSQ test: (1) Adeleye et al (2017) - Financial Reforms and Credit Growth in Nigeria: Empirical Insights from ARDL and ECM Techniques (2) Zgambo and Chilese (2015) - Empirical Analysis of the Effectiveness of Monetary Policy in Zambia (3) Belloumi (2014) - The Relationship Between Trade, FDI and Economic Growth in Tunisia: An Application of the Autoregressive Distributed Lag Model (4) Shahbaz and Islam (2014) - Financial Development and Income Inequality in Pakistan: An Application of ARDL Approach ...I'll love if you help share my link too :)

Hello, thank you for posting such a useful videos about ARDL. I have the following questions about the procedures. 1-Why did you use the VAR analysis to get the proper lag of the regression in the first place? Eviews have the information criteria to determine a proper lag structure. 2-why did you identify only 1 lag and did not follow eviews recommendations? 3- Eviews 10 have long and short run regression estimations including the ECM, why manually take the difference? CUSUM test is already included in eviews 10 for ARDL, why estimating a simple regression analysis and then perform CUSUM test?? I hope to that you notice these questions :)

Hi Steve, this is the OLS approach (indicated in the Topic) to estimating an ARDL model. You can check my other ARDL videos where I used the ARDL algorithm to run the analysis. Hope these help, thanks.

@@CrunchEconometrix Dear professor, thank you for answering my question. I want to add, what if the acquired results are counter intuitive for the selected lag. For example. when examining the relation between GDP and Foreign direct Investment (FDI) I dont get consistency in the sign of the parameters across different lags (with statistical significance). What does this really mean? Does this mean that I have wrong model specification although that the lags are determined according to information criteria or what? does this mean that for each lag (or quarter) the relation between the variable can change dramatically and in contrast with the theory? there is no serial correlation and the model passed the CUSUM test and CUSUM square test. This may indicate for stability in the estimation.

Not exactly. Unless all the info criteria agree on the same lag length otherwise select other info criteria if there are different optimal lags and re-estimate the model. Then choose the results whose coeff-signs are close to your expected a priori.

Hello again.Since i am doing an ARDL model, I followed your advice to use the ARDL bounds test to determine if there exists a long run relationship among my variables. My dependent variable is logrgdp and my regressors are logrgc, logrgk, and logrfr (where rgc=real government consumption, rgk=real public investment and rfr=real government revenues). The value of F-statistic is 10.45432, higher than I(0) and I(1). Hence, I can reject the null hypothesis of no cointegration. Further, based on the AIC criterion, 1 lag is the appropriate lag length to use. I then specified my ARDL model as logrgdp c logrgc logrgk logrfr logrgc(-1) logrgk(-1) logrfr(-1) logrgdp(-1) and estimated it thru OLS. But what is bugging me, how will I specify the ECM model? Based on your video, you only included the 1 lagged of independent variables in their first differences plus the 1 lagged ECM(residuals) while the dependent variable is in first difference. Should i do the same? Your help shall be greatly appreciated. Thank you so much.

Dear ma’am, I don’t know how to thank you. You are just amazing. You are a life saver for us. Please keep uploading such videos. With due respect, I have a simple question. You have run the diagnostic tests for 1. Short run model 2. Long run model 3. error correction model. My question is which diagnostic test result I should keep in my paper? The long run ones or the ones with the error correction model? For your kind information - I am trying to show a long run relationship between CO2 emission and economic growth.

Hello ma. Thank you so much for the videos. Your tutorials have been very helpful in my project. Here's my question: I'm using 2 models and after the bounds test, I discovered there is no cointegration in both. Is it possible that there are errors that make one's model not to cointegrate when it is supposed to. I just want to be sure, the cointegration didn't emanate from an error. Thank you.

Thank you for your videos, that very help full. I have one query while you are estimating the long rum model you specify it as Inimp c Inimp(-1) Inmva(-1) rexch(-1) and ect is found then you use ect (-1) at lag one in the short-run model specification. so the question is while estimating the long run you take lag one for the independent variable and in short-run as well you have taken ect(-1), so does it not make ect at 2 lag while specifying short run model .

@@CrunchEconometrix it would be appropriate to use long run model specification as lnimp c lnmva rexcha as it will give ECT of current time period and for short run model ECT(-1)

Thank you for all the great videos you have posted. I have a question regarding interpretation of long-run estimates. I understood that long-run model is --> lnimp c lnimp(-1) lnmva(-1) rexch(-1). Do the results from OLS of this model give us information about long-run relation? In your example, can we say that "the first lag of mva shows negative elasticity relationship on imp with a 0,257% decrease, ceteris paribus, in the long-run"? If I am wrong, where do we collect long-run estimates (coefficients/t-statistic)? Thank you in advance.

Hi Djordje, thanks for the encouraging feedback. Deeply appreciated! You gave the appropriate interpretation and the derivation of the long-run coefficients is as shown in the video.

First of all thank you very much for your helpful videos. I really appreciate it. But I've a little problem about this issue. I've run ARDL test both ARLD estimator (estimation - ARDL options) and OLS approach which used "d(y) c d(y(-1)) d(x(-1)) d(x(-2)) y(-1) x(-1)" formula. But there's a differences between two estimations and outputs didn't match. Do you have any idea why I get this such results?

Hi Merve, thanks for the positive feedback on my videos. Deeply appreciated! 💕 The reason is simple. The algorithms differ. Can't get the same results.

Hello Dr. Thanks for the tutorial on model specification when there is no cointegration in the bound test. Please how do I interprete the coefficients of the ARDL short run result given the numbers of lags selected. Thank you Dr.

Hi Aaron, interpret your results in relation to the lags. Eg: "At the 2nd of X3, the coeff is positive and significant at the 5% level which means that..."

I know I may have had a lot of questions in the past. But thank you for the effort of making this sort of video's. Maybe it is not entirely correct, because the long run model is different from the ARDL- bounds test with long run levels equation? But the ARDL SR-model can indeed be estimated like so, thank you for this.

Thank you for all your efforts, Ma. Your videos have been helpful. If I may ask, must we include the difference operator while estimating the ARDL short run model? Can't we just estimate without the difference operator? I

@@CrunchEconometrix Thanks for the prompt response. Permit me to bother you further, I'm carrying out a research on the impact of stock market development on the Nigerian economic growth. My independent variables are six in number while my sample size is 30 years. The variables are a combination of I(0) and I(1) so I tested for cointegration using the bounds testing technique. The result says there is no cointegration so I proceeded and estimated a short run ARDL model with one lag across all the variables. To my surprise, the regression result came out and none of the independent variables and their lags was significant. Also, the R^2 was too small. Could it be that the sample size is too small? Or could it be that the independent variables are too many? What could be the problem? Pleases pardon me for bothering you too much.

You will need to do proper diagnostics of the explanatory variables: 1) are they correlated (watch my video on MULTICOLLINEARITY) 2) are they relevant (watch my video on ARDL Models: General-to-Specific). You will find these suggestions very helpful.

It is such a hugh help for my research!!! I appreciate your videos so much!! So I am doing the ARDL on eviews today for a study with 6 variables and there contains I(0) and I(1) data with cointegration, so i went for Estimate ECM. Even though the max lag line is 8 but I think too many lags will cause the loss of degree of freedom so I chose the optimal lag as 2, i accordingly run all the process until the Error Correction Specification, how can I interpret the result if there are ECT(1) and ECT(2)?? I found my ECT(1)'s coefficient is negative and significant on Prob. value, but ECT(2)'s codfficient is negative but obviously not significant with an value of 0.4295. What should I interpret the outcome in this situation?? Thank you in advance!!!

Hello professor and thank you for all your efforts in the teaching of econometrics. Regarding the subject of the video, i have got a question the interpretation of the ECM coefficient. It is of my understanding that the coefficient in question is the rate of adjustment towards the long-run values, thus if you have a ECM coefficient of -0.2, 20% of the disequilibrium will be corrected in the next period. So what happens when you have ECM coefficients lower than -1 like in this case?

Hi Yasmine, thanks for the positive feedback. Deeply appreciated! It is included a a LAGGED DEPENDENT VARIABLE in line with specifying ARDL models. Please may I know from where (location) you are reaching me?

Your videos are really helpful. Ma'am please tell me If optimal lag for dependent variable is 3 then we have to use 3 lags of ecm also while calculating ECM model.

Super helpful video, quick question - ARDL bound test found no co-intergration but when I am performing serial correlation my F (prob is .0001) so hence there is serial correlation, how to address this? there was no co-intergration in ADRL bound, Please please help

Hi there, COINTEGRATION and SERIAL CORRELATION are completely different concepts. If there's no Cointegration, I explained in the introductory ARDL video what to do. Kindly search through my Channel to watch the clip.

Once again, big help! Thank you but i had a confusion. If my variable has 2 lags, would my ect in the error correction model would be like this " ect(-1) ect(-2) ? Thank you !

Thank you Ma. when i try estimating my NARDL, it shows singular matrix. Please, what does this mean and how can i go about it? Secondly, do i need to log my variables before performing NARDL test?

Good morning, Dr. I really appreciate all your efforts, thank you so much!!! My questions today: Model specifications: d(lnmva) c d(lnmva(-1)) d(lnimp(-1)) d(rexch(-1)). Why current values of regressors are omitted? When comparing the output result of eviews and stata they are difference but they only alike at the output from "Lonrun Form and Bound Test" and "Error Correction Form" My question here is that... Is it where their outputs from eviews and stata genuine to interpret or where they differ? Like when I specified d(lnimp(-1)) c d(lnimp(-1)) d(lnmva(-1)) d(rexch(-1)) ecm(-1). Thanks

Hi Naceur, you can't deal with multicollinearity without dropping variables. Watch these two videos: Multicollinearity and General-to-Specific. You'll be guided on what to do. Hope these tips are helpful.

What a pleasure it is to watch your videos. Very informative. I run the diagnostics for optimum lag length and the recommended both by AIC and Schwarz is 0. How do I specify the model in that case? Should I plug in zero instead of (-1)?

Dear Professor. A quick question: When trying to find the appropriate lag length for the eventual ARDL model, would that equation be in levels of first differences? Also, Would the appropriate long-run regression equation be stated as an OLS, restricted constant and no fixed regressors for example, as: Retailrate c keyrate indep2 indep3 indep4 Secondly, could you kindly confirm if one would just run a simple OLS model of the above equation for the "long-run" pass-through and then save the residuals, etc and use them to form the ECM if there was a long-run relationship? Lastly, based on your lecture, the "short-run" version of the model will now have the ECT in there and will be ran in differences? Based on your illustration in your "How to Estimate ARDL and ECM..." video, you used some examples but some literature specify the models differently. Would one aslo need 5 terms with the summation signs plus 5 others with the subscript t-1 in the above example equation?Your kind response would be very useful for me to better understand your videos and practically apply the findings generally to ARDL models.

To the best of my ability, I have shown how to estimate ARDL models with clarity and examples. You may want to follow the guides shown and adapt to your research. Thanks.

Thanks Prof. I value your time highly and appreciate the time you take to respond. After watching all your videos , I was hoping that you could provide some more specifics just using the equation example I used above. The reason is because your videos though insightful, vary from other material but I believe you are credible as the others seem to leave out some of the difference operators, etc. Assuming there is indeed cointegration, could you kindly state the long run and short run equations? I will take it from there once I pass that hurdle, thanks.

It’s a pleasure to watch your videos, I’ve learned a lot! I am working with panel data to estimate the short-run and long-run effects of FDI on economic growth. Because of the combination of I(0) and I(1) variables, I am going to use panel ARDL. I found in another response of yours below that you suggested Stata over Eviews as the estimation is more complicated with Eviews. Do you suggest me to learn stata from the beginning or I still can estimate panel ARDL in Eviews(version 10 or 12)? Thank you

Thank you so much for this great explanation. What if the ECT is lower than -1 (e.g -1.25) but significant. Can I use that model? Or ECT must be in range of -1 to 0? Thank you.

Azizah, ECT should lie between 0 and -1. But there are papers with the coeff lower than -1. Check my COMMUNITY TAB for my FINANCIAL REFORMS ARDL paper. My ECT is -1.08 or thereabout.

thank you for the great help descibing ARDL.but ,i m confuced why do you run ARDL models to all varibles in the model keeping them as dependent variable seperately?

@@CrunchEconometrix .thanks for your early reply,but,still i want to know this :when i write my research paper ,should i run ARDL keeping all variables i use , as dependent variable seperately.if not ,is it enough to run one ARDL model as i write in my methodology? please ,can you give some example papers relavant to my question.

Hello, Dr. Your posts have been tremendous help! I run an ARDL model with the following 1: with trend and constant 2: constant without trend 3: no constant and no trend . But the best model chosen was 3: no constant and no trend, which does not surfer from serial correlation and hetero and also the model was stable with the CUSUM and the CUSUM SQUARE.Please how do i explain( interpret) a model without trend and constant? also the ECM was -0.03( annual data was used which was in log form), i hope it is a good ECM. Thank You.

Dear Maam, in 4:57 if my variable shows lag 3 then should I exactly write for instance d(rexch(-3)) or to write d(rexch(-1)) d(rexch(-2)) d(rexch(-3)) ? thank you

Dear madam, once again thank you very much for the highly informative video. In the end of the video you refer to the cusum and cusumsq tests to assess the stability of the model. However, if the model appears to breach the 5% boundary in either the cusum or the cusumsq test, what would you advise as a general approach? Many thanks

Hi Owen, thanks for the positive feedback. Deeply appreciated! If that is the case, perform a structural break analysis. Kindly watch my video on "Chow Test for Structural Break" for guide. Regards.

@@CrunchEconometrix Dear Madam, I may be so blunt to ask for your help again. Following your advice I have included an exogenous dummy variable within my ARDL model for the structural break. However, when conducting the cusum and cusumsq tests, I find that the test reveals only the timespan for the period after the structural break. Have you come across this issue and would you know how to overcome it? Many thanks!

@@CrunchEconometrix Thank you for the quick response. So just to affirm, if the line remains within the 5% bounds for the period after the exogenous structural break, I can automatically assume that the period before the structural break which is not shown within the cusum test results is also within the 5% bounds?

You are unnecessarily complicating issues. This video is very clear and straightforward on what to do when there's a break point. Kindly watch again, thanks.

Hello Ngozi, Thank you for your informative videos. I have two questions: 1. Do you have a reference (source) for the models you posted for the short run, long run and error correction model specifications? 2. Why aren't the contemporaneous regressors included in the models, only the lagged variables are included in all the models?

Hi Khadija, thanks for the positive feedback. Deeply appreciated. Since ARDL estimates are OLS estimates, you can always cite papers that used the ARDL methods. Also, only the lags of the regressors are included due to the way the equations are specified: i = 1 rather than from i = 0....may I know from where (location) you are reaching me? Thanks.

Superiority is not in question here. Model estimation is derived from model specification. If you specify the model with i=0, that includes the contemporaneous regressor and i=1 implies without. it is as simple as that.

@@CrunchEconometrix my final question. If the coeffcicients in the longrun model are all insignificant, do you still use the residuals from this model in the ECM?

Khadija, you will agree with me that any estimation having ALL insignificant coefficients is meaningless. The golden rule is that, at least 50% of the coefficients must be statistically significant.

Hi ma'am. Thank you for your informative videos. my model is a bivariate one. can i use an alternative method to johansen such as bounds and then continue on with ardl and ecm?

CrunchEconometrix Thank you for your quick response. I would be greatful for your response to these further queries: 1.in determining optimal lag here you alternatively changed the exogenous and endogenous. Were these the optimal lag for each model? In here however th-cam.com/video/jtb_4fqxBZE/w-d-xo.html all the variables were input as endogenous. It does not seem to go with the method for determining optimal lag of each series either wherein there was no exogenous there. 2. what is the difference between vecm and ecm? Do i understand correctly vecm is for multivariate? My data is bivariate. I would like to estimate ardl and ecm directly(not thru ols) but i only seem to find vecm models tutorial mostly. Could u direct me if possible to a tutorial on direct estimate of ecm. I am studying 3 bivariate eqns(the independent is common in 2 of them). 3. what if i have serial correlation?

Hi Ran, please know that if questions on different videos are lumped up, I simply skip them. But know that ECM applies to ARDL while VECM applies to VAR. Also, watch any of my videos on diagnostics to understand "serial correlation". Thanks.

I am a bit confused. From the specification of the ARDL, there should be the summation of the explanatory variables from when t=0, but yours start from t=1. Even if the chosen lag length is 1, it means one should start from 0 to 1 and not just pluck in 1. Kindly clarify, i will appreciate.

Yes, rightly observed. I chose to omit the level of the regressors and start with their lags. Like I told others previously, you can model yours starting with the level of the regressors.

Firstly thank you for this video record. I have a question which is I have 4 variables and after the BONDS test they are cointegrated. and I use the long-run coefficient ECM model. but all my answers ECM(-1) cof: -0.02 is it significant? if not can you give an example of a significant number

Hi Temur, which one are you referring to? Statistical or magnitude significance? I suggest to look up the difference between these concepts online. Thanks.

Hi, how can we interpret the numbers for the model at min 5:25, all p values are high, so what will be our conclusion here for this short run form model ?? Help please, I have the same case.. my thesis is about money demand

Dear Ma’am, can we estimate the ARDL model without including the current values of the regressor? I am a big fan! Thank you so much for your informative videos, they helped a lot!!

Thank you so much mam for so prompt response 😊. Mam we need to estimate ARDL Model for lnimp also in your example as there is cointegration or just we need to estimate only ECM

Hi! Thanks you very much for your amazing posts! I am suffering from CUSUM. Here are my questions and your answers will be greatly appreciated! Case 1: CUSUM within range, but CUSUM SQ out of range (only a small part within range)? What does it mean? What should I do next? Case 2: Both CUSUM and CUSUM SQ are out of range. I am actually quite shocked because the bound test has proved long-run relationship exists, while CUSUM and CUSUM SQ prove the relationship is not stable. In this case, should I just stop modeling at this step? Thank you very much and looking forward to your reply. I'm just a beginner and my questions may be stupid.

Hello Dr, thank you very much for this video, it is very helpful. My only issue is with the long run model specification after the bound test determines cointegration. Is there not supposed to be the summation sign when specifying it? Check the long run model in this particular video, at exactly 9mimutes and 9 secs. Please clarify this for me.

Hi Becca, thanks for the encouraging feedback. Deeply appreciated! The summation sign is used if there are MORE THAN ONE lag that series. So, as you can see the summation sign is not needed because only one lag is used for the regressors. Hope this clarifies.

Madam, Your videos on econometrics are extremely useful for me in writing a research paper. I need some clarifications. Following your video I got the appropriate lag length as 4. In that case do I need to take as ECM(-4)? Secondly, in the final Error Correction Model which you have displayed for LNIMP, the p-values for independent variables are not significant at 5% level of significance. In that case how can one write the relationship between dependent and independent variables as findings? Otherwise I also got the satisfactory result for Serial Correlation and also for stability CUSUM diagnostic tests. I appreciate your guidance very much.

Hi Manoj, ECM is ALWAYS with one lag. If pvalue of an explvar is not significant, it implies that the relationship between depvar and explvar is not significant and you interpret your result as such. Good that your post-tests are ok.

Madam, If there is cointegration and I(1) then should we use the ECM model which you have shown in this video or do we need to use the VECM model which you have shown in other videos?

@@mkjoshi21 Manoj, u've completely mixed up the explanations. The result of the Bounds test tells you whether u'll perform an ECM or a VECM (if that's what you want). So, I'll suggest you watch the video again and take down notes while doing so. Thanks.

When do you choose another model? Model 3 with constant from last video without trend I mean: Do I use model constant with trend for data like "New firms" + "Stock market capitalisation" + "real GDP"

Thank very much Dr for your professional way of explanation. I have two questions regarding the EViews if possible; first: the time series data used in EViews are they necessarily to be annually? secondly: Do I have to transform my time series data to natural logarithm before using them in the EViews or during the analysis? THANKS

Thanks Mohd, for the encouraging words and feedback. Deeply appreciated! Not necessarily you use only annual time series and log transformation is not compulsory but advisable.

Hello madam i have a case and below are the details i have public expenditure (LPE) as independent variable and Economic Growth(GNI) as dependent variable. After running bound test of cointegration, it is found that two variables are co integrated. However after running long run model coefficient of independent variable is not significant but while running error correction model coefficient of ect is found significant. what can we conclude that there is long run relationship between independent variable and dependent variable or something else. output of long run and error correction model are attached below .

@@CrunchEconometrix Thanks madam. Do me one more favour, kindly provide me name of some reference or text book which i can consult in order to comprehend furthermore ARDL modelling and its incidental issues. Thanks in anticipation.

Thanks Dr Ngozi for your support, very useful videos indeed. I have noticed that in some of the estimation the R square value is 0.05 so does this impact the model validity

Hi Younes, if I'm using this data for thesis or manuscript, I'd improve on the Rsquared by adding regressors. Thanks for watching and sharing my videos. Deeply appreciated!

@@CrunchEconometrix another question please, how can I incorporate dummy variables in my ARDL ECM model, let's say I am assigning a value 1 for specific date and 0 otherwise so how to get this dummy variable, previously I was using @expand(dummy)

Hi Ma'am. Your explanations are convincing. Thank you for such a great help. May I request you to throw some light on the interpretation of ARDL short run specification.

Hi Nihar, there's nothing really to the interpretation, since they are OLS estimates just give the ceteris paribus interpretation. E.g. "the first lag of mva shows a negative elasticity relationship on imp with a 0.257% decrease, on average, ceteris paribus in the short-run".

@@niharranjanjena3424 Hahahaha, that'll require me getting the R software and learning how to use it. Well, I may try it someday, but no promises made, though...thanks for the challenge! :)

Thanks for the video! I just want to know how to interpretation coefficien of ECM -1.1? From another source, they said the coef should be max -1. Because its percentage.

Hi Yosita, it means correction of the previous periods errors will be at an adjustment speed of 110%. That is, given the scope and variables used there will be faster adjustment to long-run equilibrium. If you change your variables or scope, you may not get the same outcomes. Please may I know from where (location) you are reaching me?

Hi madam,thank you so much. What will be my equation if aic show alav of zero is optimal for REXCH. Please ... In my analysis, I have getting like this...

Hello sir, thank you for your video it help me alot. I have done ecm and bound test and i have some question sir. In my bound test i find the data is cointegrated, however i didnt have negative and significant ect in ecm analysis, is that mean cointegrated result in bound test didnt always mean we have cointegration in the long run sir?, Is cointegrated result in bound test only mean we possibly have long relationship and ect result determine whether we have long run relationship or not?, If that so why some people always told the variable is cointegrated in the long run when the they find result in bound test or johansen test is good?

Hi Febiyan, the Bounds tests establishes if a long-run association exist among the variables. The ECM shows the speed at which reversion to long-run equilibrium is corrected from deviations.

Well thank you for all the great efforts you are putting into your lectures. Can you please answer one of my question, That is in your analysis in the case of ECM all the variables are non significant as their probability is higher then 0.05. Although the ECM(-1) is significant, so in this scenario How can we interpret the long term results if the variables are non significant ?

Thank you for teaching how to run ADRL using E-views. I have one problem. When I am running ADRL to check co integration between my variables of study I am only able to check cointegration between 2 variables as a time. Can you please elaborate on the problem.

Hi Akriti, thanks for the positive feedback on my videos, deeply appreciated. Cointegration should be on ALL the selected variables in the model. Unless you selected 2, otherwise watch my videos and run the procedure again....may I know from where (location) you are reaching you?

@@CrunchEconometrix Madam I am from India. I have tried running the ADRL model on my four variables but there was an error being shown by Eviews. At times it Would reflect singular matrix problem or at times it would says variables are already cointegrated. Kindly, Help how should I solve the problem.

Hi Akriti, "singular matrix" imply that there's multicollinearity among the regressors. (1) run a correlation analysis to observe the relative statistics and drop the highly collinear variable OR (2) run the VIF to see the highly collinear variable and drop it. Watch my video on MULTICOLLINEARITY....you will find it very helpful.

Thank you mam for these videos, however in my analysis on bounds test I found inconclusive cointegration where F value was between I(0) and I(1), how do I proceed in such a case

Good day ma. I absolutely love your videos. As directed, I have dropped my questions here: 1. Does the prob. value of the coefficients (LNMVA etc.) matter? As you did not speak on it but only the prob. value of the ECM. 2. The lag length criteria chosen by E Views for my model is 0. Is that normal? Thanks ma. Looking forward to hearing from you.

Hi Siji, thanks for the feedback on my videos. Most appreciated! 💕. Yes, all pvalues matter not just for the ECT....and lag length can be zero and if that's the case, then lag the depvar by 1 but 0 for others since we can't run a static model.

Hi Siji, thanks for the feedback on my videos. Most appreciated! 💕. Yes, all pvalues matter not just for the ECT....and lag length can be zero and if that's the case, then lag the depvar by 1 but 0 for others since we can't run a static model.

Thank you. How useful will be the model, if the variables are statistically insignificant (like those in the model)? Also, from your last message, when the p > 0.5, it is insignificant and when p

Hi... Thanks for such great videos, I have two queries. 1: In lag selection criteria using VAR, what if we get two optimal lags (i.e., shows stars on some measures for lag 2 and on some for lag 3) should we select both? 2. What if ECM model is insignificant (p > 0.05) and there is serial correlation? Thanks again.

Hi there, thanks for the positive feedback. You are to select optimal lags from only ONE information criterion. Also, p-value of ECT implies a not significant reversion to long-run equilibrium. If there is serial correlation, several measures can be taken: change control variables, use higher-order lags etc and re-estimate the model.

hi professor! your videos are easily understandable and appealing. your replies are very helpful as well. i have another question madam: I have read journals and even your example has a negative and significant ECT that explains the speed of adjustments. in all the references that i see, the ECT does not exceed 1.00 and is interpreted in percent. now, how can an ECT coefficient of -1.15 be explained? thank you very much madam. i am currently working on a quarterly data and have followed all your instructions as well as your replies from previous inquiries.

Good to know Hernan, and I'm glad to be of help. Yes, any ECT value not lower than -2 is still acceptable. The root of the model still lies within the unit circle. See my paper Adeleye et al (2018) - Financial reforms and credit growth in Nigeria: Empirical insights from of ARDL and ECM techniques. Please tell your colleagues about my Channel...thanks!!!

Thank you so much mum for your videos,they r so helpful.However, i have a simple question .my variables are I(0) and I(1) ,do i have to use d or (difference) all of them while running the model?

Good day Prof Ngozi. I watched your video on you tube that's on Error correction model. my challenges are. how do i interpret the lagged dependent variable supposing that the optmum lag length has been chosen to be (-1). and also if i find the ECT (term) being significant but greater than 1 and either positive or negative, how do i interpret it. is it appropriate to have such an explosive system of equations. thank you for your help. Wells from South Africa.

Hi Ngoni, thanks for watching my videos. (1) ARDL estimates just like VAR estimates are OLS estimates so just give the usual ceteris paribus argument. For instance, the past lag of per capita is associted with a 0.234 increase in gdp, on average ceteris paribus at the 1% significance level. (2) ECT can be between 0 and -2 (see Loayza and Ranciere, 2006). I cite this paper to support my result whenever I have a ECT value from -1. (3) No researcher likes an explosive model, so I always suggest that you change your variables with better proxies and re-estimate again. Hope these are helpful. Please don't forget to share my TH-cam Channel links with your social media and academic community, thanks! :)

@@CrunchEconometrix i got it "The third condition refers to the existence of a long-run relationship (dynamic stability) and requires that the coefficient on the error-correction term be negative and not lower than -2 (that is, within the unit circle)" (Loayza and Ranciere, 2006)

Thank you so much for your videos they really helped us a lot. I've a question concerning the ECM (ARDL model), when I do the ECM it drops one variable (the dependent variable) from short-run coefficients so what should we do to know its short-run coefficient and why is it dropped?

@@CrunchEconometrix the same question, why eviews drop one lag to all variables such dependent variable and independent variables, why ECM didn’t take the same lags of ARDL model ? Can you explain to me the reason please and thanks a lot🥰

Ahlem, I don't have an answer to this because you indicated that EViews AUTOMATICALLY select the lag lengths. You would have retained your suggested lags if you indicated FIXED. Hope these tips are helpful, thanks.

@@CrunchEconometrix many thanks for your answer but when i will fixed the lags then you will fixed the same lags for all variables that’s why i choose automatically lags but i change the number of lags. I want to know if i estimate the model by using the ols method is more appropriate than select options directly to estimate model ? What do you thing any suggestions please ?

Hi Madam, need your help please. Suppose the natural log of all the variables (dependent&independent) are taken, will the error correction term still be interpreted in the same way? I mean if the coefficient of the ect is -2.3, is a 2.3% adjustment or a 230% adjustment toward LR equilibrium? Some recent papers (2018 and 2019) where natural log of all variables were taken, are interpreting the ect as 2.3%. Can you please guide on which interpretation is correct? Thanks.

230% convergence is correct but nobody will take your results seriously. Change your control variables, use appropriate lags and re-estimate. Note: -0.023 = 2.3%

@@CrunchEconometrix Thanks Madam for your quick reply and great content. If the model with the ect -2.3 passes all diagnostic and stability tests, will it still be invalid or we just need to justify the over convergence? E.g. financial data are subject to overshooting hypothesis as a justification

Hello Prof, Thank you so very much. Your lessons are really helpful and interesting. However, according to Pesaran and Shin (1999) as also cited in Chap. 27 of Eviews-9 User Guide; "ARDL representation of estimating co-integrating models does not require symmetry of lag lengths; each variable can have a different number of lag terms". So I ask: if my optimum lag length is 3, contrary to your instruction in this session, in my long-run specification, can I also specify some explanatory variables at a lag of 1, and 2, but not more than 3 lags? Secondly, the above citation also states that: "Some of the explanatory variables Xj may be static ( no lagged term) or dynamic regressors( at least one lagged term). Based on this also, when specifying my model for estimation, can I also choose not to lag some variables irrespective of my optimum lag length?

Hi James, I have not made any contrary instructions on my ARDL videos and I encourage viewers to adapt the information given to their research. Glad you are familiar with the P&S (1999) paper so, kindly follow accordingly. Thanks.

@@CrunchEconometrix Thank you so much for the quick response. I am deeply sorry for wanting to bother you again. I still find it a bit confusing even with the P&S(1999) paper. In clear terms, with an optimum lag length of 2 for a co-integrating model, I am asking if I can also specify the model and estimate in Eviews, as : Y c Y(-1) X1(-1) X2(-1) X2(-2) X3 X3(-1) ...........(a) rather than this.. Y c Y(-1) Y(-2) X1(-1) X1(-2) X2(-1) X2(-2) X3(-1) X3(-2) ............(b)

I have two regressors and one dependent variable and bound test showed there was a cointegration. But none are signigicant include ect. Could this model be considered as good model? If not what can i do? Regards.

Thank you. I have watched that and my understanding is that when you estimate the ARDL model in EVIEWS the first eqution that comes is the short run equation and long run equation is obtained when you view the Long run form and bounds test.

@@CrunchEconometrix Since I just have 38 observations, may I know that AIC and SIC criterion, which should I follow? As SIC is allow for small sample size from 30-80.

Prof I have a question. I obtained CUSUM plot stable over the years (lies within significance level), but for CUSUMQ plot, there is some instability. Therefore, is there any reason why? and how should I interpret it?

Hi Aina, CUSUMSQ test provide the sufficient information on model stability than the CUSUM test. I advise you check out other online resources on the differences between the two concepts. Thanks.

thank you for sharing this i have questions, do we have to but -In the paper- ECM Regression as it appears or there is another way to compute final result? I mean if there's more than one lag for each, my Selected Model: ARDL(3, 3, 2, 4, 4, 2)

For this procedure with a breakpoint.. Is the dummy & the interaction terms in eviews without the "(-1)" lagged values or is it with the lags as in the model?

@@CrunchEconometrix [〖lent1〗_t=α_0+b_1 〖lent1〗_(t-1)+b_2 〖lmk134〗_(t-1) 〖 + b〗_3 〖ly〗_(t-1) 〖 + b〗_4 Dummy〖 + b〗_5 dummylmk134〖 + b〗_6 dummyly+ e_1t] is now my long term model for the ARDL I specified in your other video about ARDL, but I don't know if this is correct to input for OLS...

Hello DrThank you for all your effort and videos. I have one question: when i run my ARDL model I find the data is cointegrated, however the coefficients associated with the variables (ln-Urbanization, ln-GDP and ln-GDP square) in the long run are not significant. How can I interpret this? for example, ln(GDP) has a coefficient equal to (-1,29), can I say the impact of GDP is negative or I don't have the right to say that.

@@CrunchEconometrix Thank's Doctor, Please I have another question. what is the difference between short run and long run when we discuss the econometric model?

There is no clear definitiveness between the 2 concepts in the literature as they also depend on the issue being discussed. I advise you search online for more constructive information.

Hello your videos are very helpful, i am following your steps and when looking at the lag criterion i got two lags for my data does this sound correct? If so would i use ecm(-1) and emc(-2) or just ecm(-1)?

Hi Tyra, thanks for the positive feedback on my videos. Deeply appreciated. Please note that the ECM ALWAYS takes one lag because the captures the speed of adjustment to long-run equilibrium if a dis-equilibrium occurs in the previous period (implies a one-lag period). May I know from where (location) you are reaching me?

CrunchEconometrix thank you for your reply! So i will have two lags of my dependent and independent variables including ecm(-1). When I did this I got that my first lagged dependent variable is significant, is this a problem for my model?& I am from London

CrunchEconometrix for example in my model when I looked for the appropriate lag length it was 2 so In my model my equation would be d(lnx) c d(lnx(-1)) d(lnx(-2)) d(lnesp(-1)) d(lnesp(-2)) ecm(-1) ? Where lnx is the dependent variable and lnesp is the independent variable Sorry if I’m confusing you

I have a little trouble with series when i run stationarity test on them i found out they have unit root a level or log. Or i my the one missing something ma? You tutorial really help alot.

Hello! I have a question about the error correction variable which we get from running the long-run model. Since it is a variable, don't we need to run a stationarity test for it?

Thanks, Raymundo for the positive feedback. Deeply appreciated! Lags are automatically generated there's nothing you can do about it. But you can use 1 lag since you have an autoregressive model.

Hello professor, I have been following your channel for quite a while now and they have been very helpful. Thank you for making my life easy. I just wanted to ask, is it possible to estimate ARDL and ECM without using OLS approach? If all of my models are cointegrated, should I use ECM in all three of them?

Hi Sushi, thanks for the positive feedback and remarks. Deeply appreciated! Yes you can. Simply click on "View" and select "Bounds test and long run" and thereafter "Error Correction". For proper guidance, watch "ARDL and Dummy Variables (Bounds and ECM)...and there's no need for 3 ECMs. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix Thank you for your prompt response. I am from Nepal by the way. I have watched one of your videos, and there you mentioned that if all of the models are cointegrated, you have to use VECM. But in my case, not all of my variables are I(1), they are the combination of I(0) and I(1). Doesn't using VECM in this case violate the condition that all 3 of the variables should be I(1) before applying VECM model?

Sushi, pls pay attention to my explanations. ARDL is applicable with all I(1) series and combination of I(0) and I(1). Secondly, ARDL is a SINGLE EQUATION model not a system of equations. Thirdly, read references and papers on ARDL modeling. Lastly, previous response to this query subsists. Thanks.

Mam what if we have no lag for the regressors (0) as the optimum critera... How to find the short run result then.And I have ecm significant and negative, the problem is that the variable I have taken without any lag is not reported in the ecm. How to find it's short run relationship with the dependent variable. Thank u mam. Sorry for puzzling u.

@@CrunchEconometrix Thank you very much, so the short term effect will be the impact multiplier? or the total multiplier? Thank you madame, i am cursing this online and I am learning this! thank you :)

@@CrunchEconometrix Hello Crunch. I have seen that They call Impact Multiplier to the b0 in the ARDL model (contemporaneus effect): I quote: "For example, the interm multiplier for two periods would be (β0+β1+β2). The total multiplier is the final effect on y on the sustained increase after q or more periods have elapsed and is given by the equation ∑qs= βs" So I think in the short term I can get the interim or impact

@@CrunchEconometrix Dear Prof, how if the result shows p-value above 5% whichs means no short run relation ? Can I solve this problem and make it shows significant relation ?

Ma'am I got 3 lag selection from AIC and after applying it in ECM like d(pmi) c d(pmi(-1)) d(pmi(-2)) d(pmi(-3)) d(bsemf(-1)) d(bsemf(-2)) d(bsemf(-3)) ecm(-1) ecm(-2) ecm(-3) I am getting insignificant coefficient for ECM. What does that means?

@@CrunchEconometrix your analyses P-s in model are 0.8, 0.9 which are not significant in none of lvls, so the results of the model are not valid, or in case of ardl its the opposite?

I chose the proper lag length for Independent variable accordingly as in your lecture file. the data has 32 observations. when I choose maximum lag length 4, optimum is lag 4. when I choose maximum lag 2, it shows optimum lag 2. please advise which one I should choose. Thanks teacher.

Hi Sithu, since you have just 32 obs, you can't play with too many lags so I'll suggest that you indicate 2 as the maximum lag. Or run 2 regressions with each lag structure and see that which gives the best results.

Professor Thank you . Please guide me if ARDL can be used when all the variables are I~(1). Somebody guided me that it is not necessary that variables be I~(0) and I~(1) for ARDL to be applicable. Please confirm. Thanks and regards

Hi Apica, kindly watch my video titled "This is how to specify ARDL models". You will find it very helpful. Thanks. May I know from where (location) you are reaching me?

Madam, Can I use the ols method in the ardl when the variables are not cointegrated? and some of my variables are I(0), is it appropriate to make the first-difference of them when doing the ardl? and what can i do if the coefficients are not significant(p-value>5%) in the short-run model? thank you!

Hi Elody, this clip tells you when ARDL is applicable and the steps to estimating too. I will advise you to watch all my ARDL models for better understanding. You can do several things if your coeffs are not significant: change the regressors, use optimal lags, use the right technique etc. May I know from where (location) you are reaching me?

Hi Dr! If I get the lag value of 4, does it mean i have to do like this d(lrm1(-1)) d(lrm1(-2)) d(lrm1(-3)) d(lrm1(-4)) for all the variables? Also, do the lag make the ECT still be lrm1 c lrm1(-1) lrgdp(-1) lreer(-1) or need to make it to lrm1 c lrm1(-1) lrm1(-2) lrm1(-3) lrm1(-4) lrgdp(-1) lrgdp(-2) ...... lreer(-3) lreer(-4) to get the ecm(-1)?

Hi Thian, adapt the guides given in the clip to suit your variables. Remember: ECT is ALWAYS with one lag regardless of the variables lag structure. Thanks.

@@CrunchEconometrix I get 4 lag for my long run model specification, doest it mean my error correction model will be d(y) c d(y(-1)) d(y(-2)) d(ly(-3)) d(y(-4)) d(x1(-1)) d(x1(-2)) d(x1(-3)) d(x1(-4)) d(x2(-1)) d(x2(-2)) d(x2(-3)) d(x2(-4)) d(x3(-1)) d(x3(-2)) d(x3(-3)) d(x3(-4)) d(x4(-1)) d(x4(-2)) d(x4(-3)) d(x4(-4)) ecm(-1)?

Mam, we are watching your vide and . Its very informative. Mean while let me ask that if my variables are a mix of I0 and I1 and it's a panel data based approach. Are implying that ARDL has no options like bound test establish long run relarion? Pls I form us thank you.

Hi Kanika, this specification is crafted for endogenous variables using OLS estimator. You may need to watch my other ARDL estimator-based videos with dummy variables. Thanks.

@@CrunchEconometrix thank you mam for your reply. I have seen that video also but in that video ecm is not the way it's in this video. I have one dummy variable and 3 other regressors. In order to generate residual series we run long run specification in ols do we need to add dummy variable and how to incorporate DV in that specification. And when we run short run specification in ols where there is no cointegration (ardl) how do we incorporate dummy variable. Pls help mam. I am really confused.

Hi Miss, I have some doubts... If some variables are stacionary with the 1st diference but have unit root has level, we don't need to transform that variable? we can insert in model just like that? Also, can you suggest some literature on using ECM model? Thanks

Hi Francisco, you've misunderstood this. Unit root requires transformation into 1st difference. Follow my procedure as shown. It is well explained. Also, there are several papers on ECM. Do a Google search.

TH-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, help me stay online.

Hello Professor,

Already subscribed and watched twice to understand the method in better way. Kindy refer few research papers to interprete the findings in correct way.

Thanks Kushwaha for your subscription, deeply appreciated!. These papers use CUSUMSQ test:

(1) Adeleye et al (2017) - Financial Reforms and Credit Growth in Nigeria: Empirical Insights from ARDL and ECM Techniques

(2) Zgambo and Chilese (2015) - Empirical Analysis of the Effectiveness of Monetary Policy in Zambia

(3) Belloumi (2014) - The Relationship Between Trade, FDI and Economic Growth in Tunisia: An Application of the Autoregressive Distributed Lag Model

(4) Shahbaz and Islam (2014) - Financial Development and Income Inequality in Pakistan: An Application of ARDL Approach

...I'll love if you help share my link too :)

Thank you :)

Can you tell slowly teacher please because we didn't inderistand

Abdallah Mohamed Sorry about that Abdallah. But you can always playback the video to get the point. I always try to speak clearly, at least😉

Your tutorials are very helpful. I will continue watching them. thanks

Glad to hear that! Thanks a lot for the encouragement, Gabriel!

Thank you soooooo much. This has helped me in my project. I just can't thank you enough.

U're very welcome, JustAfrican. Happy to know that you find the content helpful. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix Ghana, Africa

Hello, thank you for posting such a useful videos about ARDL. I have the following questions about the procedures. 1-Why did you use the VAR analysis to get the proper lag of the regression in the first place? Eviews have the information criteria to determine a proper lag structure. 2-why did you identify only 1 lag and did not follow eviews recommendations? 3- Eviews 10 have long and short run regression estimations including the ECM, why manually take the difference? CUSUM test is already included in eviews 10 for ARDL, why estimating a simple regression analysis and then perform CUSUM test?? I hope to that you notice these questions :)

Hi Steve, this is the OLS approach (indicated in the Topic) to estimating an ARDL model. You can check my other ARDL videos where I used the ARDL algorithm to run the analysis. Hope these help, thanks.

@@CrunchEconometrix Dear professor, thank you for answering my question. I want to add, what if the acquired results are counter intuitive for the selected lag. For example. when examining the relation between GDP and Foreign direct Investment (FDI) I dont get consistency in the sign of the parameters across different lags (with statistical significance). What does this really mean? Does this mean that I have wrong model specification although that the lags are determined according to information criteria or what?

does this mean that for each lag (or quarter) the relation between the variable can change dramatically and in contrast with the theory? there is no serial correlation and the model passed the CUSUM test and CUSUM square test. This may indicate for stability in the estimation.

Not exactly. Unless all the info criteria agree on the same lag length otherwise select other info criteria if there are different optimal lags and re-estimate the model. Then choose the results whose coeff-signs are close to your expected a priori.

@@CrunchEconometrix thank you for answering!

U're welcome Steve, it's the least I can do. Thanks for watching and keep sharing too😀

Hello again.Since i am doing an ARDL model, I followed your advice to use the ARDL bounds test to determine if there exists a long run relationship among my variables. My dependent variable is logrgdp and my regressors are logrgc, logrgk, and logrfr (where rgc=real government consumption, rgk=real public investment and rfr=real government revenues). The value of F-statistic is 10.45432, higher than I(0) and I(1). Hence, I can reject the null hypothesis of no cointegration. Further, based on the AIC criterion, 1 lag is the appropriate lag length to use. I then specified my ARDL model as logrgdp c logrgc logrgk logrfr logrgc(-1) logrgk(-1) logrfr(-1) logrgdp(-1) and estimated it thru OLS. But what is bugging me, how will I specify the ECM model? Based on your video, you only included the 1 lagged of independent variables in their first differences plus the 1 lagged ECM(residuals) while the dependent variable is in first difference. Should i do the same? Your help shall be greatly appreciated. Thank you so much.

Yes, do same.

@@CrunchEconometrix thank you very much for your help professor. God bless

Dear ma’am,

I don’t know how to thank you. You are just amazing. You are a life saver for us. Please keep uploading such videos.

With due respect, I have a simple question. You have run the diagnostic tests for

1. Short run model

2. Long run model

3. error correction model.

My question is which diagnostic test result I should keep in my paper? The long run ones or the ones with the error correction model?

For your kind information - I am trying to show a long run relationship between CO2 emission and economic growth.

Hi Afia, check my Community Tab for any of my ARDL papers (or any ARDL publication) and adapt the diagnostics. Thanks.

This is spot on! thanks. I can now finish the master's degree. thanks ;)

Hernan Pantolla Awesome, Hernan! Glad to have helped out... please tell others by sharing my link and videos. Gracias!😄

Hello ma. Thank you so much for the videos. Your tutorials have been very helpful in my project.

Here's my question: I'm using 2 models and after the bounds test, I discovered there is no cointegration in both. Is it possible that there are errors that make one's model not to cointegrate when it is supposed to.

I just want to be sure, the cointegration didn't emanate from an error. Thank you.

Hi Great, if there's cointegration in the models the Bounds test would have indicated that. I explained this in my ARDL videos.

See my class rep oo 😂. I thought I was the only one econometrics is dealing with 😁

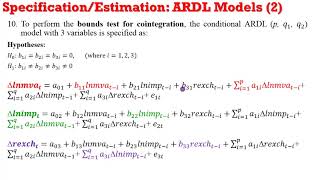

Thank you for your videos, that very help full. I have one query while you are estimating the long rum model you specify it as Inimp c Inimp(-1) Inmva(-1) rexch(-1) and ect is found then you use ect (-1) at lag one in the short-run model specification. so the question is while estimating the long run you take lag one for the independent variable and in short-run as well you have taken ect(-1), so does it not make ect at 2 lag while specifying short run model .

Ahmed, the ECT is ALWAYS with 1 lag.

@@CrunchEconometrix it would be appropriate to use long run model specification as lnimp c lnmva rexcha as it will give ECT of current time period and for short run model ECT(-1)

Thanks for your video

I want to ask a question why you change many variables as a dependent variable in this case??

Hi Ahlem, I give detailed explanation in all my clips. You may need to watch again to listen to my explanations. Thanks

@@CrunchEconometrix ok thanks a lot

Just one thing why you estimate the model using the OLS method ?

Ahlem, I gave explanations on why I did so. You will also observe that the procedures differ.

Thank you for all the great videos you have posted.

I have a question regarding interpretation of long-run estimates. I understood that long-run model is --> lnimp c lnimp(-1) lnmva(-1) rexch(-1). Do the results from OLS of this model give us information about long-run relation? In your example, can we say that "the first lag of mva shows negative elasticity relationship on imp with a 0,257% decrease, ceteris paribus, in the long-run"? If I am wrong, where do we collect long-run estimates (coefficients/t-statistic)? Thank you in advance.

Hi Djordje, thanks for the encouraging feedback. Deeply appreciated! You gave the appropriate interpretation and the derivation of the long-run coefficients is as shown in the video.

First of all thank you very much for your helpful videos. I really appreciate it. But I've a little problem about this issue. I've run ARDL test both ARLD estimator (estimation - ARDL options) and OLS approach which used "d(y) c d(y(-1)) d(x(-1)) d(x(-2)) y(-1) x(-1)" formula. But there's a differences between two estimations and outputs didn't match. Do you have any idea why I get this such results?

Merve Kurt I have this problem too. One question, when u used the ardl approach, did u do it first differences or the levels??

Hi Merve, thanks for the positive feedback on my videos. Deeply appreciated! 💕 The reason is simple. The algorithms differ. Can't get the same results.

@@renaebogle7547 I responded to you on this.

Hello Dr. Thanks for the tutorial on model specification when there is no cointegration in the bound test. Please how do I interprete the coefficients of the ARDL short run result given the numbers of lags selected. Thank you Dr.

Hi Aaron, interpret your results in relation to the lags. Eg: "At the 2nd of X3, the coeff is positive and significant at the 5% level which means that..."

I know I may have had a lot of questions in the past. But thank you for the effort of making this sort of video's. Maybe it is not entirely correct, because the long run model is different from the ARDL- bounds test with long run levels equation? But the ARDL SR-model can indeed be estimated like so, thank you for this.

Glad you enjoyed it!

Can u help me with estimating short run coefficient??

Zoya, I have responded to your query on a different thread.

Thank you for all your efforts, Ma.

Your videos have been helpful.

If I may ask, must we include the difference operator while estimating the ARDL short run model?

Can't we just estimate without the difference operator?

I

Yes, you should.

@@CrunchEconometrix Thanks for the prompt response. Permit me to bother you further, I'm carrying out a research on the impact of stock market development on the Nigerian economic growth. My independent variables are six in number while my sample size is 30 years. The variables are a combination of I(0) and I(1) so I tested for cointegration using the bounds testing technique. The result says there is no cointegration so I proceeded and estimated a short run ARDL model with one lag across all the variables. To my surprise, the regression result came out and none of the independent variables and their lags was significant. Also, the R^2 was too small. Could it be that the sample size is too small? Or could it be that the independent variables are too many? What could be the problem?

Pleases pardon me for bothering you too much.

You will need to do proper diagnostics of the explanatory variables:

1) are they correlated (watch my video on MULTICOLLINEARITY)

2) are they relevant (watch my video on ARDL Models: General-to-Specific). You will find these suggestions very helpful.

@@CrunchEconometrix Alright. Thanks a bunch, Ma

It is such a hugh help for my research!!! I appreciate your videos so much!! So I am doing the ARDL on eviews today for a study with 6 variables and there contains I(0) and I(1) data with cointegration, so i went for Estimate ECM. Even though the max lag line is 8 but I think too many lags will cause the loss of degree of freedom so I chose the optimal lag as 2, i accordingly run all the process until the Error Correction Specification, how can I interpret the result if there are ECT(1) and ECT(2)?? I found my ECT(1)'s coefficient is negative and significant on Prob. value, but ECT(2)'s codfficient is negative but obviously not significant with an value of 0.4295. What should I interpret the outcome in this situation?? Thank you in advance!!!

Hi Shenying, I'm sorry but your query is TOO long and very confusing to understand.

Hello professor and thank you for all your efforts in the teaching of econometrics.

Regarding the subject of the video, i have got a question the interpretation of the ECM coefficient. It is of my understanding that the coefficient in question is the rate of adjustment towards the long-run values, thus if you have a ECM coefficient of -0.2, 20% of the disequilibrium will be corrected in the next period. So what happens when you have ECM coefficients lower than -1 like in this case?

What is the exact value?

@@CrunchEconometrix I'm getting an ECM coefficient of -2.04

@@srjagger388 With -2.04, no one will take your results with seriousness. Change your regressors and re-estimate the model.

@@CrunchEconometrix Thank you very much for your advice! I'll do that

this is very helpful, thank you so much for sharing this ma'am :)

You are welcome, Zaim!🙏❤️

Very good Dr

Thanks for the encouraging feedback, Hamis!

Thank you. Why you include lnimp both as dependent and independent variables in the ECM

Hi Yasmine, thanks for the positive feedback. Deeply appreciated! It is included a a LAGGED DEPENDENT VARIABLE in line with specifying ARDL models. Please may I know from where (location) you are reaching me?

Your videos are really helpful. Ma'am please tell me If optimal lag for dependent variable is 3 then we have to use 3 lags of ecm also while calculating ECM model.

Ma'am please tell me how to make interpretation if ECM is insignificant

Hi Ruchi, ECM is ALWAYS with 1⃣ lag...and if insignificant, it implies that the reversion to long run equilibrium is of zero relevance.

Super helpful video, quick question - ARDL bound test found no co-intergration but when I am performing serial correlation my F (prob is .0001) so hence there is serial correlation, how to address this? there was no co-intergration in ADRL bound, Please please help

Hi there, COINTEGRATION and SERIAL CORRELATION are completely different concepts. If there's no Cointegration, I explained in the introductory ARDL video what to do. Kindly search through my Channel to watch the clip.

Once again, big help! Thank you but i had a confusion. If my variable has 2 lags, would my ect in the error correction model would be like this " ect(-1) ect(-2) ? Thank you !

Hi Ali, regardless of the number of lag lengths, it will be ECT(-1). There's only ONE ECT in every ARDL model.

Thank you Ma. when i try estimating my NARDL, it shows singular matrix. Please, what does this mean and how can i go about it?

Secondly, do i need to log my variables before performing NARDL test?

Hi Iwasam, I have not engaged NARDL. You may want to check out other online resources for guides. Thanks.

Respected Mam,

Why did you run ARDL model directly on log of variables ie. lnmva. Can we not run ardl on base series.

Hi Dhaval, using log of a series is at the discretion of the researcher. Regards.

Good morning, Dr. I really appreciate all your efforts, thank you so much!!!

My questions today:

Model specifications:

d(lnmva) c d(lnmva(-1)) d(lnimp(-1)) d(rexch(-1)).

Why current values of regressors are omitted?

When comparing the output result of eviews and stata they are difference but they only alike at the output from "Lonrun Form and Bound Test" and "Error Correction Form" My question here is that... Is it where their outputs from eviews and stata genuine to interpret or where they differ? Like when I specified d(lnimp(-1)) c d(lnimp(-1)) d(lnmva(-1)) d(rexch(-1)) ecm(-1).

Thanks

Hi Busari, you can include current values of the regressor but CANNOT use the lagged difference of the depvar as a regressand. Thanks.

When I include the current values of the dependant variables, my R squared value comes a abnormally high (0.97). Can you help me out with this?

Thank you for you clear clarification. But how we deal with multicolinearity in ARDL model? (without dropping any variable).

Hi Naceur, you can't deal with multicollinearity without dropping variables. Watch these two videos: Multicollinearity and General-to-Specific. You'll be guided on what to do. Hope these tips are helpful.

Many Thanks!

What a pleasure it is to watch your videos. Very informative. I run the diagnostics for optimum lag length and the recommended both by AIC and Schwarz is 0. How do I specify the model in that case? Should I plug in zero instead of (-1)?

Hi McDonalds, it will be d(X) since you have zero lag length.

Dear Professor. A quick question: When trying to find the appropriate lag length for the eventual ARDL model, would that equation be in levels of first differences? Also, Would the appropriate long-run regression equation be stated as an OLS, restricted constant and no fixed regressors for example, as:

Retailrate c keyrate indep2 indep3 indep4

Secondly, could you kindly confirm if one would just run a simple OLS model of the above equation for the "long-run" pass-through and then save the residuals, etc and use them to form the ECM if there was a long-run relationship?

Lastly, based on your lecture, the "short-run" version of the model will now have the ECT in there and will be ran in differences? Based on your illustration in your "How to Estimate ARDL and ECM..." video, you used some examples but some literature specify the models differently. Would one aslo need 5 terms with the summation signs plus 5 others with the subscript t-1 in the above example equation?Your kind response would be very useful for me to better understand your videos and practically apply the findings generally to ARDL models.

To the best of my ability, I have shown how to estimate ARDL models with clarity and examples. You may want to follow the guides shown and adapt to your research. Thanks.

Thanks Prof. I value your time highly and appreciate the time you take to respond. After watching all your videos , I was hoping that you could provide some more specifics just using the equation example I used above. The reason is because your videos though insightful, vary from other material but I believe you are credible as the others seem to leave out some of the difference operators, etc.

Assuming there is indeed cointegration, could you kindly state the long run and short run equations? I will take it from there once I pass that hurdle, thanks.

I explained what to do if there's cointegration. You may want to watch my ARDL videos again. Tha.

It’s a pleasure to watch your videos, I’ve learned a lot!

I am working with panel data to estimate the short-run and long-run effects of FDI on economic growth. Because of the combination of I(0) and I(1) variables, I am going to use panel ARDL. I found in another response of yours below that you suggested Stata over Eviews as the estimation is more complicated with Eviews. Do you suggest me to learn stata from the beginning or I still can estimate panel ARDL in Eviews(version 10 or 12)? Thank you

Stata is more robust for panel ARDL estimations.

@@CrunchEconometrix Thank you.

Thank you so much for this great explanation. What if the ECT is lower than -1 (e.g -1.25) but significant. Can I use that model?

Or ECT must be in range of -1 to 0?

Thank you.

Azizah, ECT should lie between 0 and -1. But there are papers with the coeff lower than -1. Check my COMMUNITY TAB for my FINANCIAL REFORMS ARDL paper. My ECT is -1.08 or thereabout.

@@CrunchEconometrix I will check it. Thank you so much for your response.

thank you for the great help descibing ARDL.but ,i m confuced why do you run ARDL models to all varibles in the model keeping them as dependent variable seperately?

Hi Adikari, thanks for the positive feedback....appreciated! I gave the rationale for doing that. You may need to watch the clip again, thanks.

@@CrunchEconometrix .thanks for your early reply,but,still i want to know this :when i write my research paper ,should i run ARDL keeping all variables i use , as dependent variable seperately.if not ,is it enough to run one ARDL model as i write in my methodology? please ,can you give some example papers relavant to my question.

My ARDL are clear enough detailing what needs to be done.

Hello, Dr.

Your posts have been tremendous help! I run an ARDL model with the following

1: with trend and constant

2: constant without trend

3: no constant and no trend .

But the best model chosen was 3: no constant and no trend, which does not surfer from serial correlation and hetero and also the model was stable with the CUSUM and the CUSUM SQUARE.Please how do i explain( interpret) a model without trend and constant? also the ECM was -0.03( annual data was used which was in log form), i hope it is a good ECM. Thank You.

Hi David, kindly check other online resources for the interpretation as I have never estimated any model without a constant.

Dear Maam, in 4:57 if my variable shows lag 3 then should I exactly write for instance d(rexch(-3)) or to write d(rexch(-1)) d(rexch(-2)) d(rexch(-3)) ? thank you

Hi Ariesta, use the 2nd spec. Thanks.

Hello. Big fan.

Why haven’t you taken the first differences in the long run model specification? You have just used the data at level?

Hi Kanishka, the long-run is assumed to be a stable-state. Hence, it is denoted by a "level" relationship.

Dear madam, once again thank you very much for the highly informative video. In the end of the video you refer to the cusum and cusumsq tests to assess the stability of the model. However, if the model appears to breach the 5% boundary in either the cusum or the cusumsq test, what would you advise as a general approach? Many thanks

Hi Owen, thanks for the positive feedback. Deeply appreciated! If that is the case, perform a structural break analysis. Kindly watch my video on "Chow Test for Structural Break" for guide. Regards.

@@CrunchEconometrix Dear Madam, I may be so blunt to ask for your help again. Following your advice I have included an exogenous dummy variable within my ARDL model for the structural break. However, when conducting the cusum and cusumsq tests, I find that the test reveals only the timespan for the period after the structural break. Have you come across this issue and would you know how to overcome it? Many thanks!

The important thing is if the line lies within the 95% bounds...that shows stability after controlling for a break in the model.

@@CrunchEconometrix Thank you for the quick response. So just to affirm, if the line remains within the 5% bounds for the period after the exogenous structural break, I can automatically assume that the period before the structural break which is not shown within the cusum test results is also within the 5% bounds?

You are unnecessarily complicating issues. This video is very clear and straightforward on what to do when there's a break point. Kindly watch again, thanks.

Thank you vert much.but dôme économiste think that the speed of adjustment must be negative but < to 1 .is there any thing to do about it ?

Hi Ganga, you can change your control variables and re-estimate.

Hello Ngozi,

Thank you for your informative videos.

I have two questions:

1. Do you have a reference (source) for the models you posted for the short run, long run and error correction model specifications?

2. Why aren't the contemporaneous regressors included in the models, only the lagged variables are included in all the models?

Hi Khadija, thanks for the positive feedback. Deeply appreciated. Since ARDL estimates are OLS estimates, you can always cite papers that used the ARDL methods. Also, only the lags of the regressors are included due to the way the equations are specified: i = 1 rather than from i = 0....may I know from where (location) you are reaching me? Thanks.

@@CrunchEconometrix I am from Kenya. what determines whether i=1 or i=0 is used? is one superior to the other?

Superiority is not in question here. Model estimation is derived from model specification. If you specify the model with i=0, that includes the contemporaneous regressor and i=1 implies without. it is as simple as that.

@@CrunchEconometrix my final question. If the coeffcicients in the longrun model are all insignificant, do you still use the residuals from this model in the ECM?

Khadija, you will agree with me that any estimation having ALL insignificant coefficients is meaningless. The golden rule is that, at least 50% of the coefficients must be statistically significant.

Hi ma'am. Thank you for your informative videos. my model is a bivariate one. can i use an alternative method to johansen such as bounds and then continue on with ardl and ecm?

Yes, you can.

CrunchEconometrix Thank you for your quick response. I would be greatful for your response to these further queries:

1.in determining optimal lag here you alternatively changed the exogenous and endogenous. Were these the optimal lag for each model? In here however th-cam.com/video/jtb_4fqxBZE/w-d-xo.html all the variables were input as endogenous. It does not seem to go with the method for determining optimal lag of each series either wherein there was no exogenous there.

2. what is the difference between vecm and ecm? Do i understand correctly vecm is for multivariate? My data is bivariate. I would like to estimate ardl and ecm directly(not thru ols) but i only seem to find vecm models tutorial mostly. Could u direct me if possible to a tutorial on direct estimate of ecm. I am studying 3 bivariate eqns(the independent is common in 2 of them).

3. what if i have serial correlation?

Hi Ran, please know that if questions on different videos are lumped up, I simply skip them. But know that ECM applies to ARDL while VECM applies to VAR. Also, watch any of my videos on diagnostics to understand "serial correlation". Thanks.

CrunchEconometrixNoted. Thank you so much for your time.

I am a bit confused. From the specification of the ARDL, there should be the summation of the explanatory variables from when t=0, but yours start from t=1. Even if the chosen lag length is 1, it means one should start from 0 to 1 and not just pluck in 1. Kindly clarify, i will appreciate.

Yes, rightly observed. I chose to omit the level of the regressors and start with their lags. Like I told others previously, you can model yours starting with the level of the regressors.

Firstly thank you for this video record.

I have a question which is I have 4 variables and after the BONDS test they are cointegrated. and I use the long-run coefficient ECM model. but all my answers ECM(-1) cof: -0.02

is it significant? if not can you give an example of a significant number

Hi Temur, which one are you referring to? Statistical or magnitude significance? I suggest to look up the difference between these concepts online. Thanks.

Hi, how can we interpret the numbers for the model at min 5:25, all p values are high, so what will be our conclusion here for this short run form model ?? Help please, I have the same case.. my thesis is about money demand

Ala, there is no short-run relationship since all the pvalues > 0.05.

Dear Ma’am, can we estimate the ARDL model without including the current values of the regressor? I am a big fan! Thank you so much for your informative videos, they helped a lot!!

Hi Aarya, advisable to include it. Thanks for the positive feedback. Deeply appreciated!

@@CrunchEconometrix thank you for your response Ma’am. Take care!

Mam can you tell me how to estimate short run coefficients under this..as I have to put it in a table??

Good day ma, can you please refer me to that your video where you talked about dummy variables? I can't find it again

I have videos on that. Kindly do a search within my Channel to locate them. Use "dummy" as the search word. Thanks.

Thank you so much mam for so prompt response 😊.

Mam we need to estimate ARDL Model for lnimp also in your example as there is cointegration or just we need to estimate only ECM

ARDL OLS model for short run relationship

Hi Ruchi, my explanations on what to do...and which I actually DID are quite clear. You may want to watch the video again.

What are you referring to?

Hi! Thanks you very much for your amazing posts! I am suffering from CUSUM. Here are my questions and your answers will be greatly appreciated! Case 1: CUSUM within range, but CUSUM SQ out of range (only a small part within range)? What does it mean? What should I do next?

Case 2: Both CUSUM and CUSUM SQ are out of range. I am actually quite shocked because the bound test has proved long-run relationship exists, while CUSUM and CUSUM SQ prove the relationship is not stable. In this case, should I just stop modeling at this step?