Thx a lot! I'm struggling for mathematical finance and your video about martingale and sigma field saves my life! They are super abstract!!!!Thx again!!!

Much more intuitive now, I had only seen formulas and was applying them without really knowing the bigger picture. Thanks and by the way you've got a nice voice to listen to.

axioms are a minimum number of assumptions that you must take to be true ('self-evident'), in order to build a set of coherent and useful proofs - the theory. They are not always intuitive

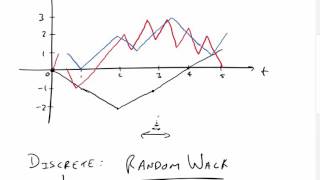

When you say that the brownian motion follows a normal distribution, does that mean that at any point in time, the increment provided by the brownian motion can take any value from -inf to + inf and that the probability of each of the possible increments is given by the normal distribution density function (as opposed to, for example, a random walk in which the increment is either 1 or -1 and we usually give it a uniform distribution - as far as I know)? My question probably has some technical mistakes but I am not a mathematician/statistician or even close. I'm just trying to get some intuition behind all of these concepts and their applicability to the modeling of financial markets.

I have a question about the Ito's integral. You say that the Ito Integral in the integral of a random variable with respect to Brownian motion correct? But what exactly is that? For example, if you integrate a velocity function what the answer IS is the total distance traveled. Or more generally multiple the y-axis by the x-axis and it is the total of what ever that product is. So what exactly IS the answer you get from performing Ito's Integration?

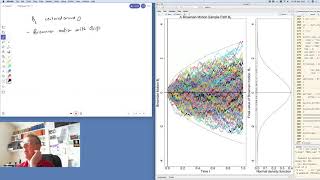

Einstein developed a theory of Brownian motion (it originates in physics) where he showed that the density of particles undergoing Brownian motion satisfies an effective diffusion equation, the solutions of which have the form of a normal distribution, so essentially yes this is proven

![[안방1열 풀캠4K] 베이비몬스터 'DRIP' (BABYMONSTER FullCam)│@SBS Inkigayo 241110](http://i.ytimg.com/vi/AQ4RIghEvUs/mqdefault.jpg)

Couldn't comment in your stochastic calc video but it felt really well explained!!!!! This channel is a hidden gem

Thank you for sharing your understanding. Your explanation is rigorous yet very intuitive. Your contribution is important in educating more people

To learn this difficult subject. (I hit the wrong button before I finished my comment.)

Thx a lot! I'm struggling for mathematical finance and your video about martingale and sigma field saves my life! They are super abstract!!!!Thx again!!!

Much more intuitive now, I had only seen formulas and was applying them without really knowing the bigger picture. Thanks and by the way you've got a nice voice to listen to.

axioms are a minimum number of assumptions that you must take to be true ('self-evident'), in order to build a set of coherent and useful proofs - the theory. They are not always intuitive

saving my life i love you

When you say that the brownian motion follows a normal distribution, does that mean that at any point in time, the increment provided by the brownian motion can take any value from -inf to + inf and that the probability of each of the possible increments is given by the normal distribution density function (as opposed to, for example, a random walk in which the increment is either 1 or -1 and we usually give it a uniform distribution - as far as I know)?

My question probably has some technical mistakes but I am not a mathematician/statistician or even close. I'm just trying to get some intuition behind all of these concepts and their applicability to the modeling of financial markets.

bro u just unlocked me

68.3% at 1 sd away from 0, 95.4% at 2 sd's from 0, and 99.7% at 3 sd's away from 0, approximately

95.5%

@@erickjian7025 95.44997% as a computation, the standard normal table is slightly off

Can't we prove the continuity of BM sample paths with the law of the iterated logarithm for instance ?

Awesome, really useful

I have a question about the Ito's integral. You say that the Ito Integral in the integral of a random variable with respect to Brownian motion correct? But what exactly is that? For example, if you integrate a velocity function what the answer IS is the total distance traveled. Or more generally multiple the y-axis by the x-axis and it is the total of what ever that product is. So what exactly IS the answer you get from performing Ito's Integration?

Great video.Can u make a video of how hursts exponent value of not equal to 0.5 is not a Brownian motion.I want to understand the math behind it.

That 3rd axiom can't be proven? I feel like there is a proof that the distribution is normal but I may be mistaken.

Einstein developed a theory of Brownian motion (it originates in physics) where he showed that the density of particles undergoing Brownian motion satisfies an effective diffusion equation, the solutions of which have the form of a normal distribution, so essentially yes this is proven

TH-cam professors...🙂

lol wiener motion 🌭

🤣🤣🤣