TH-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, help me stay online.

Hi Meena, uni = one, bi = two and multi = many. Eg analyzing the impact of oil prices on its past behavior is a Univariate model, impact of oil prices on stock prices is a Bivariate model while analyzing the impact of oil prices on stock prices, exchange rates, interest rate etc is a Multivariate model. Your research objective determines which one you want to use.

@@CrunchEconometrix mam as i want to study the relationship of foreign investment purchase, sale with the stock returns....than in which category will it be considered as i have to applyVAR model. than do i need to put all variables collectively to decide lag length for VAR and again need to put variables collectively in endogenous column to run VAR model. or i should study firstly return and purchase than return and sale. please guide mam....

Hi Meena, watch my videos on VAR and ARDL to technique is applicable to your research objectives. Understanding, the technique is very useful in the arrangement of the variables in the model.

Your concise and appropriate videos have taught me Stata and now Eviews. Thank you so much for your efforts. You have helped me to pass my Post-graduation degree and more.😄🤗

First of all, thank you very much for your videos very understandable. I would have a question. I'm predicting VECM, but the problem of changing variance and autocorrelation arises. What should I do.

Hello Prof thanks for the video. i want to ask when testing for joint significant using wald test is it possible we test for all the variable in one model. maybe c1=c2=c3=c4=0. can we trust this? thank you

Incredible - thank you so much for such a straightforward video. Is it an issue if the coefficients are individually insignificant, but jointly significant via the F test?

Thanks for the kind remarks on my video, deeply appreciated! Even if the F-stat is significant, your results will be trashed if all the coeffs are statistically not significant. They imply the inability to refute the underlying null hypotheses. The rule-of-thumb is that at least 50% of the coeffs must be statistically significant.

Prof, thank you for help having this channel. It has helped me a lot in understanding econometrics and time analysis concept and both its basic and advance. I have a question, you concluded base on the DW that no serial correlation but in essence, model with lags using DW to decide for serial correlation is misleading. i would agree with you are using it in this case without strong affirmation of it presence.

Hi! First thing first thanks a lot for such insightful videos about VAR, this has been helping my thesis a lot. However I have question, when it’s sure that the data are first difference level... isn’t it supposed to be using type of d for estimating the VAR? Like d(...) but you wrote the variables in original one without d(...). I hope you will help as I’m confused which one is correct:”) thanks a lot!! 🤍

Hi Afifah, thanks for the encouraging feedback...deeply appreciated. Either approach is correct I explained that in my introductory VAR video (I advise you watch it). Kind regards.

Thx for confirming! I have another question, hope u will be kind to reply again.. so the optimum lag suggested by AIC SC and all is 1... however using 1, there is hereroskedasticity. Then I use lag 2, everything’s perfect! But my question is... how can I adjust my argument that 2 is best optimal lag while eviews output obviously showing 1?

Thank you so much. All the videos were helpful. Please do I test for residual diagnostics from my final VAR result with the p value or from the VAR result with the t-statistics?

Hi Judith, thanks for the positive feedback on my videos. Deeply appreciated! You can use either. Please, may I know from where (location) you are reaching me?

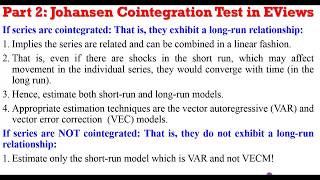

Hi, Thanks for the excellent video. I have seven variable model. Suppose, if i run unit root and found some independent variable are only stationary at first difference, while remaining are stationary at both level and first difference. So, in that situation, can i run Johansen Conintegration using all variable. So, is it compulsury for Johansen Cointegration that all variables should be at first difference, not mix. Hoping for your answer soon. Regards.

Hello In the VAR model results when you obtain the probability value and one of the dependent variable is suffering from serial correlation what should I do or what is the implication of that dependent variable.

Please in the interpretation of VAR model results when the constant C is statistical significance with the variables under the consideration how do you interpret it.

Hi Mohd, the constant basically has no interpretation. It is the intercept of the model. Interpretation: it the value of the depvar when the regressors are zero.

Hi Madam if my optimal lag selection to run VAR model is 1, and i want to search for shortrun relationship between the variables, can i use Wald test? or just check individual significance of the variable in the equation is enough?

Hi Abby, I'll say that "individual significance of the variable in the equation is enough" because VAR is for short-run analysis....may I know from where (location) you are reaching me?

I am in great confusion. I have 6 variables and they are cointegrated which means I have to use vecm model but the Problem is that my 4 variables has unit root at level but 2 variables has no unit root at level. I want to know can I convert all 6 variables to stationary at 1st difference and after that I can perform vecm model to do analysis? Please help me!!!

@@CrunchEconometrix I will use vecm. But I want to understand about my unit root issue. Can i convert stationary and non stationary variables (level) to 1st difference and reject the unit root test null hypothesis and then perform vecm..

TH-cam recently changed the way my content will be monetised. My channel now needs 1,000 subscribers. So it would be amazing if you show your support by both watching my videos and subscribing to my channel if you haven’t done so already. Monetising my videos allows me to invest back into the channel with some new equipment so this small gesture from you will be extremely huge for me. Many thanks for your support….CrunchEconometrix loves to teach, help me stay online.

@cruncheconometrics mam i have confusion about the bivariate and multivariate VAR. in which condition we do apply both models plz guide...

Hi Meena, uni = one, bi = two and multi = many. Eg analyzing the impact of oil prices on its past behavior is a Univariate model, impact of oil prices on stock prices is a Bivariate model while analyzing the impact of oil prices on stock prices, exchange rates, interest rate etc is a Multivariate model. Your research objective determines which one you want to use.

@@CrunchEconometrix mam as i want to study the relationship of foreign investment purchase, sale with the stock returns....than in which category will it be considered as i have to applyVAR model. than do i need to put all variables collectively to decide lag length for VAR and again need to put variables collectively in endogenous column to run VAR model. or i should study firstly return and purchase than return and sale. please guide mam....

Hi Meena, watch my videos on VAR and ARDL to technique is applicable to your research objectives. Understanding, the technique is very useful in the arrangement of the variables in the model.

YOU ARE THE BEST! Thank you so much for this amazing and informative channel.

Wow, thank you so much...happy to help!

Excellent, clear series of lectures. Very useful, thank you.

Thanks, Ravi for your encouraging feedback. Deeply appreciated!🥰🙏

Your concise and appropriate videos have taught me Stata and now Eviews. Thank you so much for your efforts. You have helped me to pass my Post-graduation degree and more.😄🤗

Great to hear, Purabi...we need to celebrate this. Congratulations!

tried to find how to make p-values for var and almost gave up... You're THE BEST!

U're welcome, Ivan! 🥰

You are just the best. So explicit. Your lectures are my help here.

Hahahaha, good to hear that my videos are helpful, Musa. Kindly share my Channel link with your students, friends and academic networks. Thanks!💕

Thank you so much Mam ,, you had made the interpretation of model so simple and clear .. thanks alot

Hi Priyanka, thanks for the encouraging feedback. Deeply appreciated! Made my day :). Please may I know from where you are reaching me?

I am from India😊

Thank you

God bless you.

you are doing a great job. keep it up

It's my pleasure, Mohd...thanks!

Great videos! Very clear! Very useful!

Glad it was helpful, Gaston...thanks!

Thank you very much

First of all, thank you very much for your videos very understandable. I would have a question. I'm predicting VECM, but the problem of changing variance and autocorrelation arises. What should I do.

Thanks for encourage feedback, ÇAĞATAY...estimate the model at higher-order lags.

Hello Prof thanks for the video. i want to ask when testing for joint significant using wald test is it possible we test for all the variable in one model. maybe c1=c2=c3=c4=0. can we trust this? thank you

Yes, Kilian you can. Thanks

Incredible - thank you so much for such a straightforward video. Is it an issue if the coefficients are individually insignificant, but jointly significant via the F test?

Thanks for the kind remarks on my video, deeply appreciated! Even if the F-stat is significant, your results will be trashed if all the coeffs are statistically not significant. They imply the inability to refute the underlying null hypotheses. The rule-of-thumb is that at least 50% of the coeffs must be statistically significant.

Prof, thank you for help having this channel. It has helped me a lot in understanding econometrics and time analysis concept and both its basic and advance.

I have a question, you concluded base on the DW that no serial correlation but in essence, model with lags using DW to decide for serial correlation is misleading. i would agree with you are using it in this case without strong affirmation of it presence.

Hi Abideen, thanks for the encouraging feedback. Deeply appreciated!

hi, thanks i have 5 variables 4 I(0) and the last I(1) can i estimate with var ?

or i make FIRST DIFFERENCE TO the 4 ?

or i make another model ?

Watch my videos on time series ARDL.

Hi kindly tell me the advantages of PANEL VAR over other available methodologied

Hi Shazia, you may need to check other online resources for that information. Thanks.

I do get benefit from this excellent video

Thanks for the positive feedback, Jasem. Glad to be of help. Please share my Channel link with your students and academic networks...thanks!

Hi! First thing first thanks a lot for such insightful videos about VAR, this has been helping my thesis a lot. However I have question, when it’s sure that the data are first difference level... isn’t it supposed to be using type of d for estimating the VAR? Like d(...) but you wrote the variables in original one without d(...). I hope you will help as I’m confused which one is correct:”) thanks a lot!! 🤍

Hi Afifah, thanks for the encouraging feedback...deeply appreciated. Either approach is correct I explained that in my introductory VAR video (I advise you watch it). Kind regards.

Thx for confirming! I have another question, hope u will be kind to reply again..

so the optimum lag suggested by AIC SC and all is 1... however using 1, there is hereroskedasticity. Then I use lag 2, everything’s perfect! But my question is... how can I adjust my argument that 2 is best optimal lag while eviews output obviously showing 1?

Simple Afifah. Just put a note in your text indicating what you did.

Thank you so much. All the videos were helpful. Please do I test for residual diagnostics from my final VAR result with the p value or from the VAR result with the t-statistics?

Hi Judith, thanks for the positive feedback on my videos. Deeply appreciated! You can use either. Please, may I know from where (location) you are reaching me?

Thanks for your response. I live in Jos

Hi, Thanks for the excellent video. I have seven variable model. Suppose, if i run unit root and found some independent variable are only stationary at first difference, while remaining are stationary at both level and first difference. So, in that situation, can i run Johansen Conintegration using all variable. So, is it compulsury for Johansen Cointegration that all variables should be at first difference, not mix. Hoping for your answer soon. Regards.

Hi Muhd, in this case the JCT is not applicable but the Bounds Cointegration test. Kindly watch my videos on ARDL and Bounds procedure.

Hello

In the VAR model results when you obtain the probability value and one of the dependent variable is suffering from serial correlation what should I do or what is the implication of that dependent variable.

Serial correlation will not affect a variable but ALL variables in the VAR system. Estimate the model at higher-order lags.

Please in the interpretation of VAR model results when the constant C is statistical significance with the variables under the consideration how do you interpret it.

Hi Mohd, the constant basically has no interpretation. It is the intercept of the model. Interpretation: it the value of the depvar when the regressors are zero.

This is good.

What is the meaning of an error message "near singular matrix" when I try to perform Johansen cointegration?

There is multicollinearity in the data. Watch my video on "Multicollinearity" on how to resolve the problem.

@@CrunchEconometrix Thanks..

Hi Professor,

How can I interpret VAR results, if my lagged variables are in first difference of log?

A percentage change in X causes Y to change by Z%, on average, ceteris paribus.

Thank you

You're welcome, Mohd! Please may I know from where (location) you are reaching me?

Hi Madam

if my optimal lag selection to run VAR model is 1, and i want to search for shortrun relationship between the variables, can i use Wald test? or just check individual significance of the variable in the equation is enough?

Hi Abby, I'll say that "individual significance of the variable in the equation is enough" because VAR is for short-run analysis....may I know from where (location) you are reaching me?

I am in great confusion. I have 6 variables and they are cointegrated which means I have to use vecm model but the

Problem is that my 4 variables has unit root at level but 2 variables has no unit root at level.

I want to know can I convert all 6 variables to stationary at 1st difference and after that I can perform vecm model to do analysis?

Please help me!!!

Maneesh, the procedures for ARDL, VAR, VECM techniques are well explained. Kindly watch them to know the most applicable to your study. Thanks.

@@CrunchEconometrix I will use vecm. But I want to understand about my unit root issue. Can i convert stationary and non stationary variables (level) to 1st difference and reject the unit root test null hypothesis and then perform vecm..

@@maneesh123777 Please follow the guides shown in my VECM videos. Thanks.

I want to have all your videos on econometric. where can I get them?

They are in 9 playlists.

Could you make one Video on the SVAR model with dummy and restrictions?

No idea yet about SVAR but it's included in my todolist. Thanks for the suggestion, grateful!

Madam

all my variables are stationary at level. can i run VAR? and what will be the lag length since they are both stationary.

Not VAR. Just OLS. I have a video on that. Kindly watch it.

Ghana