Mortgages explained UK

ฝัง

- เผยแพร่เมื่อ 13 ก.ค. 2024

- This video is your need-to-know guide to mortgages. Wrap your head around the basics, learn about interest charges and compare which mortgage or mortgage scheme is the right one for you. Find out more - www.finder.com/uk/mortgages

00:00 Introduction

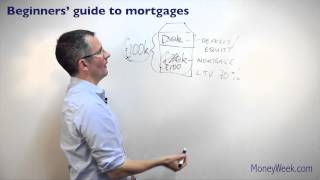

00:39 The mortgage essentials

02:26 Interest charges

03:31 Types of mortgages and schemes

04:32 Mortgage jargon explained

Extra resources:

95% mortgage scheme 👉 www.finder.com/uk/low-deposit...

Help to buy mortgage scheme 👉 www.finder.com/uk/help-to-buy

Shared ownership mortgages 👉 www.finder.com/uk/shared-owne...

#mortgagesuk #homeowner #propertyuk

Thank you. As someone new to this, these are good clear explanations.

Glad you found the video helpful!

Same😅

This is useful, thank you. There are so many annoying points when buying a property, but I guess I just have to accept things for the way they are 😂 If I mortgage, I feel like I need to find the longest fix rate scheme they have to protect myself from rising prices - I only want to buy an apartment or something similiar in the £50-90K bracket because I might be able to pay off the property within 10 years 😅 I hope I can pull it off in the future, I feel like it's so risky investing in a house for 20+ years

Thank you for this!x

Thank you😁

I like your way to explain. Awesome 👌

Thanks a lot 😊 Glad you found the video helpful!

Thanks

kudos,for making mortgage looks so simple to understand🎉

Glad you found the video helpful! 😊

American here - It's crazy that you can't get a fixed interest loan for the life of the mortgage like we do over here with 30year fixed rate loans. Sounds like a scam to me. Also, why would anyone want an interest only loan for a primary residence, I'm so lost. I hope you guys can lobby for 30year fixed rate loans. Great video!

Yip that our life here in the UK the government and the banking system milking every penny from the working class and lining there pockets and giving the rest to alcoholics and drug users

Being 16 i would of neevr thought i'd be sdat here learning aboutall this so im prepared for the future as well as understanding credit score insurance taxes the rest never thought i'd be motivated to learn this stuff that i would call boring lol

It's never too early to learn about how to manage your money well. Glad you're enjoying learning about all this stuff 💪

Good info! Quick question if you can help...With the buy to flip loan, would it be negative equity if the loan + interest borrowed was more than the value of a property once renovated and how would someone go about buying a 2nd home to renovate and sell if that were so?

Hiya! Thanks for getting in touch. Yes, you would be in negative equity if your loans and interest amounted to more than the value of the property once renovated. The idea is to buy something cheap that you can add value to via improvements or renovations, which then cause the property value to be more than the loans + interest so you can sell it and make a profit. Hope that helps.

Hi! Technically yes and the bridging loan (buy to flip loan) would then be difficult to convert into a standard mortgage and you wouldn’t be able to pay it off if you sold. A bridging loan is normally very expensive because there are short-term loans. For an example you can expect to pay 0.8% of the total loan each month as interest payments. Also, a normal bridging loan would only last for 12 months, at which time you will have to either pay it off or ask for an extension. I once had a bridging loan which went past 12 months and ended up paying 2% per month as interest. So the idea is, take the bridging loan, paid off as quickly as possible. If you’re unable to pay it off with a sale or by converting it to a standard mortgage then you will be in trouble. However you might be able to convince the buy to let mortgage lender that the property is worth more when you’ve finished the renovation. Therefore you might be able to borrow more as a buy to let mortgage in order to pay off a bridging loan if your bridging loan is higher than the typical sale value. I hope all of that makes sense.

@@tomsoaneofficial yeah that makes sense, thankyou! I was thinking along the lines of if, for example say one buys a wreck house and renovates it up good but the resale price is say the same or slightly less than the full loan with interest, renovation costs and whatever other bills. That would create a none profitable project or even a loss, but could the value of the property be used as equity for a remortgage to repeat that process rather than paying off the bill? In my mind the first house basically acting as a large deposit on a new renovation that would have an initial cost much lower than the final value of the first renovation.

Hi, I recently got a mortgage offer from Halifax, and the exchange of contract is finished, there are a few months to go to get the completion done since this is a new build house. I recently found out there is a huge difference between the Outstanding amount remaining after the Fixed term, for a different mortgage term like 25y or 29y. I would like to ask my Bank to reduce the term before the Mortgage starts, would they be ok with it?

Hi there, thanks for your question! I'm afraid only your bank will be able to answer that question. If you have a mortgage broker, who has sorted your mortgage out with your bank, it's definitely worth getting in touch with them to ask for different terms on your mortgage. Good luck and enjoy your new home!

Banks are not in the business of lending money, they are in the business of securitising debt. They do not lend any money, the borrower borrows the money into existence. The mortgage deed is treated as a species of money and is securitised and sold on.

The worlds leading authority in banking Pro Richard Werner as shown this in his empirical studies of the banking industry.

These facts are not disclosed to the borrower.

Thanks, for the next time: music should not be louder than voice.

Very good video, just bit of feedback, lower the music in the background as it covers your voice too much

Thanks very much! And thanks for your feedback, we'll definitely make a note of that 😊

How to get mortgage job in UK

American here... I've heard in the UK one is not allowed to pay off their mortgage early. True or false?

Hiya! Yes, you absolutely can pay off your mortgage early in the UK. It's always a good idea to check the terms of your individual mortgage offer with your provider in advance though. Hope that helps 😊

Hi how to reduce the value of my property? I have help to Buy and I want to reduce the value of my property. I'm thinking to install solar panels and battery on credit do you think this will help thank you

Do you mean you want to cut down on the cost of your bills? Every situation will be different, but you can start comparing some different energy providers here - www.finder.com/uk/energy

Background music’s super annoying

Hello quick question which wont be quick.

Say I'm buying a house worth 500k

I put down 100k

I work earn 25k a year

Would they give me a mortgage or I dont earn enough?

Let's say I pay £250k deposit I have saved up?

On 25k a year?

Hiya! Thanks for getting in touch. In the UK, you can typically borrow up to 4 times your salary. So on £25K that would be a mortgage of £100K. However, what a mortgage provider will actually lend you will hugely depend on your personal circumstances and financial situation. Which is why I'd suggest chatting to a mortgage advisor, who will be able to give you more specific information on what you would be able to borrow. Hope that helps 😊

interest rates are at over 6% now. I'm so confused after going to my bank for 100,000 mortgage & it said I could potentially pay back 600,00 over 25 years. Why would anyone take out a mortgage if it costs 6x the value of the property. Such a scam.

An interest rate of 6% over 25 years for a 100k mortgage is only 150k in interest meaning you paid 250k for the house not 600k. Additionally the Bank of England puts up interests rates to dissuade you from borrowing money and instead encourages the saving of money, therefore you aren't expected to get mortgages at 6% lol.

Thanks for explaining@@askindale4943

What’s with that music…we r learning….we need silence in background thank you

Music is ridiculous.