I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

Thanks a lot for an explicit coverage of VAR and VECM. I am currently writing my dissertation and your videos on these topics really helped me. I would also like to watch your videos on Nonlinear regression techniques such as quadratic, exponential and cubic. If the videos are not available, kindly upload them.

Thank you so much for your videos on ARCH and GARCH models! It has helped me tremendously!! i am currently doing my dissertation using these models and your explanation is so clear and easily understandable !!! thank you so so so much you are the best!! also your references are extremely helpful, i could never make it without your amazing teaching technique!! keep going dear.

I'm very happy with this news. Keep blazing the trail, Lamgroot and kindly share the link to my TH-cam Channel with your friends and academic community. Please may I know from where (location) you are reaching me?

@@iamgroot3834 Wow! Iamgroot, my African connect! ❤️I'll appreciate it if you can share the link to my TH-cam Channel with your friends and academic community in Mauritius 🇲🇺. They will find the content helpful too 😊. Thanks!

Thanks, Mehinsan for the encouraging feedback... deeply appreciated. The slides are not available to the public. You may jot helpful points as you watch the clips. Thanks.

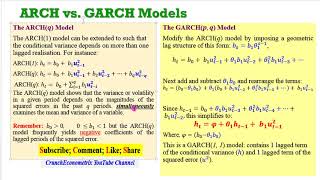

Thanks for all videos on ARCH (i have seen aii of them) and GARCH watched first 3 of them. I think some typo mistske is in the slide started with "GARCH model originat ........" , in the second bullet point the correct sentense is: p represents the lagged term of conditional variance and q is the lagged term of squared reeor term.

Hi Swama, thanks for the positive feedback on my videos. Deeply appreciated! My Channel is a blend of basic, intermediate and advanced-level video tutorials. Kindly look through the Playlists. I'm sure you will find some very useful. Please may I know from where (location) you are reaching me?

Dear Dr. Adeleye, I hope you are doing great. I am leaning ARCH/GARCH models by following your videos. You are really helpful for me. I have a question related to minimum observations on which i can run ARCH and GARCH models. I have limited number of observations and trying capture volatility before and after COVID19. I have no of obs 300 before and 200 after the covid19 crisis. Can i run this model? It would be helpful if you can give reference of material as well.

Adil, thanks for the encouraging feedback. Deeply appreciated! The minimum number of observations required for any statistical analysis is 30. This can be confirmed from econometrics textbooks or online resources. Regards.

I have another question. I am measuring the volatility of 9 stock index before and after covid 19. 3 out of 9 indexes after covid does not shows the Arch effect. What could we drive the interpretation? Does it mean that market with no arch effect are less risky? Please guide me.

@@CrunchEconometrix thank you Dr. Adeleye. What if I applied GARCH model on all 9 indices and i found 3 results in which the sum of ARCH and GARCH coefficient is more than 1. what does it mean? Your valuable would be highly appreciated.

Good evening Dr. Please how can we explain the causes of currency fluctuations based on the stationarity test analysis. Or is there any other tools to depicts the causes of exchange rate fluctuations. Thanks

@@CrunchEconometrix The news impact function is typicallydefined as the expectation of tomorrow's volatility conditional on today's return with today's volatility fixed at unconditional volatility. ... The monotonic news impact curve, instead of the U-shaped curve, for SV models is due to the different specification of volatility process.This is what i found from Google. I'm from India.

Congrats on your brilliant series. However, one specific point you made in minute 1.40 approx of this video, regarding what p and q stand for, do not coincide with the written explanatory statement, atop equation (2);. In it,, p stands as the order of the squared error term and q is the order of the lagged variable h, contrary to your audio explanation. Thanks and best.

Hello Ngozi Adeleye ..brilliant econometrician, what if all the value of max stastics are less than 5% critical values in johansen co integration test .,but trace statistics result are okay.. what shall I decide ?

Excellent video Professor. It's really helpful. I watched your GARCH videos and I'm concerned if I can compare the unconditional variance of the GARCH with a variance. I mean I have 2 series: 1 with ARCH effect and the other without. Can I compare the extracted unconditional variance of the GARCH (serie with the ARCH effect) with the variance (serie without ARCH effect)?

@@CrunchEconometrix exactly. If the serie doesn't has an arch effect, you shouldn't use the GARCH. I have 2 series: 1 with arch effect and 1 without arch effect. I did a GARCH for the series with arch and I didn't use the GARCH for the other series because it hasn't an arch effect. So the question is: if I extract the unconditional variance (long-run average variance) of the GARCH, can I compare it to the variance of the series without arch effect? Are these estimates comparable?

Hi madam I hope you will be doing well, MADAM I read your paper titled " Comparative investigation of the growth -poverty - inequality in sub saharan and caribbean countries' ' . Could you please guide how we can calculate Gini Index growth rate (%).

in the first video you were saying p denotes lagged terms variance and q denotes lagged terms of square error. but in this video you are saying exactly opposite.

Madem I saw others peoples use arima in garch model. I would juste like to know between using arch in garch model and using arima in garch model, which is better? I understood everything you explained in the videos, but it's just for my knowledge.

Ok Patrick. I will only say that those studies will have justifications for using those techniques. You may need to find similar studies to yours and use what they used.

HI… i hope you will be okay .. i have a question…. whih is not related to this vedio... My data is time serious and i test johensan co-integration test there is 3 co-integrating variables out of 4 … now can i use FMOLS test ….to find out the long run relationship or not …. thank you

hello there i am working on bilateral remittance and its cost. I have home country and host country. kindly if you can make it easy for me, how to work in STATA for bilateral panel data? tnx

Hi Cyril, please know that dofiles are no longer free but available on my website upon payment of a token after which you are allowed a one-time download. Here's the link cruncheconometrix.com.ng/shop

CrunchEconometrix hello ma. After performing the ardl bounds test to determine wether short or long run. Is it the same command we use to perform both the long run and the short run? Or are they different command

Dear Mam Want to send one manuscript related to Time Series Econometrics with special reference to ARCH/GARCH to your mail id for your valuable comments. Your comments or suggestions will enrich my writings. Kindly allow me to send. Looking for your kind angle of ratification

Hi Sir, please bear with me. Due to time constraints and my busy schedule, I restrict my terms of engagement to comments pertaining to my TH-cam videos. Kindly post your queries and I will do my best to guide you. Thanks for your understanding.

Dear Dr. Bosede Ngozi ADELEYE Just have a look on the manuscripts written by me by taking lots of help from your videos. I don’t want to waste your valuable time , just have a look for few minutes and suggest me whether I can proceed for publication. Please mam allow me to send. Regards, Kanchan Datta

Please can you make videos for covid19 forecasting using ARIMA model On urgdt basis Will be thankful Can you send me your email As i need to send you email Regards

I want to appreciate all my subscribers from across the globe (Africa, Asia, Europe, the Middle East, The Americas, and The Pacific). Thank you all for your support. I am encouraged by your comments, questions, likes and critiques. They keep me focussed and poised to do better. I will continue to contribute my little quota such that every student and researcher will independently analyse his/her data. My teaching approach is very practical. I adopt a do-as-I-do style. Many thanks to those who have supported me by telling others. Once again, CrunchEconometrix loves to teach, support my Channel with your subscription, likes, feedbacks and sharing my videos with your cohorts. Please do not keep me to yourself (lol) inform your friends, students and academic networks about my Channel. Tell them CrunchEconometrix breaks down the econometric jargons and teaches with simplicity. Follow me on Facebook, Twitter and Reddit. Love you all, greatly!!!

in 2024, this is really amazing, thank you so much for rescuing my semester🤣

U're welcome.

Thanks for all these good video

Thanks for the encouraging feedback, Cyril. Deeply appreciated! Please may I know from where (location) you are reaching me?

Please ma. The command for the Gregory Hansen test is not working on stata 16. How do I fix that thanks

I am writing you from the University of East Anglia, Norwich UK

CrunchEconometrix university of East Anglia Norwich, UK

Cyril, so many codes are not working on Stata16. They are yet to get it right. So, always use earlier versions with v16.

Thanks a lot for an explicit coverage of VAR and VECM. I am currently writing my dissertation and your videos on these topics really helped me. I would also like to watch your videos on Nonlinear regression techniques such as quadratic, exponential and cubic. If the videos are not available, kindly upload them.

Great to hear, Emmanuel...thanks! I have also noted the suggested topics.

Thank you so much for your videos on ARCH and GARCH models! It has helped me tremendously!! i am currently doing my dissertation using these models and your explanation is so clear and easily understandable !!! thank you so so so much you are the best!! also your references are extremely helpful, i could never make it without your amazing teaching technique!! keep going dear.

I'm very happy with this news. Keep blazing the trail, Lamgroot and kindly share the link to my TH-cam Channel with your friends and academic community. Please may I know from where (location) you are reaching me?

@@CrunchEconometrix I am from Mauritius, a small island in the indian ocean.

@@iamgroot3834 Wow! Iamgroot, my African connect! ❤️I'll appreciate it if you can share the link to my TH-cam Channel with your friends and academic community in Mauritius 🇲🇺. They will find the content helpful too 😊. Thanks!

Dear Dr Adeleye, this is really nice. May God bless you for this. Also, would it be possible to get your slides?

Thanks, Mehinsan for the encouraging feedback... deeply appreciated. The slides are not available to the public. You may jot helpful points as you watch the clips. Thanks.

Thank you all videos helped me alot :)

Good to hear, Vinay. Thanks for the encouraging feedback, deeply appreciated! Please may I know from where (location) you are reaching me?

Thanks for all videos on ARCH (i have seen aii of them) and GARCH watched first 3 of them. I think some typo mistske is in the slide started with "GARCH model originat ........" , in the second bullet point the correct sentense is: p represents the lagged term of conditional variance and q is the lagged term of squared reeor term.

Thanks Dr. Ghauri for pointing out the typos. Appreciated!

Ma'am all the vedeos are excellent....is there any video on basics of econometrics done by u?

Hi Swama, thanks for the positive feedback on my videos. Deeply appreciated! My Channel is a blend of basic, intermediate and advanced-level video tutorials. Kindly look through the Playlists. I'm sure you will find some very useful. Please may I know from where (location) you are reaching me?

Dear Dr. Adeleye, I hope you are doing great. I am leaning ARCH/GARCH models by following your videos. You are really helpful for me. I have a question related to minimum observations on which i can run ARCH and GARCH models. I have limited number of observations and trying capture volatility before and after COVID19. I have no of obs 300 before and 200 after the covid19 crisis. Can i run this model? It would be helpful if you can give reference of material as well.

Adil, thanks for the encouraging feedback. Deeply appreciated! The minimum number of observations required for any statistical analysis is 30. This can be confirmed from econometrics textbooks or online resources. Regards.

@@CrunchEconometrix Thank you

I have another question. I am measuring the volatility of 9 stock index before and after covid 19. 3 out of 9 indexes after covid does not shows the Arch effect. What could we drive the interpretation? Does it mean that market with no arch effect are less risky? Please guide me.

Correct. That's the most plausible explanation, Adil.

@@CrunchEconometrix thank you Dr. Adeleye.

What if I applied GARCH model on all 9 indices and i found 3 results in which the sum of ARCH and GARCH coefficient is more than 1. what does it mean? Your valuable would be highly appreciated.

Good evening Dr.

Please how can we explain the causes of currency fluctuations based on the stationarity test analysis. Or is there any other tools to depicts the causes of exchange rate fluctuations.

Thanks

Udo, use the historical events of the economy you're investigating to discuss the variable.

@@CrunchEconometrix thanks Dr. Really grateful

Ma'am can you please do a video on how to build a news impact curve in Eviews.

Hi Ann, I'm not sure what that is. Can you be more specific and may I know from where (location) you are reaching me?

@@CrunchEconometrix The news impact function is typicallydefined as the expectation of tomorrow's volatility conditional on today's return with today's volatility fixed at unconditional volatility. ... The monotonic news impact curve, instead of the U-shaped curve, for SV models is due to the different specification of volatility process.This is what i found from Google. I'm from India.

No, idea about this technique. Much love to your friends and academic community in India. Tell them about my TH-cam Channel :)

Congrats on your brilliant series. However, one specific point you made in minute 1.40 approx of this video, regarding what p and q stand for, do not coincide with the written explanatory statement, atop equation (2);. In it,, p stands as the order of the squared error term and q is the order of the lagged variable h, contrary to your audio explanation. Thanks and best.

Hi Douglas, that is an mix-up. But I'm sure you do understand what p, q stands for as my explanations are quite clear. Thanks for the observation.

Just add a small correction in the slide. No big deal. Again kudos for your fantastic work.

Thanks... Not sure that will be happening. I gave clear explanations... And the model can be easily followed.

Hello Ngozi Adeleye ..brilliant econometrician, what if all the value of max stastics are less than 5% critical values in johansen co integration test .,but trace statistics result are okay.. what shall I decide ?

Henok, you are posting this query on the WRONG thread. Kindly re-post appropriately. Thanks.

Excellent video Professor. It's really helpful.

I watched your GARCH videos and I'm concerned if I can compare the unconditional variance of the GARCH with a variance. I mean I have 2 series: 1 with ARCH effect and the other without. Can I compare the extracted unconditional variance of the GARCH (serie with the ARCH effect) with the variance (serie without ARCH effect)?

Hi Eduardo, you did not watch my ARCH videos as advised for you to know that once there is no "arch" effect, then no basis for ARCH/GARCH modeling.

@@CrunchEconometrix exactly. If the serie doesn't has an arch effect, you shouldn't use the GARCH.

I have 2 series: 1 with arch effect and 1 without arch effect. I did a GARCH for the series with arch and I didn't use the GARCH for the other series because it hasn't an arch effect. So the question is: if I extract the unconditional variance (long-run average variance) of the GARCH, can I compare it to the variance of the series without arch effect? Are these estimates comparable?

In my opinion, there is no basis for comparing a model with an ARCH effect and another without.

Hi madam

I hope you will be doing well, MADAM I read your paper titled " Comparative investigation of the growth -poverty - inequality in sub saharan and caribbean countries' ' .

Could you please guide how we can calculate Gini Index growth rate (%).

Hi Majid, first generate the natural logarithm of Gini Index (lngini), then generate the difference of lngini to get the growth rate of Gini Index.

Dear Madam can we use garch to model panel data as in for many countries and many independent variables

Hi Saa, to the best of knowledge, the answer is NO.

in the first video you were saying p denotes lagged terms variance and q denotes lagged terms of square error. but in this video you are saying exactly opposite.

Check the model. I tailor my explanations to the model...and that shouldn't be a problem once you know what your p and q represent.

Madam we can use AR model in garch model? Thank!

Kindly watch my ARCH and GARCH videos. Support them with readings (see references at the end of the video) for better understanding. Thanks.

Madem I saw others peoples use arima in garch model. I would juste like to know between using arch in garch model and using arima in garch model, which is better? I understood everything you explained in the videos, but it's just for my knowledge.

Ok Patrick. I will only say that those studies will have justifications for using those techniques. You may need to find similar studies to yours and use what they used.

@@CrunchEconometrix Thank you madam!

HI… i hope you will be okay ..

i have a question….

whih is not related to this vedio...

My data is time serious and i test johensan co-integration test there is 3 co-integrating variables out of 4 …

now can i use FMOLS test ….to find out the long run relationship or not ….

thank you

Yes, you can use FMOLS to establish long-run relationships.

hello there i am working on bilateral remittance and its cost. I have home country and host country. kindly if you can make it easy for me, how to work in STATA for bilateral panel data? tnx

Categorise the countries and analyse your model in line with your study objectives.

Abbreviation ( A GARCH ) ?

Hi Khalid, your query is unclear.

Please ma can I get the do file for the ardl modelling

Hi Cyril, please know that dofiles are no longer free but available on my website upon payment of a token after which you are allowed a one-time download. Here's the link cruncheconometrix.com.ng/shop

CrunchEconometrix hello ma. After performing the ardl bounds test to determine wether short or long run. Is it the same command we use to perform both the long run and the short run? Or are they different command

Dear Mam

Want to send one manuscript related to Time Series Econometrics with special reference to ARCH/GARCH to your mail id for your valuable comments. Your comments or suggestions will enrich my writings. Kindly allow me to send. Looking for your kind angle of ratification

Hi Sir, please bear with me. Due to time constraints and my busy schedule, I restrict my terms of engagement to comments pertaining to my TH-cam videos. Kindly post your queries and I will do my best to guide you. Thanks for your understanding.

Dear Dr. Bosede Ngozi ADELEYE

Just have a look on the manuscripts written by me by taking lots of help from your videos. I don’t want to waste your valuable time , just have a look for few minutes and suggest me whether I can proceed for publication. Please mam allow me to send.

Regards,

Kanchan Datta

Please can you make videos for covid19 forecasting using ARIMA model

On urgdt basis

Will be thankful

Can you send me your email

As i need to send you email

Regards

Hi Ali, I have no idea how to do that at the moment. You may need to check other online resources. Thanks.