The problem I have with most of my professors is that they dont try to convey or intrepret the problem practically and just stick to finding patterns in problems and finding the solutions. But you sir, has made my interest spark in economics even more by literally convincing me that any problem in economics can be solved by just just a fraction of your common sense and some basic formulas. I am so glad I found you on youtube. Once again thank you soo much sirr

I taught exactly similiar concepts to my students of engineering economics... compounding was less frequent than payments.... One of my student was discussing another way of solving it..." give simple interest to the amount when there was no compounding , and after a quarter, give compound interest... I was looking for some reference...your video helped ...thanks

Thanks for your great videos. One question, is it not better if we use an effective monthly rate? (because we have monthly deposits). Here, you combined every three-month $500 into once. As we have monthly compounding on it can we simply sum those $500?! I calculated with a monthly compounding rate and considered the period as 12*10 = 120 months, but the final answer is not the same as yours. I appreciate if you could help regarding this, Thanks!

This problem is illustrating how to deal with cash flows that occur MORE frequently than the compounding period. The point of the example is to show at you MUST simple add the dollar amounts of the payments together since there are no interest calculations occuring at the time of the payments...so it is correct to simply add the numbers. Watch the video again and listen to the explanation very carefully. The video is correct. Perhaps the purpose of the video is what is unclear?

I get you, because the video is using a lump sum approach (assuming the bank does nothing with the first 2 installments of each quarter), but some other models, like yours probably, require you to convert the less frequent compounding period interest rate to what is called an "effective monthly interest rate", which the bank applies to every monthly payment despite say a quarterly or semi-annually compounding period. They are two distinct calculations; which one applies to your course really depends on the lecturer.

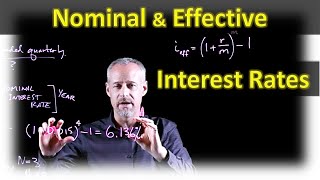

Thank you for a great explanation. I wonder why we used the nomial interest rate and not the effective one? when should I use one over the other? Thank you

Good question. In this problem, we are in fact using the 'effective' interest rate. The 'nominal' rate is quoted as 10% compounded quarterly, meaning the effective quarterly rate is 2.5% - this comes from the conventions for how rates are quoted. This can be confusing for students! I suggest you watch my video on "Nominal and Effective Interest Rates" and also my video on "Compounding More Frequent than Payments" - each of these videos has an example problem that should help you understand when (and how) to interpret this whole interest-rate-business! Good luck!

Ha! Your question challenges the conventions of nominal and effective interest rates. We typically never have a compounding period longer than 1 year. BUT, just for fun, if we assume the word 'nominal' still refers to a 1-year timeframe (a reasonable assumption), then I think you could simply use a rate of 14% when you do the interest calculations every 2-years. If you back-calculate an 'effective' yearly rate the question you would ask is, "what effective yearly rate compounded twice would give 14% ?"... Perhaps the answer is 6.77% ? [ i.e. (1 + 0.0677)^2 -1 = 0.14 ] Others should feel free to comment on this!! Thanks for the interesting question.

Mike borrowed 200,000 at 5% compounded quarterly and agreed to pay on a monthly basis for 5 years. How much is the monthly payment? the choices are 50, 499.13 50, 499.31 40, 499.13 40, 499.31 but as I solved it the way you explained 3(200,000) = A ( (1 + 0.05/4)^4(5) - 1) / (1 + 0.05/4)^4(5) (0.05/4) ) A = is not in the choices why??

So... your problem is quite different from this video, and more complicated. I would interpret the problem like this: 5% compounded quarterly means an effective yearly rate of [(1+(0.05/4))^4 - 1] = 5.0945337% Find the monthly rate that gives the same effective yearly rate as above by taking the 12th-root of 1.050945337 - i.e. (1+0.050945337)^(1/12) - 1 = 0.4149425% Now use the equation for A/P for N=60 (5yrs x 12months), and i = 0.004149425, and P = $200,000 [the equation for A/P is [(i*(1+i)^N)/((1+i)^N-1))] A = P * (A/P, i, N) for the above values A = 200000 * 53.017333 = $3,772.35 *** this is the answer for the monthly payments. I'm sorry to say that none of the answers you were given as choices make sense...It's always good to do a quick reality-check on your numbers. If someone borrows $200,000 and makes monthly pmts for 5-years (60-months), then their payments should be somewhere in the range of $3,333+some effect for the interest (just do $200,000/60 to get a general idea of the magnitude); so $3,772.35 seems like it is about right given the effects of compound interest.

Unfortunately this approach uses a simplifying assumption that making a $500 per month deposit is the same as making a $1,500 deposit per quarter and that's wrong. It ignores the time value of money of the $500 deposits made before a compounding event. The yield of these two investments would be different. The APY of the former would actually be less because of the interim-quarter deposits that don't earn anything. You can prove this by using an equivalency test to an instrument that is otherwise the same but compounds monthly.

Jon, thanks for the comment. The purpose of the video is to demonstrate what happens when interest is compounded quarterly. There is no interest accumulated on the monthly deposits until you reach the end of a quarter. What you're saying is true when the interest rate is compounded monthly. I'm confident the video is correct for its intended purpose.

The problem I have with most of my professors is that they dont try to convey or intrepret the problem practically and just stick to finding patterns in problems and finding the solutions. But you sir, has made my interest spark in economics even more by literally convincing me that any problem in economics can be solved by just just a fraction of your common sense and some basic formulas. I am so glad I found you on youtube. Once again thank you soo much sirr

Thank you for the wonderful comment. I'm glad you like my videos. Good luck in your course!

You teach it so much better than my professors!!! Thank you!!! Great explanations with all the reasonings and how to do it

Glad it was helpful!

I taught exactly similiar concepts to my students of engineering economics... compounding was less frequent than payments....

One of my student was discussing another way of solving it..." give simple interest to the amount when there was no compounding , and after a quarter, give compound interest...

I was looking for some reference...your video helped ...thanks

Glad my video was helpful!

reviewing this topic for Exam FM. Thanks for the explanation. Good work!

Most welcome!

Thank you for the explanations, professor, it was very helpful!

You're welcome!

very professional work, thanks

Glad you liked it!

Thanks for your great videos. One question, is it not better if we use an effective monthly rate? (because we have monthly deposits). Here, you combined every three-month $500 into once. As we have monthly compounding on it can we simply sum those $500?! I calculated with a monthly compounding rate and considered the period as 12*10 = 120 months, but the final answer is not the same as yours. I appreciate if you could help regarding this, Thanks!

This problem is illustrating how to deal with cash flows that occur MORE frequently than the compounding period. The point of the example is to show at you MUST simple add the dollar amounts of the payments together since there are no interest calculations occuring at the time of the payments...so it is correct to simply add the numbers. Watch the video again and listen to the explanation very carefully. The video is correct. Perhaps the purpose of the video is what is unclear?

I get you, because the video is using a lump sum approach (assuming the bank does nothing with the first 2 installments of each quarter), but some other models, like yours probably, require you to convert the less frequent compounding period interest rate to what is called an "effective monthly interest rate", which the bank applies to every monthly payment despite say a quarterly or semi-annually compounding period. They are two distinct calculations; which one applies to your course really depends on the lecturer.

Thank you for a great explanation. I wonder why we used the nomial interest rate and not the effective one? when should I use one over the other? Thank you

Good question. In this problem, we are in fact using the 'effective' interest rate. The 'nominal' rate is quoted as 10% compounded quarterly, meaning the effective quarterly rate is 2.5% - this comes from the conventions for how rates are quoted. This can be confusing for students! I suggest you watch my video on "Nominal and Effective Interest Rates" and also my video on "Compounding More Frequent than Payments" - each of these videos has an example problem that should help you understand when (and how) to interpret this whole interest-rate-business! Good luck!

@@EngineeringEconomicsGuy Thank you so much for getting back to me.

no problem!

Thank you so much 😊

You're welcome 😊

If the compounding period is 2 years, the nominal interest rate is 7%, what is the effective interest rate? Thank you so much for your video!

Ha! Your question challenges the conventions of nominal and effective interest rates. We typically never have a compounding period longer than 1 year. BUT, just for fun, if we assume the word 'nominal' still refers to a 1-year timeframe (a reasonable assumption), then I think you could simply use a rate of 14% when you do the interest calculations every 2-years. If you back-calculate an 'effective' yearly rate the question you would ask is, "what effective yearly rate compounded twice would give 14% ?"... Perhaps the answer is 6.77% ? [ i.e. (1 + 0.0677)^2 -1 = 0.14 ] Others should feel free to comment on this!! Thanks for the interesting question.

Would like to take your help for a small question...because I dont see any of my concepts getting applied to that ...if you can , let me know

You can contact me at eeconomicsguy@gmail.com

this guy is so frickin cool

Thank you sir .

You're welcome! Good luck in your course.

very helpful !! thanks

No problem!

Thanks a lot sir!

You're welcome! Good luck in your course!

Thank you so much

You're most welcome

Mike borrowed 200,000 at 5% compounded quarterly and agreed to pay on a monthly basis for 5 years. How much is the monthly payment?

the choices are

50, 499.13

50, 499.31

40, 499.13

40, 499.31

but

as

I solved it the way you explained

3(200,000) = A ( (1 + 0.05/4)^4(5) - 1) / (1 + 0.05/4)^4(5) (0.05/4) )

A = is not in the choices

why??

So... your problem is quite different from this video, and more complicated. I would interpret the problem like this:

5% compounded quarterly means an effective yearly rate of [(1+(0.05/4))^4 - 1] = 5.0945337%

Find the monthly rate that gives the same effective yearly rate as above by taking the 12th-root of 1.050945337 - i.e. (1+0.050945337)^(1/12) - 1 = 0.4149425%

Now use the equation for A/P for N=60 (5yrs x 12months), and i = 0.004149425, and P = $200,000

[the equation for A/P is [(i*(1+i)^N)/((1+i)^N-1))]

A = P * (A/P, i, N) for the above values

A = 200000 * 53.017333 = $3,772.35 *** this is the answer for the monthly payments.

I'm sorry to say that none of the answers you were given as choices make sense...It's always good to do a quick reality-check on your numbers. If someone borrows $200,000 and makes monthly pmts for 5-years (60-months), then their payments should be somewhere in the range of $3,333+some effect for the interest (just do $200,000/60 to get a general idea of the magnitude); so $3,772.35 seems like it is about right given the effects of compound interest.

**Sorry the one line should read: A = 200000 / 53.01733 or A = 200000 * 0.018862

sir, do you have an fb page where i can send you pictures of my solutions, thank you😁

I don't do Facebook but you can send me an email eeconomicsguy@gmail.com

Unfortunately this approach uses a simplifying assumption that making a $500 per month deposit is the same as making a $1,500 deposit per quarter and that's wrong. It ignores the time value of money of the $500 deposits made before a compounding event. The yield of these two investments would be different. The APY of the former would actually be less because of the interim-quarter deposits that don't earn anything. You can prove this by using an equivalency test to an instrument that is otherwise the same but compounds monthly.

Jon, thanks for the comment. The purpose of the video is to demonstrate what happens when interest is compounded quarterly. There is no interest accumulated on the monthly deposits until you reach the end of a quarter. What you're saying is true when the interest rate is compounded monthly. I'm confident the video is correct for its intended purpose.

hmm