if I have a negative NPV is this better for my US currency or worse : because the only way to get a negative NPV would be if we are paying a higher amount and receiving a lower amount giving me a negative premium. However other sources state that a negative premium/NPV value is in fact better for us as this means your premium as a cost will decrease by that much and therefore save you money. All in all my question is what does a negative NPV value mean good or bad for the US ? thank you

Should we not use the 110 as the basis for the forward exchange rate and then invert if necessary? The above implies that the yen is strengthening relative to the USD when USD interest rates are higher which is counter intuitive.

@@renzocrisologo5602 it's not swap inception (when PV = 0). Maybe the swap is two years old. Since inception, the FX rate has changed (and both interest rates may have changed). If the rates are unchanged, the implied initial USDJPY is ¥122.8 (i.e., PV = 0) not ¥120.0 b/c the rates aren't equal. The different spot rates and different interest rates give rise to some differential, but mostly it's explained by the fact the swap's current value is not zero: that means at least one of the three variables has changed, but the spot FX has the biggest impact.

You are a gifted teacher. Thank you for helping so many of us!

if I have a negative NPV is this better for my US currency or worse : because the only way to get a negative NPV would be if we are paying a higher amount and receiving a lower amount giving me a negative premium. However other sources state that a negative premium/NPV value is in fact better for us as this means your premium as a cost will decrease by that much and therefore save you money. All in all my question is what does a negative NPV value mean good or bad for the US ?

thank you

Should we not use the 110 as the basis for the forward exchange rate and then invert if necessary? The above implies that the yen is strengthening relative to the USD when USD interest rates are higher which is counter intuitive.

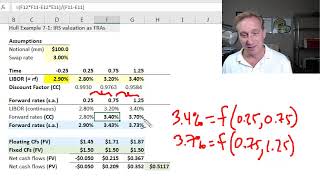

What exchange rates are the principal and interest flows made at?

can i have the excel worksheet?

Thank you sir.

Thanks, Sir.

whos the teacher in the video pls? Such a great teacher I needa thank you.

David from Bionic Turtle

USD 10 x exchange rate 110 isn't jpy 1,100? Why jpy 1,200?

The USD payer is paying 10 * $1.00 = $10.00, so the JPY is paying 10x the USDJPY which is quoted per $1.00 of the base USD

Exactly, but 110 x 10 equals 1,100 no 1,200. Othr way, pls can you shows the fórmula to get 1,200... Thksss

@@renzocrisologo5602 it's not swap inception (when PV = 0). Maybe the swap is two years old. Since inception, the FX rate has changed (and both interest rates may have changed). If the rates are unchanged, the implied initial USDJPY is ¥122.8 (i.e., PV = 0) not ¥120.0 b/c the rates aren't equal. The different spot rates and different interest rates give rise to some differential, but mostly it's explained by the fact the swap's current value is not zero: that means at least one of the three variables has changed, but the spot FX has the biggest impact.

Very clear! It was confusing but now I've learned the main variables change over the life of this contract. Thxs