Thanks Professor. Very well thought-out and interesting. You should compare this valuation to the many others that are done appropriately by the investment bankers, so that we can understand the difference between this version, and something that's a bit better - perhaps still not perfect, but better.

Wow, thank you so much, what a wonderful summary on this carnival of financial perversions... the only viable way forward may be "Teslabucks" credits for free recharges for holders of Mod3 deposits, sold at a discount. For the sake of vertical integration, and synergy, these can be produced at low cost in house. Anybody that's good for an $1K deposit on a non-existent car is good for some free future recharges for that car. So that may be a viable way of funding this folly. At least I can't think of any other.

Great investigative work, love to see the inside of how IB work. Thanks for the lesson. But is this a 1off scenario because of the Musk relationship in both business's and this was just an exercise in order to go through the process and get it done, I assume his isn't standard. How many SC investors are TSLA investors, bet you a lot..

Thanks for speaking out. This bad joke of a merger is based on one thing, the word of a charismatic CEO that he will find synergies selling products together, but the problem is that same CEO has a huge conflict of interest. He is way too leveraged in his investment in both companies. So much so that he has no alternative but to buy into solar city's failure to bail himself out. The investment banks did such a poor job because they just want to collect their fees for tamping it YES without incriminating themselves -"we're not criminal, just stupid!".

Do Tesla's largest shareholders (e.g. T. Rowe Price, Fidelity) scrutinize these assumptions? If they do and approve the merger, what would their reasons for doing so be?

How much of the criticism would you apportion to be Investment Banking specific, and how much would you apportion to be attributable to the BoD conflicts of interest? I fully agree that the IB critiques are correct, and it has always been a matter of "paid to promote" for this industry. However the real concern is when the BoD attempts to subvert and obfuscate the real value. I also believe that your assumption that there is no valid increased revenue expectation to be an important point for debate. TSLA offers international distribution channels in 40 different countries, whereas currently SCTY are only present in 22 states of the USA, and in Mexico. With the combined TSLA & SCTY companies becoming a single entity, the merged company will be able to offer off-grid energy solutions independent of local regulations and/or subsidies, and hence the addressable market for SCTY increases by a very large multiple.

Why do you assume that a merged company would make off grid energy solutions independent from local regulations? Also, what is the "off-grid energy solution" that the merged company provides?

Hi msfkl, The off-grid solution is SCTY panels and TSLA battery storage, although this is currently referred to as "distributed grid" as regulations do impose themselves. However, I think that once a plurality of households are able to produce and consume their own electricity, that the connected house will become optional and/or resisted as an unnecessary expense. It is supposition I grant you, but I can't see how the regulators will be able to justify forcing consumers to be part of the centralised grid or even part of a distributed grid, unless they offer the households an actual financial incentive for making their energy production available to others.

TL;DW version: investment bank valuations are BS, and if necessary, those valuations can be stretched well past the point of believability. Investment banks will tell any story they have to in order to facilitate a deal, because they get a piece of it.

Also funny to read some of the criticisms in the comments now that this merger has played out. The rosy BS projections of synergy and control turn out to be exactly that.

Aswath, funny you mention doing mischief and hiding it in a valuation by being clever. you've certainly got experience with someone doing this in their blog's laughably low balling estimates of Tesla's valuation.

The criticism in the video completely ignores the strategic reasons for the deal and is misguided. The simple fact is, SolarCity is worth more to its shareholders as part of Tesla vs. standalone valuation. In a similar way, Tesla is worth more to its shareholders if SolarCity is a successful enterprise, for many reasons. In addition, there's nothing wrong with using ranges. Although I agree that fairness opinions are almost always gamed, the purpose of a fairness opinion is to conclusively determine if a deal is not "not fair," not to determine if it is fair or not, as concluding that it is fair is to declare that valuation is an exact science, which it isn't, but academics cannot admit that, because otherwise they'd be out of a job. Prof. Damodaran is making the same mistakes he made with Amazon. I'd be happy to meet, off the record, and argue against pretty much every key point in this video.

No question at all that Solar City stockholders love this deal. You do realize that the fairness opinion that Evercore is offering is for Tesla shareholders, right? And ranges are a cop out. Distributions are not.

+Aswath Damodaran I'll take the opposite side on the terminal growth rate criticism. 6-8% growth is lower than it should be as I expect tesla to grow double digits at least until 2025. So they should've done a 10-year DCF with a global GDP growth rate in the terminal value calculation. Of course depending on margin assumptions, I would expect that a 20% annual top-line growth until 2025 combined with a 5% global growth rate will produce a higher NPV than a 5-year DCF with 6-8% terminal growth assumption in 2020, because by the time we get to 2025, cash flows are discounted to almost nothing anyway. Also, the video does not distinguish between if the terminal growth rate and discount rate assumptions are nominal or real.

The video does not ignore strategic reasons and is not misguided. The very purpose of a fairness opinion is to put all relevant factors into an all comprising format and then assess. As indicated in the video, synergies are the monetary manifestation of "strategic reasons" for a deal, why combined both companies are worth more than standalone or in fact any other benefits of a combination - if it's not in the numbers, it does not exist. On ranges: the ranges are extraordinary by any standard, to an extent that it renders the value of such opinion a lot less relevant. I am surprised such wide a ranges passed the internal fairness-opinion committees at Evercore and Lazard.

Solar city is a downward trending company with no ways of generating revenue as federal subsidies dried up. Without some help(Acquisition) It would have collapsed in the near future. This is a bad deal as it now puts Tesla in a disadvantage, while other competitors electric vehicles are about to hit the market.

6-8% ? Are they seriouse? Do they give any reasons for this, i mean... that´s ludicrous.

Thanks Professor. Very well thought-out and interesting. You should compare this valuation to the many others that are done appropriately by the investment bankers, so that we can understand the difference between this version, and something that's a bit better - perhaps still not perfect, but better.

Wow, thank you so much, what a wonderful summary on this carnival of financial perversions... the only viable way forward may be "Teslabucks" credits for free recharges for holders of Mod3 deposits, sold at a discount. For the sake of vertical integration, and synergy, these can be produced at low cost in house. Anybody that's good for an $1K deposit on a non-existent car is good for some free future recharges for that car. So that may be a viable way of funding this folly. At least I can't think of any other.

Great investigative work, love to see the inside of how IB work. Thanks for the lesson. But is this a 1off scenario because of the Musk relationship in both business's and this was just an exercise in order to go through the process and get it done, I assume his isn't standard. How many SC investors are TSLA investors, bet you a lot..

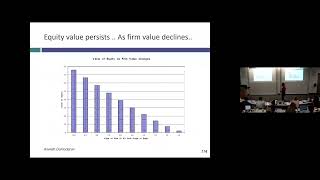

88 to 302?? Jeeze the variance in value per share is crazy.

Thanks for speaking out. This bad joke of a merger is based on one thing, the word of a charismatic CEO that he will find synergies selling products together, but the problem is that same CEO has a huge conflict of interest. He is way too leveraged in his investment in both companies. So much so that he has no alternative but to buy into solar city's failure to bail himself out. The investment banks did such a poor job because they just want to collect their fees for tamping it YES without incriminating themselves -"we're not criminal, just stupid!".

Do Tesla's largest shareholders (e.g. T. Rowe Price, Fidelity) scrutinize these assumptions? If they do and approve the merger, what would their reasons for doing so be?

Been Waiting for something like this for a long time!! 6-8% TGR? LOL

Wow! Didn't know it was this bad.

I am super curious of how do you find this kind of information?

Great video Dr Damodaran!!!!

Thanks Professor, great insight and entertaining to listen to.

I hope you were meaning "With all the greatest respect for the doorman in my building"

yes as a former investment banker... this is so true its painful

How much of the criticism would you apportion to be Investment Banking specific, and how much would you apportion to be attributable to the BoD conflicts of interest?

I fully agree that the IB critiques are correct, and it has always been a matter of "paid to promote" for this industry. However the real concern is when the BoD attempts to subvert and obfuscate the real value.

I also believe that your assumption that there is no valid increased revenue expectation to be an important point for debate. TSLA offers international distribution channels in 40 different countries, whereas currently SCTY are only present in 22 states of the USA, and in Mexico. With the combined TSLA & SCTY companies becoming a single entity, the merged company will be able to offer off-grid energy solutions independent of local regulations and/or subsidies, and hence the addressable market for SCTY increases by a very large multiple.

Why do you assume that a merged company would make off grid energy solutions independent from local regulations? Also, what is the "off-grid energy solution" that the merged company provides?

Hi msfkl,

The off-grid solution is SCTY panels and TSLA battery storage, although this is currently referred to as "distributed grid" as regulations do impose themselves.

However, I think that once a plurality of households are able to produce and consume their own electricity, that the connected house will become optional and/or resisted as an unnecessary expense.

It is supposition I grant you, but I can't see how the regulators will be able to justify forcing consumers to be part of the centralised grid or even part of a distributed grid, unless they offer the households an actual financial incentive for making their energy production available to others.

Wonderful!

TL;DW version: investment bank valuations are BS, and if necessary, those valuations can be stretched well past the point of believability. Investment banks will tell any story they have to in order to facilitate a deal, because they get a piece of it.

Great video sir!! Learnt a lot from you!! Keep posting..

Thanks for the education!

Also funny to read some of the criticisms in the comments now that this merger has played out. The rosy BS projections of synergy and control turn out to be exactly that.

great work professor!

Great vid.

Great Video Professor !!

great video, very educational!

Aswath, funny you mention doing mischief and hiding it in a valuation by being clever. you've certainly got experience with someone doing this in their blog's laughably low balling estimates of Tesla's valuation.

Insane !!!

great work, subscribed for me

The criticism in the video completely ignores the strategic reasons for the deal and is misguided. The simple fact is, SolarCity is worth more to its shareholders as part of Tesla vs. standalone valuation. In a similar way, Tesla is worth more to its shareholders if SolarCity is a successful enterprise, for many reasons. In addition, there's nothing wrong with using ranges. Although I agree that fairness opinions are almost always gamed, the purpose of a fairness opinion is to conclusively determine if a deal is not "not fair," not to determine if it is fair or not, as concluding that it is fair is to declare that valuation is an exact science, which it isn't, but academics cannot admit that, because otherwise they'd be out of a job. Prof. Damodaran is making the same mistakes he made with Amazon. I'd be happy to meet, off the record, and argue against pretty much every key point in this video.

No question at all that Solar City stockholders love this deal. You do realize that the fairness opinion that Evercore is offering is for Tesla shareholders, right? And ranges are a cop out. Distributions are not.

+Aswath Damodaran I'll take the opposite side on the terminal growth rate criticism. 6-8% growth is lower than it should be as I expect tesla to grow double digits at least until 2025. So they should've done a 10-year DCF with a global GDP growth rate in the terminal value calculation. Of course depending on margin assumptions, I would expect that a 20% annual top-line growth until 2025 combined with a 5% global growth rate will produce a higher NPV than a 5-year DCF with 6-8% terminal growth assumption in 2020, because by the time we get to 2025, cash flows are discounted to almost nothing anyway. Also, the video does not distinguish between if the terminal growth rate and discount rate assumptions are nominal or real.

The video does not ignore strategic reasons and is not misguided. The very purpose of a fairness opinion is to put all relevant factors into an all comprising format and then assess. As indicated in the video, synergies are the monetary manifestation of "strategic reasons" for a deal, why combined both companies are worth more than standalone or in fact any other benefits of a combination - if it's not in the numbers, it does not exist. On ranges: the ranges are extraordinary by any standard, to an extent that it renders the value of such opinion a lot less relevant. I am surprised such wide a ranges passed the internal fairness-opinion committees at Evercore and Lazard.

Solar city is a downward trending company with no ways of generating revenue as federal subsidies dried up. Without some help(Acquisition) It would have collapsed in the near future. This is a bad deal as it now puts Tesla in a disadvantage, while other competitors electric vehicles are about to hit the market.

@@yamantasdivarCOVID m🎉f