Why give us a rise at all? Makes more sense to stop taxing us and removing our bus pass and heating allowance etc. Kier Starmers gvt is greedy and self centred especially when you think of all the allowances he, his wife and his gvt claim. We are his slaves

You cant get pension credits if you are on the new state pension, as it is £6.00 over the cut off, so no winter fuel, free glasses, free dentist, free council tax, reduced rate on water bill wifi bill. So the new state pensioners are worse off than the others, all for thr sake of 6 quid. Not fair at all.😮

mines due early nxt year i will recieve 221 a week is this the new pension or is it the old am not sure , what i do know is i been paying deductions since 1975 when i left school into work immediately nxt years my 50th of work

Just found you thanks. Am furious with a Labour government which has betrayed the Labour movement and attacked pensioners like this. I was one of the pensioners on the borderline so I couldn't get pension credit. I worked when I wasn't doing child care some of which was before the law entitling credits for child care duties. I had two pensions when it wasn't common, one for the NHS and local authority work and the other regular retirement pension. I was in a low paid area such as nursery nurse or NHS admin. Now having paid tax upon tax just to live, divorced without my own home, I am under attack again and am incredulous. Total corruption in UK governments of any followed by incompetence.

@@maxinelucas1104 only some pensioners. I’m ex of the NHS and an OAP. I can survive without the Winter allowances. Yes, it was welcome, but did I really need it? The Nation is in a dire state, and at some stage the new Government was going to have to make tough decisions. I’m pretty sure that those close to the cut off point, will not be neglected, if they truly aren’t coping.

Thanks for the informative and well balanced video. The informal chat setting was easy watching. The biggest pension change which concerns me is if the government decides to means test the state. As time goes on and the number of people with DC and DB pensions increase I feel it's a real possibility. What's your view? Paul

I think it is inevitable but will start at a high rate. For example people with more than £30k per year private pension will see a small reduction. Those over £60k private pension per year will get no state pension.

There has been talk of the potential for means testing the state pension, heaven forbid. I think this would go straight to the top of your list, although hopefully its unlikely due to the fallout it would create. I don't put anything past the current leadership however given recent decisions where clearly they didn't underake proper impact assessments.

It has become too difficult and too complicated to claim Winter Fuel allowance, especially when there are doubts over the eligibility to qualify. Let us have the "two tier" State Pension rectified instead, which would make the more senior [and the most vulnerable] pensioners on the old system over £50 per week better off. After all, it is these people who have paid in the most, 44+ years to fully qualify compared to 35 years as it is now!! Of course this Government would consider it to be too costly to equalize, despite the unfairness of the system.

What's unsaid is that auto-enrolled pension savers get a 3% contribution from their employer, in larger private sector companies that's typically 10%, whereas for the public sector it's more than double that - in the NHS it's 23.7%, Civil Service 26.6% to 30.3%, for firefighters 28.8%, and for teachers 28.68%. It's not just two tier policing, but two tier pensions. Plus those on private pensions not only have to fund their own, but also the public sectors workers' ones thru their taxes. And now it seems thru their own pension schemes being raided by government to give big payrises to public sector workers. No wonder the public sector Unions give generous gifts to Labour MPs.

When I worked as an internal auditor in the public sector, I knew I could move to the private sector and earn £10000 more for the exact same role. The better pension in the public sector balanced thing out to about even. I spent a third of my career in the public sector and two-thirds private sector. I would say they are comparable overall.

Nice balanced conversation - I enjoyed that. I retired 5 yrs ago at 55 so I share your concerns. Bringing DC pensions inside IHT is very likely - surprising it already hasn't happened. In addition to your list I think one that has been overlooked is the generous salary sacrifice system. This loses the Treasury monies from employees and employers NI payments. I'm not sure how much salary sacrifice costs but it would be relatively easy to do away with it. When working I gained lots from Salsac and also bunged in the max £40k limit into my DC pension for many years to reduce income tax. I also have concern that NI taxation may be brought to bear on DB and DC pension payments taken in retirement - but I don't think it would be applicable to state pension. My concern here is due to requiring older citizens to contribute more due to the ageing population and increased pressure on the NHS. Also wonder if some form of tax grab may be made on ISA's - hope not as I have significant investments in mine and my Mrs ISAs. Well done keep going with the channel - have subscribed.

If death in service benefits are not part of the estate I see no reason why passing on a pension should be, they are both ways of protecting dependents

@@Time2RetireUK I wasn't aware that the suggestion was that IHT would only apply to pensions that are "active" or even what that fully means, however, a significant number of dependents would still be present. The main one is their partner with, as of 2021 24% of couples in their 50s are not married or in a civil partnership. Some will have kids as well so a not insignificant portion have dependants and that portion is growing

I have saved all my life and have a big pot I am going to spend spend spend and gift my stuff to my daughter. Then I will sponge off the government like all the none tax paying lot do .no liebour government is getting my pot to spend on refugees

Hmmmm. If Labour go 'beserk' on pensions they will face a massive backlash - I'm sure they are aware of the need to tread warily. These are my thoughts: 1) IHT applying to pension funds. This is the lowest hanging fruit and, quite frankly, it's a loophole that should have been closed for some time. 2) Increased retirement age. This is already happening, with a rise to age 68 in 2046, but almost certainly to happen earlier, the question is how much earlier? My guess is 2038 or 2037. April 2035 would be the earliest, given the need to give at least 10 years of notice before this can happen, but I think any earlier than 2037 would cause a lot of anger. 3) Flat rate tax relief. The radicals in the Labour government want this, but there are issues associated with implementing this, and it would not work for those with salary sacrifice arrangements. Of course salary sacrifice could be abolished but this would be very controversial, causing massive inconvenience for employers. Flat rate tax relief would also be generationally unfair, as it would favour the oldest people close to retirement over younger age groups, who would be disadvantaged by flat rate tax relief. 4) Lowering or abolishing the tax free lump sum. Relatively low hanging fruit, but controversial, given that many people have made plans with this relief in mind. There would certainly be a backlash. I think it more likely that Labour will simply leave the maximum (currently £268k) frozen for years to come and let inflation do its job. 5) Winter fuel allowance. A serious issue for the poorest pensioners, but insignificant for many others. I never assumed this would go on forever, and frankly I'm a lot more concerned about keeping the triple lock. 6) Bringing NI onto DC and DB pensions. Highly controversial, given that this would negatively affect nearly everyone and break the principle that NI should not be chargeable on investment income. I don't see this as likely, despite some Labour radicals wanting it. 7) ISA changes. Low hanging fruit in my view, given that ISAs tend to be used by the wealthier sections of society. Pretty sure that, at the very least, there will be a limit on the maximum that can be kept in an ISA. Some people have said £100k, though I think £250k is more likely and would cause less of a backlash. I also think that the £20k maximum ISA contribution may be lowered, perhaps to £10k. That said, there is a possibility, though a relatively small one, that ISAs could be abolished altogether. That would save the government a fairly hefty sum, but would result in a strong backlash that could be hard to manage. 8) Lowering the maximum on yearly pension contributions. Currently, one can contribute a maximum of £60k a year into a pension and obtain tax relief. Obviously, this benefits the very highly paid, and, as such is low hanging fruit for Labour. I'm pretty sure this will be lowered to perhaps £40k, or even $30k, in order to reduce the tax loss. Much more likely to happen than introducing flat rate tax relief in my view. 9) Re-introducing a tax-free cap on pension funds. The Tories recently abolished the tax free cap on pension funds, allowing people like doctors to build up huge sums without being taxed. Labour had previously said that they would not reverse this change, but I'm sure they are reconsidering this. I believe the likelihood of a cap coming back has increased sharply since Labour won the election and would be surprised if this did not happen, though there might be some special measures to spare people like doctors. 10) CGT. Not directly relevant to pensions, but relevant to people who have used buy-to-let as a type of pension fund. CGT will rise for sure, and I think probably match income tax rates, with perhaps the tax free allowance being ditched altogether. 11) Means testing the state pension. This, apparently, is the system in Australia and a number of other countries. Means testing effectively means the abolition of the state pension, given that it would be removed from all but the poorest people. I don't think this will happen soon in the UK because it would be such a radical change, but it may happen in the longer term. There also high admin costs associated with administering and enforcing means testing. A more efficient approach might be to lower the 40% tax threshold for the over 65s from £50k to perhaps £40k. This would force better off pensioners to pay more tax, while not affecting the majority, but it would be strongly resisted by mostly public sector trade unions and professional bodies.

regarding question 4 after huge drops in transfer values i think they shouldn't go anywhere near this, db members have lost enough as it after the last goverment (Truss)messed up , im down 40 percent already and only 2 yrs to go if they do away with tax relief it will be a nightmare on my small pot 50 percent down in a few years i would probably have been better off at the bookies than investing or keeping db pension plans at the moment. its already been a disaster for many pensioner s who are retiring shortly. i also think these insurance companies insuring db schemes thru buyouts are also taking advantage of this and many people who are considering buyouts of thier schemes should be made aware of big insurance companys taking the piss with improper buyouts a pension scheme is run for the good of its members by the trustees whilst an insurance company is run for the company's owners shareholders a conflict of interests i believe

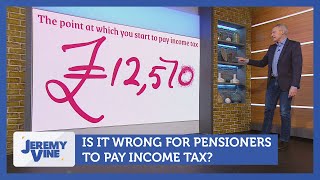

Government putting the basic pension up , is only taking it further past the threshold for claiming pension credit. Those on new state pension , without an extra private pension or extra income & paying rent , are totally banjaxed . They can’t claim pension credit & all the other extras it opens the door to, like rent & council tax rebate & other perks . A few poxy quid a week on the state pension next April , won’t even cover the rise on one household bill , let alone all the others including food . Pensioners shouldn’t be paying any tax, they paid more than enough the first time around when they earned the bunce or paid for stuff they own in the first place . The government & the clowns running it , have got a brass neck .

I have been paying in to a pension all my working life. Now 69 and retired 4 years , and have one fund not touched and was planning to take this in 5 more years ….. when one current fund expires to 0 then start the next and use the tax relief as part of the pension , if they reduce this to 100000 I will not be able to do this and will have a smaller pension as a result . And DB pensions have a similar problem as well and could end up with a smaller pension

All of your 5 points potentially affect me, but if im honest, some of these do make sense especially number 5 putting tax on inheritance tax makes sense. For my part if I lose out then so be it, it’s for the good of the country, then so be it. I wanted to be able to retire at 55, so might have to be 57 or even later, but I can’t complain I’m doing ok, and honestly I’d rather the people with more are taxed, than those with very little.

@@JamesKerr-z4o Thats fine as long as they take a hard look at those of working age on unemployment benefit too. We have had millions of people coming to this country who have found jobs. So the jobs were there. I bet a third of the “unemployed are either working on the black market or do not want to work. There could be billions saved there.Stop sending money abroad. More millions saved.

So if I am planning to pay off my 200K mortgage when I retire and the gov abolish the 25% tax free lump sum, does that mean that I will be charged 40% and 45% income tax on a large part of that 200K as it will be classed as income in that one year? So would I be better off to pay of my mortgage slowly each year and try to keep my annual income below the tax thresholds or increase my mortgage payments each year before retirement? What approach would be best?

In the theoretical position of there being no lump sum commencement relief you would be charged tax at your prevailing rate, so taking £200,000 out in the same year would incur a lot of tax.

Surely, since the recent DWP pensioner bank account snoop bill was introduced, they can see who is eligible for pension credit? The DWP can see income and expenses and work out if a person is eligible. They are quick to check bank accounts for benefit fraud but don't check eligibility for pension credits.

There will be people drawing their pensions and running a barber shop that only takes cash, and they pay themselves in cash. Checking bank accounts only goes so far.

There are some oddities about pensions. You get tax relief putting money, so should pay tax when you take money out. Retiring and not taking your money out so that money is sheltered from inheritance tax is against that principle. So while I understand protecting the money in a pension from inheritance tax while you are of working age. As the argument would be that your family will need that money after an untimely death. I think the 75 year is an odd cliff edge. I would as a halfway house reduce that cliff edge to 65. I think paying National Insurance on pensions is the most likely change. It raises by far the biggest amount of money, instantly. Most of the changes you raise do not guarantee raising a lot of money in this financial year. Income tax, National Insurance and VAT are the ways governments raise money. Relatively small changes in National Insurance by the last government created a £20 billion reduction in government income. I fully support that. The NI fund, is not just for state pensions. It also funds the NHS and working age benefits like maternity pay. £110 billion goes on state pensions and £45 billion on the NHS. Now while any age uses the NHS, it’s a fact that over 65s consume more NHS resources than other age groups. It also allows the government to increase NI take without breaking their pledge on not raising tax on working people. I think we need to address a lot of extra spending in care of the elderly. Especially on bed blocking. Where people are well enough to leave hospital, but not well enough to be at home. So the NHS needs to spend more to sort that out. If they take away the tax free allowance, that will be such a huge change it would undermine trust in pension savings. To fuel the growth economy. The government needs to encourage savings. As a nation we don’t save enough. Undermining the long established rules on how pensions work would be a disaster. It takes away trust in long term savings. Also it raises very little money. I can see a move to reducing it to say an easier to understand maximum if £250,000 or £200,000 as the politics is making those with the broader shoulders etc, and very few have £million in pension savings. One reason why scraping the tax free allowance raises relatively little.

Depending on the budget could determine if I bring my retirement early or keep on working. 55 due to retire at 60. I'm ready to down tools and spend my DC pension to 67.

I think pensions WILL be included for IHT purposes. I think they WILL bring in flat rate tax relief. I think the tax free lump sum allowance WILL be lowered. Hope they dont meddle with isa’s.

I don't believe flat rate tax relief will be introduced - this would affect overwhelmingly the younger age groups, given that people in their 50s will already have benefitted from the higher reliefs. They may get rid of the 45% income tax relief, but probably keep the 40% tax one. I also think that meddling with the tax free lump sum would be controversial, but they might do that anyway. ISAs I think will be changed for sure.

@@Time2RetireUK as long as they do not put a limit on what is allowed to be held in isa,s retrospectively as I have a reasonable amount being frugal for 3 decades. they may drop the limit going forward to say 10k in my opinion.

Also, I cannot see Rachael Thieves still allowing higher rate tax payers gaining 40+% into their pensions whilst taking away the winter fuel allowance for those well off.

This is very complicated, let’s suppose someone sacrifices 7% of their salary so their employer now pays 10% into their pension. How do you stop this? You could tax all employers contributions above 3% of the salary, but this not only impacts everyone who works for companies with more generous pensions but also everyone in the public sector. As an example the NHS pays in over 20% in to their employees pensions. Salary sacrifice is effectively giving 40% tax relief. Encouraging salary sacrifice not only loses 2% on taxing those on over £50,000, but the employer also saves 8%, so encouraging salary sacrifice potentially loses more money than it makes, due to loss of all these NI payments.

She supposedly wants to make everyone less dependent on the State, which means testing the Winter Fuel Allowance & State Pension would be in line with, but discouraging pensions saving would not.

Time frames are important - think of the WASPI women. I can see these being announced , but not to start for say 2 years or whatever. They will need to give people time to re-plan.

If you gave people notice that the tax free allowance was to be scrapped in April 2025, the withdrawals would crash the bond market, a bit like the Truss budget. They would have to do it from midnight the day before the budget.

@Time2RetireUK I agree , lots of people would try to retire all at once. That's why I suggested 2 years+ for example , not 6 months. Good talking points.

@sharoncross5371 So, what's all the fuss about those 800, 000 who currently don't claim it and now needing to fill in a 200+ point questionnaire to get it ? Also , you don't just ' get ' your pension at retirement age. You have to claim it. It's classed as a benefit.

To the 38% who voted for Labour, I hope you’re happy now !!!! Fact 38% of a 60% turnout, 20% of eligible voters. How did they get 65% of the seats in parliament, actually Corbyn got more votes in 2017 and possibly more in 2019

@@Time2RetireUK Sorry confused by your response, I thought the 25% is not connected to your tax allowance? Therefore you could take this and no tax payed.

Some years where I need a bit more cash, say kids wedding, I would like option to access some extra cash without suffering more tax. If I take it this year when I don't need it it won't ba available later. Also, the amount you can withdraw is a %. So the longer you leave it the more you can withdraw.

It really makes me laugh with everyone bashing Labour. Who caused all the problems we are in currently? It would be refreshing if most of the comments could be balanced.

How balanced do you need it to be? The "black hole" was created by labour. 9 billion in wage increases for pubkic sector workers, train drivers and 22% for junior doctors, who say they will accept it for now but will demand more, 11 billion for overseas climate control and aid. Their job is too balance our country's books not overseas, not blow our money away on illegal immigrants, asylum seekers etc, but no, let's bash the pensioners, and other vulnerable groups. Is that balanced enough for you, LABOUR OUT, LABOUR SUPPORTERS BIW YOUR HEADS IN SHAME.

![[LIVE] : ONE ลุมพินี 87 วันนี้!! คู่เอก "ก้องชัย vs โชคปรีชา"](http://i.ytimg.com/vi/YN6e7HVnekw/mqdefault.jpg)

They should give the pension increase now instead of April

I like that plan 👍

Why give us a rise at all? Makes more sense to stop taxing us and removing our bus pass and heating allowance etc. Kier Starmers gvt is greedy and self centred especially when you think of all the allowances he, his wife and his gvt claim. We are his slaves

You cant get pension credits if you are on the new state pension, as it is £6.00 over the cut off, so no winter fuel, free glasses, free dentist, free council tax, reduced rate on water bill wifi bill. So the new state pensioners are worse off than the others, all for thr sake of 6 quid. Not fair at all.😮

mines due early nxt year i will recieve 221 a week is this the new pension or is it the old am not sure , what i do know is i been paying deductions since 1975 when i left school into work immediately nxt years my 50th of work

@@doglover-t9b that's the new state pension...millions of pensioners are losing out...

Just found you thanks. Am furious with a Labour government which has betrayed the Labour movement and attacked pensioners like this. I was one of the pensioners on the borderline so I couldn't get pension credit. I worked when I wasn't doing child care some of which was before the law entitling credits for child care duties. I had two pensions when it wasn't common, one for the NHS and local authority work and the other regular retirement pension. I was in a low paid area such as nursery nurse or NHS admin. Now having paid tax upon tax just to live, divorced without my own home, I am under attack again and am incredulous. Total corruption in UK governments of any followed by incompetence.

Did u vote for them?

@@sharonhalliwell Of course she did. No doubt spent her Winter Fuel Payment on Xmas presents as well

It’s not fair pensioners are going to suffer this year Labour should do something about it

@@maxinelucas1104 only some pensioners. I’m ex of the NHS and an OAP. I can survive without the Winter allowances. Yes, it was welcome, but did I really need it? The Nation is in a dire state, and at some stage the new Government was going to have to make tough decisions. I’m pretty sure that those close to the cut off point, will not be neglected, if they truly aren’t coping.

Labourites are not going to do anything about it. They are crooks

Great video love the way you get it across by chatting 🥰

Thank you! 🤗

Thanks for the informative and well balanced video. The informal chat setting was easy watching.

The biggest pension change which concerns me is if the government decides to means test the state. As time goes on and the number of people with DC and DB pensions increase I feel it's a real possibility. What's your view?

Paul

I think it is inevitable but will start at a high rate. For example people with more than £30k per year private pension will see a small reduction. Those over £60k private pension per year will get no state pension.

few months ago the press were going on about the state pension age being increased to 71 by 2050

I am guessing the government would be looking to make some savings during the next 5 years to make a difference during their current term in office

They can raise the pension age but there’s no jobs in the uk lately for older people

Just found your channel. Great video thanks guys

Thanks for watching!

There has been talk of the potential for means testing the state pension, heaven forbid. I think this would go straight to the top of your list, although hopefully its unlikely due to the fallout it would create. I don't put anything past the current leadership however given recent decisions where clearly they didn't underake proper impact assessments.

Yes I have seen that. Just really don't think it will be happen yet. Australia do it though

It has become too difficult and too complicated to claim Winter Fuel allowance, especially when there are doubts over the eligibility to qualify. Let us have the "two tier" State Pension rectified instead, which would make the more senior [and the most vulnerable] pensioners on the old system over £50 per week better off. After all, it is these people who have paid in the most, 44+ years to fully qualify compared to 35 years as it is now!! Of course this Government would consider it to be too costly to equalize, despite the unfairness of the system.

This is the best idea yet

What's unsaid is that auto-enrolled pension savers get a 3% contribution from their employer, in larger private sector companies that's typically 10%, whereas for the public sector it's more than double that - in the NHS it's 23.7%, Civil Service 26.6% to 30.3%, for firefighters 28.8%, and for teachers 28.68%.

It's not just two tier policing, but two tier pensions. Plus those on private pensions not only have to fund their own, but also the public sectors workers' ones thru their taxes. And now it seems thru their own pension schemes being raided by government to give big payrises to public sector workers. No wonder the public sector Unions give generous gifts to Labour MPs.

When I worked as an internal auditor in the public sector, I knew I could move to the private sector and earn £10000 more for the exact same role. The better pension in the public sector balanced thing out to about even.

I spent a third of my career in the public sector and two-thirds private sector. I would say they are comparable overall.

Nice balanced conversation - I enjoyed that. I retired 5 yrs ago at 55 so I share your concerns.

Bringing DC pensions inside IHT is very likely - surprising it already hasn't happened.

In addition to your list I think one that has been overlooked is the generous salary sacrifice system. This loses the Treasury monies from employees and employers NI payments. I'm not sure how much salary sacrifice costs but it would be relatively easy to do away with it. When working I gained lots from Salsac and also bunged in the max £40k limit into my DC pension for many years to reduce income tax.

I also have concern that NI taxation may be brought to bear on DB and DC pension payments taken in retirement - but I don't think it would be applicable to state pension. My concern here is due to requiring older citizens to contribute more due to the ageing population and increased pressure on the NHS. Also wonder if some form of tax grab may be made on ISA's - hope not as I have significant investments in mine and my Mrs ISAs. Well done keep going with the channel - have subscribed.

Thanks for the sub. Great response 👍

If death in service benefits are not part of the estate I see no reason why passing on a pension should be, they are both ways of protecting dependents

"In service" suggests dependants need protection. Somebody leaving an active pension less so.

@@Time2RetireUK I wasn't aware that the suggestion was that IHT would only apply to pensions that are "active" or even what that fully means, however, a significant number of dependents would still be present. The main one is their partner with, as of 2021 24% of couples in their 50s are not married or in a civil partnership. Some will have kids as well so a not insignificant portion have dependants and that portion is growing

Public service pensions aren't funny that init

I have saved all my life and have a big pot I am going to spend spend spend and gift my stuff to my daughter. Then I will sponge off the government like all the none tax paying lot do .no liebour government is getting my pot to spend on refugees

Hmmmm. If Labour go 'beserk' on pensions they will face a massive backlash - I'm sure they are aware of the need to tread warily. These are my thoughts:

1) IHT applying to pension funds. This is the lowest hanging fruit and, quite frankly, it's a loophole that should have been closed for some time.

2) Increased retirement age. This is already happening, with a rise to age 68 in 2046, but almost certainly to happen earlier, the question is how much earlier? My guess is 2038 or 2037. April 2035 would be the earliest, given the need to give at least 10 years of notice before this can happen, but I think any earlier than 2037 would cause a lot of anger.

3) Flat rate tax relief. The radicals in the Labour government want this, but there are issues associated with implementing this, and it would not work for those with salary sacrifice arrangements. Of course salary sacrifice could be abolished but this would be very controversial, causing massive inconvenience for employers. Flat rate tax relief would also be generationally unfair, as it would favour the oldest people close to retirement over younger age groups, who would be disadvantaged by flat rate tax relief.

4) Lowering or abolishing the tax free lump sum. Relatively low hanging fruit, but controversial, given that many people have made plans with this relief in mind. There would certainly be a backlash. I think it more likely that Labour will simply leave the maximum (currently £268k) frozen for years to come and let inflation do its job.

5) Winter fuel allowance. A serious issue for the poorest pensioners, but insignificant for many others. I never assumed this would go on forever, and frankly I'm a lot more concerned about keeping the triple lock.

6) Bringing NI onto DC and DB pensions. Highly controversial, given that this would negatively affect nearly everyone and break the principle that NI should not be chargeable on investment income. I don't see this as likely, despite some Labour radicals wanting it.

7) ISA changes. Low hanging fruit in my view, given that ISAs tend to be used by the wealthier sections of society. Pretty sure that, at the very least, there will be a limit on the maximum that can be kept in an ISA. Some people have said £100k, though I think £250k is more likely and would cause less of a backlash. I also think that the £20k maximum ISA contribution may be lowered, perhaps to £10k. That said, there is a possibility, though a relatively small one, that ISAs could be abolished altogether. That would save the government a fairly hefty sum, but would result in a strong backlash that could be hard to manage.

8) Lowering the maximum on yearly pension contributions. Currently, one can contribute a maximum of £60k a year into a pension and obtain tax relief. Obviously, this benefits the very highly paid, and, as such is low hanging fruit for Labour. I'm pretty sure this will be lowered to perhaps £40k, or even $30k, in order to reduce the tax loss. Much more likely to happen than introducing flat rate tax relief in my view.

9) Re-introducing a tax-free cap on pension funds. The Tories recently abolished the tax free cap on pension funds, allowing people like doctors to build up huge sums without being taxed. Labour had previously said that they would not reverse this change, but I'm sure they are reconsidering this. I believe the likelihood of a cap coming back has increased sharply since Labour won the election and would be surprised if this did not happen, though there might be some special measures to spare people like doctors.

10) CGT. Not directly relevant to pensions, but relevant to people who have used buy-to-let as a type of pension fund. CGT will rise for sure, and I think probably match income tax rates, with perhaps the tax free allowance being ditched altogether.

11) Means testing the state pension. This, apparently, is the system in Australia and a number of other countries. Means testing effectively means the abolition of the state pension, given that it would be removed from all but the poorest people. I don't think this will happen soon in the UK because it would be such a radical change, but it may happen in the longer term. There also high admin costs associated with administering and enforcing means testing. A more efficient approach might be to lower the 40% tax threshold for the over 65s from £50k to perhaps £40k. This would force better off pensioners to pay more tax, while not affecting the majority, but it would be strongly resisted by mostly public sector trade unions and professional bodies.

regarding question 4 after huge drops in transfer values i think they shouldn't go anywhere near this, db members have lost enough as it after the last goverment (Truss)messed up , im down 40 percent already and only 2 yrs to go if they do away with tax relief it will be a nightmare on my small pot 50 percent down in a few years i would probably have been better off at the bookies than investing or keeping db pension plans at the moment. its already been a disaster for many pensioner s who are retiring shortly. i also think these insurance companies insuring db schemes thru buyouts are also taking advantage of this and many people who are considering buyouts of thier schemes should be made aware of big insurance companys taking the piss with improper buyouts a pension scheme is run for the good of its members by the trustees whilst an insurance company is run for the company's owners shareholders a conflict of interests i believe

Great post. Thanks for your considered answer 👍

@@Time2RetireUK Just my tuppence worth's. Hopefully it will provide food for thought.

Government putting the basic pension up , is only taking it further past the threshold for claiming pension credit. Those on new state pension , without an extra private pension or extra income & paying rent , are totally banjaxed . They can’t claim pension credit & all the other extras it opens the door to, like rent & council tax rebate & other perks . A few poxy quid a week on the state pension next April , won’t even cover the rise on one household bill , let alone all the others including food . Pensioners shouldn’t be paying any tax, they paid more than enough the first time around when they earned the bunce or paid for stuff they own in the first place . The government & the clowns running it , have got a brass neck .

I have been paying in to a pension all my working life. Now 69 and retired 4 years , and have one fund not touched and was planning to take this in 5 more years ….. when one current fund expires to 0 then start the next and use the tax relief as part of the pension , if they reduce this to 100000 I will not be able to do this and will have a smaller pension as a result . And DB pensions have a similar problem as well and could end up with a smaller pension

10 days and things will be clearer following the budget

All of your 5 points potentially affect me, but if im honest, some of these do make sense especially number 5 putting tax on inheritance tax makes sense.

For my part if I lose out then so be it, it’s for the good of the country, then so be it. I wanted to be able to retire at 55, so might have to be 57 or even later, but I can’t complain I’m doing ok, and honestly I’d rather the people with more are taxed, than those with very little.

@@JamesKerr-z4o Thats fine as long as they take a hard look at those of working age on unemployment benefit too.

We have had millions of people coming to this country who have found jobs. So the jobs were there.

I bet a third of the “unemployed are either working on the black market or do not want to work.

There could be billions saved there.Stop sending money abroad. More millions saved.

I think that they could also slash the annual allowance of £60,000 to £40,000 pa. That should be easy to administer!

Yes that would be straightforward and could bring in quite a lot. You may be on to something 🤔

Can't see how your number 1 is the biggest risk, what about talk of means testing the state pension itself ? nightmare !

So if I am planning to pay off my 200K mortgage when I retire and the gov abolish the 25% tax free lump sum, does that mean that I will be charged 40% and 45% income tax on a large part of that 200K as it will be classed as income in that one year? So would I be better off to pay of my mortgage slowly each year and try to keep my annual income below the tax thresholds or increase my mortgage payments each year before retirement? What approach would be best?

In the theoretical position of there being no lump sum commencement relief you would be charged tax at your prevailing rate, so taking £200,000 out in the same year would incur a lot of tax.

@@Time2RetireUK Exactly. So my Q was what is best strategy to use re. paying off a 200K mortgage.

Worth seeing a solicitor. Maybe.

If this government done tax-free allowance then they would be doing the dirty on the unions and civil servants that they have just tucked up too

i wonder if they will lift the 30000 threshold for financial advise afterall after inflation has now taken it upto 35000 in todays terms

I doubt it. People can be tricked into selling a defined benefit pension into a defined contribution pension too easily.

Surely, since the recent DWP pensioner bank account snoop bill was introduced, they can see who is eligible for pension credit? The DWP can see income and expenses and work out if a person is eligible.

They are quick to check bank accounts for benefit fraud but don't check eligibility for pension credits.

There will be people drawing their pensions and running a barber shop that only takes cash, and they pay themselves in cash. Checking bank accounts only goes so far.

There are some oddities about pensions. You get tax relief putting money, so should pay tax when you take money out. Retiring and not taking your money out so that money is sheltered from inheritance tax is against that principle. So while I understand protecting the money in a pension from inheritance tax while you are of working age. As the argument would be that your family will need that money after an untimely death. I think the 75 year is an odd cliff edge. I would as a halfway house reduce that cliff edge to 65.

I think paying National Insurance on pensions is the most likely change. It raises by far the biggest amount of money, instantly. Most of the changes you raise do not guarantee raising a lot of money in this financial year. Income tax, National Insurance and VAT are the ways governments raise money. Relatively small changes in National Insurance by the last government created a £20 billion reduction in government income.

I fully support that. The NI fund, is not just for state pensions. It also funds the NHS and working age benefits like maternity pay. £110 billion goes on state pensions and £45 billion on the NHS. Now while any age uses the NHS, it’s a fact that over 65s consume more NHS resources than other age groups. It also allows the government to increase NI take without breaking their pledge on not raising tax on working people. I think we need to address a lot of extra spending in care of the elderly. Especially on bed blocking. Where people are well enough to leave hospital, but not well enough to be at home. So the NHS needs to spend more to sort that out.

If they take away the tax free allowance, that will be such a huge change it would undermine trust in pension savings. To fuel the growth economy. The government needs to encourage savings. As a nation we don’t save enough. Undermining the long established rules on how pensions work would be a disaster. It takes away trust in long term savings. Also it raises very little money. I can see a move to reducing it to say an easier to understand maximum if £250,000 or £200,000 as the politics is making those with the broader shoulders etc, and very few have £million in pension savings. One reason why scraping the tax free allowance raises relatively little.

Depending on the budget could determine if I bring my retirement early or keep on working. 55 due to retire at 60. I'm ready to down tools and spend my DC pension to 67.

I hope you get to retire early. You can't buy back time 🤞

I think pensions WILL be included for IHT purposes.

I think they WILL bring in flat rate tax relief.

I think the tax free lump sum allowance WILL be lowered.

Hope they dont meddle with isa’s.

I don't believe flat rate tax relief will be introduced - this would affect overwhelmingly the younger age groups, given that people in their 50s will already have benefitted from the higher reliefs. They may get rid of the 45% income tax relief, but probably keep the 40% tax one. I also think that meddling with the tax free lump sum would be controversial, but they might do that anyway. ISAs I think will be changed for sure.

In what way do you think isa’s will be changed.

Well the British ISA has been scrapped, and i think the limit won't change from £20k. Not sure what else will change. Do you have any thoughts?

@@Time2RetireUK as long as they do not put a limit on what is allowed to be held in isa,s retrospectively as I have a reasonable amount being frugal for 3 decades.

they may drop the limit going forward to say 10k in my opinion.

Also, I cannot see Rachael Thieves still allowing higher rate tax payers gaining 40+% into their pensions whilst taking away the winter fuel allowance for those well off.

This is very complicated, let’s suppose someone sacrifices 7% of their salary so their employer now pays 10% into their pension. How do you stop this?

You could tax all employers contributions above 3% of the salary, but this not only impacts everyone who works for companies with more generous pensions but also everyone in the public sector. As an example the NHS pays in over 20% in to their employees pensions.

Salary sacrifice is effectively giving 40% tax relief.

Encouraging salary sacrifice not only loses 2% on taxing those on over £50,000, but the employer also saves 8%, so encouraging salary sacrifice potentially loses more money than it makes, due to loss of all these NI payments.

She supposedly wants to make everyone less dependent on the State, which means testing the Winter Fuel Allowance & State Pension would be in line with, but discouraging pensions saving would not.

Who’s going to give migrants a pension more importantly

Time frames are important - think of the WASPI women. I can see these being announced , but not to start for say 2 years or whatever. They will need to give people time to re-plan.

If you gave people notice that the tax free allowance was to be scrapped in April 2025, the withdrawals would crash the bond market, a bit like the Truss budget. They would have to do it from midnight the day before the budget.

@Time2RetireUK I agree , lots of people would try to retire all at once. That's why I suggested 2 years+ for example , not 6 months. Good talking points.

As far as I can remember, you automatically get the Winter Fuel Allowance in the year you receive your state pension. You don’t have to claim it.

@sharoncross5371 So, what's all the fuss about those 800, 000 who currently don't claim it and now needing to fill in a 200+ point questionnaire to get it ? Also , you don't just ' get ' your pension at retirement age. You have to claim it. It's classed as a benefit.

To the 38% who voted for Labour, I hope you’re happy now !!!!

Fact 38% of a 60% turnout, 20% of eligible voters. How did they get 65% of the seats in parliament, actually Corbyn got more votes in 2017 and possibly more in 2019

Tempted to get my 25% of one of my pensions this month, hopefully that will not be counted to the new limited amount

I'm leaving mine until I come to a year when my tax position is better placed to take advantage of it.

@@Time2RetireUK Sorry confused by your response, I thought the 25% is not connected to your tax allowance? Therefore you could take this and no tax payed.

Some years where I need a bit more cash, say kids wedding, I would like option to access some extra cash without suffering more tax. If I take it this year when I don't need it it won't ba available later. Also, the amount you can withdraw is a %. So the longer you leave it the more you can withdraw.

Zelensky laughing all the way to the bank.

It really makes me laugh with everyone bashing Labour.

Who caused all the problems we are in currently?

It would be refreshing if most of the comments could be balanced.

How balanced do you need it to be? The "black hole" was created by labour. 9 billion in wage increases for pubkic sector workers, train drivers and 22% for junior doctors, who say they will accept it for now but will demand more, 11 billion for overseas climate control and aid. Their job is too balance our country's books not overseas, not blow our money away on illegal immigrants, asylum seekers etc, but no, let's bash the pensioners, and other vulnerable groups. Is that balanced enough for you, LABOUR OUT, LABOUR SUPPORTERS BIW YOUR HEADS IN SHAME.

He does that, their will be riots.

Riots are generally started by the under 40s. The under 40s think gen X and boomers have stolen their future. They'll be celebrating in the streets

Your numbers 2 to 5 will not harm the vast majority of pensioners.

Let's hope not

They WILL harm the vast majority of people preparing and saving to retire!

Not a very happy video.

Let's hope Things Can?

Only Get.

Better Let's hope Kia.

Remembers this song and the whole hope it Inspired

I am optimistic in the medium term 👍