I forgot to explicitly say in the video: the v(i) shown in the MLE equation is identical to the GARCH variance; i.e., v(i) = σ^2(i). The u^2(i) should be familiar as the daily return-squared (which, as mentioned, I suggest thinking of as simply a one-day variance). Also, Analytics Vidhya just happen to post a good on MLE (albeit this is not GARCH specific): trtl.bz/2Lctz19 ... if you find a great MLE tutorial article, please do share!

I see that this example deals with just one asset, the s&p 500 index. What if I am observing a portfolio of 3 or more risky assets, how do I go about setting up the MLE model?

That’s too easy of a question…using excel simply set the objective to “Max” subject to 3 constraints… 1) the yellow cells should be able to change 2) the weights equal 1 3) the weights should all be positive values

I forgot to explicitly say in the video: the v(i) shown in the MLE equation is identical to the GARCH variance; i.e., v(i) = σ^2(i). The u^2(i) should be familiar as the daily return-squared (which, as mentioned, I suggest thinking of as simply a one-day variance). Also, Analytics Vidhya just happen to post a good on MLE (albeit this is not GARCH specific): trtl.bz/2Lctz19 ... if you find a great MLE tutorial article, please do share!

Hi Sir how u determine de Raw values for the Omega, Beta and Alpha? Is there a calibration or its just a theoric number?

Curious how you calculate the variance in cell E9 = D8*D8 Why don't you use E9 = VAR.P(D8, D9) ??

Sir,How you got the Omega,Beta and Alpha values please reply me

I see that this example deals with just one asset, the s&p 500 index. What if I am observing a portfolio of 3 or more risky assets, how do I go about setting up the MLE model?

Awesome video found it very helpful

Bro just casually carries my bachelor thesis

I used to solver on my data set. Is it normal to get an omega of exactly 0? Would that matter in estimating volatility?

Thank you so much, Sir. Your channel is a blessing.

How to forecast volatility then?

How did you get the likelihood?

Please mention all constraints to be used in solver clearly.

That’s too easy of a question…using excel simply set the objective to “Max” subject to 3 constraints…

1) the yellow cells should be able to change

2) the weights equal 1

3) the weights should all be positive values

@@investwithvincent6329 Might be for you. But was difficult for me back then.

Variance or Variance estimate?

Hi my friends. I have a one questions: whats is the meaning of alpha and beta adding 1 ?? (this is not the case with this video)

thank you very much !

Thank you for watching!

Superb

hello guys please how do we calculate alfa and beta

Oh my. You ve saved my life. Thank you!!

Are you able to share the solver password? Thank you.

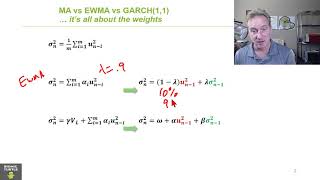

GARCHs explain the volatility with ... the volatility

Sir please share the link for excel file.

Link to XLS begins the description (see above), here also trtl.bz/2NlLn7d

Alpha +Beta should be less than one, in your example it was greater than one

it helps to listen to the video (yellow are rescaled "user friendly" values): beta 0.910121 + alpha 0.083390 < 1.0

I think it should be added as a constraint when use solver