In the video, I referred to "swap tenor" as a synonym for the TERM or LIFE of the swap; in my example, the term is three (3) years. However, I should note that Hull defines tenor as the payment frequency period (in my example, six months). Further, it appears some authors say tenor could refer to either the TERM/LIFE of the swap, or the payment frequency period. Contrary to my video, I actually like Hull's approach because then we have two short words to refer to different features of the swap. Thank you!

how did they get all those changing libor rates. the first libor rate at september was 2.20 then in march it was 2.80 and after six months it was 3.30. how did they determine that change in the libor.

Thank you! "Plain vanilla IRS" refers to the illustrated (in the video) fixed-for-floating IRS, as in: one counterparty exchanges fixed (floating) rate in return for floating (fixed) rate. There are many variations. A variation is floating-for-floating (aka, basis swaps). Also, the payment timing (in the example, six months) does not need to match: one can pay quarterly and the other semi-annually. Also, the principal can vary over time (eg, amortize). Finally, a constant maturity swap (CSM) exchanges LIBOR for a swap rate. Thanks,

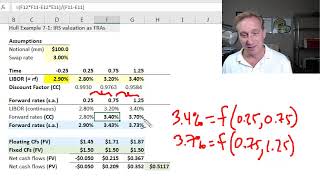

I think your detailed exemple at the end is a poor reflection of the case shown at the beginning. You are missing one additional column which is Float paid and is equal to LIBOR + 0,1%. The Net Cash Flow is also wrong since you are missing this big component.

When I spoke to motivation (see th-cam.com/video/c5CcH9Uvx_c/w-d-xo.html), I tried to explain that a firm may use the swap to transform a fixed-rate liability (borrowing) into a floating-rate obligation, or vice-versa. In my example, Ciitgroup "transforms" external fixed-rate borrowing (at 3.10%) into net floating rate of LIBOR + 0.12%. The company can also use the swap to transform assets (i.e., lending) from fixed-rate to floating rate, or vice-versa. Finally, my next video illustrates comparative advantage, which allows a company to actually improve its absolute interest rate.

For example, someone who recieve fix interest income wants change them into floating interest payment because he thing the intrest rate will rise. But for this "swap" he has to pay a price

In the video, I referred to "swap tenor" as a synonym for the TERM or LIFE of the swap; in my example, the term is three (3) years. However, I should note that Hull defines tenor as the payment frequency period (in my example, six months). Further, it appears some authors say tenor could refer to either the TERM/LIFE of the swap, or the payment frequency period. Contrary to my video, I actually like Hull's approach because then we have two short words to refer to different features of the swap. Thank you!

Which of hull's books does this reference ?

I would like to entitle you entire cities. Best on youtube for this kind of stuff. Thanks Sir.

how did they get all those changing libor rates. the first libor rate at september was 2.20 then in march it was 2.80 and after six months it was 3.30. how did they determine that change in the libor.

Easy to follow.

What does "plain vanilla" mean, and which other types of interest rate swaps are out there? Great video

Thank you! "Plain vanilla IRS" refers to the illustrated (in the video) fixed-for-floating IRS, as in: one counterparty exchanges fixed (floating) rate in return for floating (fixed) rate. There are many variations. A variation is floating-for-floating (aka, basis swaps). Also, the payment timing (in the example, six months) does not need to match: one can pay quarterly and the other semi-annually. Also, the principal can vary over time (eg, amortize). Finally, a constant maturity swap (CSM) exchanges LIBOR for a swap rate. Thanks,

thanks for added xlx file!

So is the idea that both parties expect interest rates to rise? Are they speculating on the direction of interest rates? Thanks.

I think your detailed exemple at the end is a poor reflection of the case shown at the beginning. You are missing one additional column which is Float paid and is equal to LIBOR + 0,1%. The Net Cash Flow is also wrong since you are missing this big component.

i must of missed it so what is the purpose of a interest rate swap

When I spoke to motivation (see th-cam.com/video/c5CcH9Uvx_c/w-d-xo.html), I tried to explain that a firm may use the swap to transform a fixed-rate liability (borrowing) into a floating-rate obligation, or vice-versa. In my example, Ciitgroup "transforms" external fixed-rate borrowing (at 3.10%) into net floating rate of LIBOR + 0.12%. The company can also use the swap to transform assets (i.e., lending) from fixed-rate to floating rate, or vice-versa. Finally, my next video illustrates comparative advantage, which allows a company to actually improve its absolute interest rate.

For example, someone who recieve fix interest income wants change them into floating interest payment because he thing the intrest rate will rise. But for this "swap" he has to pay a price

did not understand