Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. Actually I am in that group. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Very useful thanks! Are there problems in implementing this model when we have one cross-section only over 10 years? Is it still recommended to use this model under this circumstance?

Aoa sir please guide my dependant variable is level stationary and remaining 2 independent are First difference stationary May i apply Kao pedronia and fisher

Dear Sayed, I am currently running a panel cointegration test with the model gdp=gfcf+labor+nec+c+trend, where gfcf is real gross fixed capital formation per capita, labor=labor force participation rate, nec=nuclear energy consumption per capita. I followed the step in your video, however, the results shows no cointegration. Do you have any advice on this?

Hi Hua, may I ask what did you determine as your next step, as I am currently writing a dissertation on a similar topic including renewable energy consumption and non renewable in replacement of your nuclear energy consumption variable.

Dear Mr. Hossain, I thank you very much as this has opened me the door to understand better about how to proceed in my Phd studies. There is one thing I would like to ask you is that my control panel on eViews 8 does not offer the three methods (Pedroni, Kao, ..) you selected. Also the results come not the way your results display. They come in very different ways. Which eViews do you use in this presentation? Thank you and God bless you.

Dear Sayed, Thanks a lot for the wonderful work that you are doing. What would be you advice if I wish to run a panel vecm, of which the time period is just 12 years and 52 cross-sections? Best regards, Clement

Sir, I have not yet done panel VECM yet so unable to comment. However, I would like to invite you to join our Hossain Academy data analysis discussion below. facebook.com/groups/hossainacademy/

Thaaaank you for your big effort.. it helps me a lot Dr. .. can you answer me please sir .. why I can't find the option ''Pedroni", there is only KAO and Fisher that's all in the panel?

Thank you, sir, If we tested for cointegration by Pedroni method and we found that the panel data are cointegrated in one test ( individual intercept and individual trend ) from three tests; as well as it is cointegrated in the KAO test(second method). is it considered as cointegrated or not?

Thank you for your most valuable videos which are playing major role to carry out my research works. I got one doubt sir, that is, one of your variable Export is doesn't have unit root problem at the level itself. According to the theory (you stated) the variables should be integrated at order one I(1) to run the cointegration. But you ran the cointegration test including export (which is integrated at order zero I(0). Can we run like this? Please clear my doubt sir.

I said I assume that variables have unit root at level. In this case I did not test the way you did. But guideline is variables must be I(1) to run cointegration..

Hello sir, i want to ask whether or not should i do panel cointegration for variables that are already stationary without doing first differencing? should i do for first difference variables only or do for all of the variables? thank you in advance.

Hello sir.. i've a issue... when i run cointegration eviews shows "insufficient numbers of observations" error and when i run ARDL test the eviews show "near singular matrix" error... While on my superviosr's eviews it doesnot show any error and data is same.....what should i do?

Thank you Awam, I would like to invite you to join Hossain Academy Facebook at below link and post your question there if you have any. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Thank you for your nice video. Hope that you will do it in STATA. BTW, your personal website is not working for last few days. Is there any way to get the data set.

Sayed Hossain Your website www.sayedhossain.com is not opening in my browser. Is there anything in my side or the your site has problem? How do I get the data for this video? And I am usually a STATA user. So I hope that you will do the same test in STATA and all your upcoming like PANEL FMOLS, Panel Dynamic OLS model etc.

Yes I have plan to make it into STATA and R software also. Wait few days more. I do not know why you can not open Hossain Academy website as it is working here. You type Hossain Academy in Google and find it there.

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy.

How can We do that on Stata Mr. Hossain? I need to do a co-integration test using either pedroni or fisher and I have no idea how to do it. Please help!

Dear Adrian, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Dear Taha, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. Actually I am in that group and may help you. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy

+Nesrine BENDIMA Thank you for your question but I would like to invite you to join Hossain Academy Facebook for greater interaction about economics, finance and econometrics with me. Thank you Sayed Hossain from Hossain Academy. Please join below and post your question.facebook.com/groups/hossainacademy/

If we tested for cointegration and we found that the panel data is cointegrated, how do we change the model/regression? can you make a video about this? :)

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

![ปฏิเสธไม่ไหว (Crush on you) - LIPTA feat. No One Else [Official MV]](http://i.ytimg.com/vi/NBw1jF342vw/mqdefault.jpg)

Sir your video tutorials are priceless.they have helped me immensely in my projects during masters.thank you for all the help.god bless u.

You are welcome

@@sayedhossain23 They helped me too. your way of explanation is very easy and makes those who are not good in statistics to understand everything

Hello from TURKEY, thanks for your effort.

Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your

question there. Actually I am in that group. Thank you once again, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

Thank you, I already enjoyed the group few minutes ago

Thank you sir. Your videos are VERY appreciated.

thanks for your supporting, im so glad of your work, please keep going on, you got a new subscriber

Thanks for the sub!

Very useful thanks! Are there problems in implementing this model when we have one cross-section only over 10 years? Is it still recommended to use this model under this circumstance?

Sir, do I need to log the data before conduct the test?

Thanks for your video, it really helped me a lot!!!

Aoa sir please guide my dependant variable is level stationary and remaining 2 independent are First difference stationary

May i apply Kao pedronia and fisher

Dear Sayed, I am currently running a panel cointegration test with the model gdp=gfcf+labor+nec+c+trend, where gfcf is real gross fixed capital formation per capita, labor=labor force participation rate, nec=nuclear energy consumption per capita. I followed the step in your video, however, the results shows no cointegration. Do you have any advice on this?

Hi Hua, may I ask what did you determine as your next step, as I am currently writing a dissertation on a similar topic including renewable energy consumption and non renewable in replacement of your nuclear energy consumption variable.

Dear Mr. Hossain, I thank you very much as this has opened me the door to understand better about how to proceed in my Phd studies. There is one thing I would like to ask you is that my control panel on eViews 8 does not offer the three methods (Pedroni, Kao, ..) you selected. Also the results come not the way your results display. They come in very different ways. Which eViews do you use in this presentation? Thank you and God bless you.

Dear Sayed,

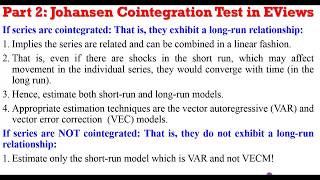

Thanks a lot for the wonderful work that you are doing. What would be you advice if I wish to run a panel vecm, of which the time period is just 12 years and 52 cross-sections?

Best regards,

Clement

Sir, I have not yet done panel VECM yet so unable to comment. However, I would like to invite you to join our Hossain Academy data analysis discussion below.

facebook.com/groups/hossainacademy/

Hi, I am working on panel data, can u helping me who to apply and interpret the results of johanson cointegration

Thaaaank you for your big effort.. it helps me a lot Dr. .. can you answer me please sir .. why I can't find the option ''Pedroni", there is only KAO and Fisher that's all in the panel?

Thank you, sir, If we tested for cointegration by Pedroni method and we found that the panel data are cointegrated in one test ( individual intercept and individual trend ) from three tests; as well as it is cointegrated in the KAO test(second method). is it considered as cointegrated or not?

Sir can you plz tell me,which eviews version you have used in this video?

Nice Video

do we need to create difference series for I(1) variable to run pedroni?

Thank you for your most valuable videos which are playing major role to carry out my research works. I got one doubt sir, that is, one of your variable Export is doesn't have unit root problem at the level itself. According to the theory (you stated) the variables should be integrated at order one I(1) to run the cointegration. But you ran the cointegration test including export (which is integrated at order zero I(0). Can we run like this? Please clear my doubt sir.

I said I assume that variables have unit root at level. In this case I did not test the way you did. But guideline is variables must be I(1) to run cointegration..

Sayed Hossain Thank you for your kind reply Sir....Now, I got clear idea. Thank you once again.

Sir how do you know from this video that Export is doesn't have unit root problem at the level itself?

Thank you very much

Hello sir, i want to ask whether or not should i do panel cointegration for variables that are already stationary without doing first differencing? should i do for first difference variables only or do for all of the variables? thank you in advance.

Hello sir.. i've a issue... when i run cointegration eviews shows "insufficient numbers of observations" error and when i run ARDL test the eviews show "near singular matrix" error... While on my superviosr's eviews it doesnot show any error and data is same.....what should i do?

Thank you Awam, I would like to invite you to join Hossain Academy Facebook at below link and post your question there if you have any. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Thanks Sayed

Prosper Chitambara You are welcome to Hossain Academy. thank you sayed Hossain from Hossain Academy at www.sayedhossain.com

Hello from Algerien, thanks for your lessons ....If possible Panel Cointegrating Model. One. stata.....please.

LEBEN OUTCOME

Hurlin panel casuality test, How is make in the eviews ?

+Erkan Alsu Not yet done.

Thank you for your nice video. Hope that you will do it in STATA. BTW, your personal website is not working for last few days. Is there any way to get the data set.

In EVIEWS page, Data is in EVIEW form and in STATA, data is in STATA form. Can u tell me exactly where it is not working. Thanks

Sayed Hossain Your website www.sayedhossain.com is not opening in my browser. Is there anything in my side or the your site has problem?

How do I get the data for this video? And I am usually a STATA user. So I hope that you will do the same test in STATA and all your upcoming like PANEL FMOLS, Panel Dynamic OLS model etc.

Yes I have plan to make it into STATA and R software also. Wait few days more. I do not know why you can not open Hossain Academy website as it is working here. You type Hossain Academy in Google and find it there.

If we have a combination of I(0) and I(1) variables in our panel data which panel co-integration test can be run? Thank you.

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy.

Hi Fulya, in this case ARDL is better option if N

How can We do that on Stata Mr. Hossain? I need to do a co-integration test using either pedroni or fisher and I have no idea how to do it. Please help!

+Adrian Liapis

Hossain Academy EVIEWS section has the video on panel cointegration test using Pedroni.

Dear Adrian, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

Hello, If the data was not stationary at the first difference but it was at the second than we could run the model.

Thanks

Dear Taha, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. Actually I am in that group and may help you. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy

if i have 5 varibales stationary at level and 2 statinory at 1 st difference i go for cointegration ?? thank you

+Nesrine BENDIMA

Thank you for your question but I would like to invite you to join Hossain Academy Facebook for greater interaction about economics, finance and econometrics with me. Thank you Sayed Hossain from Hossain Academy. Please join below and post your question.facebook.com/groups/hossainacademy/

how to run Granger panel causality test with VECM ? ty very much

+Chi Duong Thien Wald test you can apply

+Sayed Hossain ty bro

Can eview run autocorrelation test for panel data ?

If we tested for cointegration and we found that the panel data is cointegrated, how do we change the model/regression? can you make a video about this? :)

If the panel variables are cointegrated, then you can run Panel dynamic OLS model, that is panel dols model. I have not done it yet but will do soon.

Data are not available on the website.

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/