Thanks a bunch man. My finance prof's always assume that ALL their students know how to use financial calc's; and therefore, they don't explain how to use it. Your video really helped me. thnx

Thank you for the quick and simple tutorial. I was trying to figure out how to calculate the bond yield using the bond worksheet instructs in the manual. Great job!

Dextose: To use the IRR function, data must be entered into the calculator's cash-flow worksheet. Hit CF on the second row. To clear the worksheet, hit 2nd CLR WRK. Enter the bond's price as a negative in the CFO field (remember to hit Enter). Hit the down arrow and enter the semiannual coupon payment into C01 (Enter). Then enter the bond's maturity times 2 minus 1 in the FO1 field (Enter). Finally, enter 1,000 plus the coupon payment into CO2. Hit IRR, CPT and multiply the answer by 2.

How can I solve this type of problem using the IRR function? My teacher solved it this way in class for some reason. I'm not sure how would I would incorporate the bond's price into that function. Thanks ^_^

A 7 year $10,500 bond paying a coupon rate of 5.50% compounded semi-annually was purchased at 98.30. Calculate the yield at the time of purchase of the bond. how do i calculate it? the answer my assignment gave me was 5.80%

This video shows the significance of P/Y (payments per year) for bond value calculation. This only got my calculator to show the expected value. All other videos just ignore P/Y, resulting in weird values.

Because in investing you will not always be working to find the yield for a coupon bond. Often, investors are considering yields of other things, such as T-Bills, short-term notes, and mortgages. Whatever works best for you, but the chances of errors may be reduced if in the long run you train yourself to input the time periods for "n" (such as 30 years * 12 payments per year for mortgages) and then multiply the interest rate at the end by the same number of time periods you used for "n" (in the example I used, you would multiply your I/Y answer by 12 months) to convert for the annual rate. This is true especially if you are a finance student when exams require you to think the problem through by determining the appropriate cash flows, time periods, and number of payments.

the current market price of the bond is the Present value of the cash flows that it will generates you can find that out fairly easily if you know the market interest of a identical instrument

Andrew this has to be given to you, so yea he just pulled the number out of thin air. Otherwise you'd have two independent unknowns, yield rate and face value.

Nice video, but as Ladislav poitned out, it's recommended to NOT set P/Y = 2. CLR TVM does not reset this, and while I can't speak for other exams, you sure as hell don't want to under stress forget to change P/Y in the middle of the actuarial FM exam (where time is a huge commodity)! So just keep P/Y = 1 and use 30 for the number of payments.

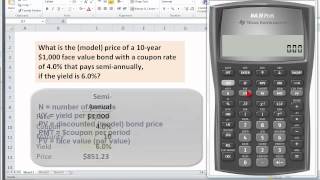

***** as mentioned in the video, bonds pay interest semi-annually. So as we multiplied N x2 and PMT/2.. we will multiply the I/Y value we get (5%) by 2 to get the 10%.

This is probably the best video on the subject out on the internet. Thank you for taking the time to help!

Thanks a bunch man. My finance prof's always assume that ALL their students know how to use financial calc's; and therefore, they don't explain how to use it. Your video really helped me.

thnx

Thank you for the quick and simple tutorial. I was trying to figure out how to calculate the bond yield using the bond worksheet instructs in the manual. Great job!

R u alive

thx dawg, my test tomorow will probably go well because of you!

your the man..huge help on a exam pre test problem.. keep up the good work

Thank you, now I understand what is happening in class

Thank you for simple explanation

Thank you. You really helped me with my test. Thank you again

You are a life saver! Amazing! Thank you thank you thank you!!!!!!!!!!

No wonder I couldn't figure it out! Thank you so much :)

simple but really clear that is help me a lot ! Thank you

Thanks! I was having a hard time computing it on my new BAII Plus.

Great help ! Thanks. Adding you to LinkedIn

thanks a lot! You saved my life!!!

generally, yes. this is the convention used on the CFA exam as the majority of US fixed income instruments pay coupons semi annually

you make it super easy, thank you :)

Este video me cambio la vida! This video changes my life =)

Thank you very much!

Great video, thank you!

Thanks so much for this video

Dextose:

To use the IRR function, data must be entered into the calculator's cash-flow worksheet. Hit CF on the second row. To clear the worksheet, hit 2nd CLR WRK. Enter the bond's price as a negative in the CFO field (remember to hit Enter). Hit the down arrow and enter the semiannual coupon payment into C01 (Enter). Then enter the bond's maturity times 2 minus 1 in the FO1 field (Enter). Finally, enter 1,000 plus the coupon payment into CO2. Hit IRR, CPT and multiply the answer by 2.

that's what i needed to know tysm

Brilliant video :)

Thanks a lot, still valid

How can I solve this type of problem using the IRR function? My teacher solved it this way in class for some reason. I'm not sure how would I would incorporate the bond's price into that function. Thanks ^_^

OMG!!!!!!! Thank you so much!!!!!!!

thanks, helped a lot!!!

thank you. very much appreciated :)

Thank you so much!!!!!

A 7 year $10,500 bond paying a coupon rate of

5.50% compounded semi-annually was purchased

at 98.30. Calculate the yield at the time of purchase of the bond.

how do i calculate it? the answer my assignment gave me was 5.80%

This video shows the significance of P/Y (payments per year) for bond value calculation. This only got my calculator to show the expected value. All other videos just ignore P/Y, resulting in weird values.

i don't think u should change p/y to 2

why?

Because in investing you will not always be working to find the yield for a coupon bond. Often, investors are considering yields of other things, such as T-Bills, short-term notes, and mortgages. Whatever works best for you, but the chances of errors may be reduced if in the long run you train yourself to input the time periods for "n" (such as 30 years * 12 payments per year for mortgages) and then multiply the interest rate at the end by the same number of time periods you used for "n" (in the example I used, you would multiply your I/Y answer by 12 months) to convert for the annual rate. This is true especially if you are a finance student when exams require you to think the problem through by determining the appropriate cash flows, time periods, and number of payments.

good point thanks

Excellent

life saver!!

I don't get how you get the price 615.69? you just pulling out this number of thin air?

the current market price of the bond is the Present value of the cash flows that it will generates you can find that out fairly easily if you know the market interest of a identical instrument

Andrew this has to be given to you, so yea he just pulled the number out of thin air. Otherwise you'd have two independent unknowns, yield rate and face value.

Nice video, but as Ladislav poitned out, it's recommended to NOT set P/Y = 2. CLR TVM does not reset this, and while I can't speak for other exams, you sure as hell don't want to under stress forget to change P/Y in the middle of the actuarial FM exam (where time is a huge commodity)! So just keep P/Y = 1 and use 30 for the number of payments.

nice

i took pv as -ve am still getting 4.999 =(

I keep getting 5 % as my answer

Did you change the P/Y to 2? Thats the problem I had too at first.

***** as mentioned in the video, bonds pay interest semi-annually. So as we multiplied N x2 and PMT/2.. we will multiply the I/Y value we get (5%) by 2 to get the 10%.

You made mistake by changing I/Y to 2.

thug life ain't ez

Awesome video! Thanks