Really Sir, you are the real hero of this digitalized century. For this expensive software running scheme, your tutorial is the best guide for the students of LDCs for whom buying a computer is also a herculian task.................................................................I'm learning eviews from your site and in the future if I will be settled in my career then, undoubtedly, I will meet you to honour your such type of miraculous social awareness and human captical campaign basically in this (educational) field. Hats up to you Sir, you are actually making a revolution in your field....

Dear Paudel, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

I do not have Microfit software to run ARDL Model. Logit, Probit and Two Stage least Square model I have plan in future to make video. Thank you for visiting Hossain Academy

Dear collegues I am currently stuck on testing PPP for long run effect between France and Germany during post-Bretton Woods period (April 1973-December 1990). I need to check for cointegration (Johansen test) among Fr/Ger exchange rate, Fr CPI and Ger CPI. Taking logarithms, basically, the equation looks like ln(Ger/Fr)=ln(Ger CPI)-ln(Fr CPI). Preliminary, we should test for unit root, and there is the most interesting thing: utilizing ADF(with constant and trend) and Perron's Procedure I got Ger/Fr = I(1), CPIs are both I(2). The question is how can I perform cointegration test if ranks of integration are different? Is it eligible to take the difference concerning CPIs to derive I(1) process and proceed with Johansen test? Regards

why do you use the correlogram and not an ADF or PP in unit root test function in Eviews to test for non-stationarity. The reason i ask is because after lag four in difference on correlogram i can still reject the null hypothesis.

All methods are equally good. But so many lags is not preferred. I would take the decision of SC suggesting one lag....You use the same number of lags for all models such as Johansen, VAR, VECM etc after lag selection....

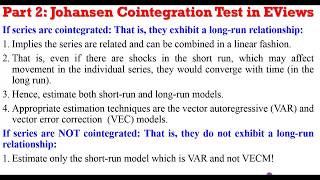

Hi Sir, allow me ask you a quite trivial question. Econometric theory states two series integrated of order zero and order one i.e. I(0) and I(1) can't be Cointegrated. Is it necessary to go ahead and run the Johansen test of Cointegration? My second query is about the lag selection criteria. Normally, after carrying out the various criteria like AIC, LR, SC, HQ and FPE, some people subtract 1 from the answer they get. E.g if the criteria say the optimal lag is say 4, then they subtract one so that the lag to be used in Cointrgration test is 3. The idea is that series to be tested for Cointegration are always in first difference so we need to subtract one from the optimal lag indicated by the lag selection criteria! What is your opinion on this Sir? And what should be my next step now that one of my two series is I(0) while the other is I(1)? Thanks' Kigosa Nathan.

In first case you can not run Johansen test as both variables are not I(1). I have not heard about the lag selection criteria that you have mentioned but it sounds new to me. I shall think about it.

hi sir, start from 2.17 , when we open the estimate VAR , all variables is key in at the Endogenous Variable column only (like what u do)? or i need to key in my independent variables at Exogenous Variables column ?

Hi sir, I ran the VEC model but now my question is where does granger come into effect now. Should run the granger causality test soon as well after VECM or I should consider the causality based on VECM.

Hi,I would like to know that are our variables must have one unit root? In that way, all variables are none-stationary at level and stationary at 1st difference?

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy.

hi Prof Hossain, i'm very appreciate for your tutorials...it's really helpful..can i know in 18:29 minutes, you choose the option 3 (intercept no trend model) why we choose option 3 but not option 1 or 4? correct me if i'm wrong..because i din't learn about Lag selection yet..Thank you =)

Hi Sir, I'm again back with two burning issues; 1. If two series are I(0) and I(1), do I use the level data when running the test for optimal lag or I have to use the first difference data of the non-stationary variable? 2. If one of the variables has to be transformed to first difference, is that automatically done in VECM, VAR, and when running the test for optimal length or I have to manually /physically do it?

In case of lag selection, you use the data that you have directly whether it is I(0) or I(1). In case of VECM, data automatically convert to first difference but in case of VAR, you need to convert data to first difference manually..

I used this method to pick the optimal lag, but the best results from AIC and SC are quite different. AIC suggest 7 lag SC suggest 1. which one should i pick? Im running a johansen model with daily observations so I included 30 lags to test. When I narrow the lag down to 8, both criteria results jump to 1 lag. SO is there something wrong the model? or the lag i picked? how to pick the appropriate lag to run the var model?

Depends on frequency of your data. If it's quarterly/monthly/daily then yes that is enough. However, if annual you may want to add more years because you only have 25 observations.

night Sir , i'am rizky , I was a college student would like to ask how the selection and use of the value of lambda max and lambda trace the Johansen cointegration test , if both of the numbers of cointegration vectors formed is different. eg in lambda trace cointegration vectors are 3 and lambda max cointegration are 2 , then I have to choose which one?

Dear Rizky, Thank you. I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

If we find that even the 1st difference also cannot accept the null hypothesis so we cannot use the data to run cointegration ? What if we need to test for the long-run relationship. Do you have other options to test for long-run relationship ? Thank you.

Dear Fah, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Hello prof hossain.. i saw your tutorials vidéos in youtube , i am so happy for that.. because i need like those vidéos i want to thank you so much. . And i have a question i hope that i find her answer.. plz when we study a stationary of two time séries and we found one stationry at level and other stationary at first différence. . What do we do? I need your solution. . We can't apply cointegration méthode are there any solution Thank you

Dear Nina, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Dear Sir.. i really impressed with your lectures and your knowledge. here i have some issues that if we have a model having 4 variables in which our 2 variables are stationary at level and 2 are stationary at 1st difference. then what method should we choose?

+Zeeshan Shah Thank you. I would like to invite you to join Hossain Academy Facebook for greater interaction about economics, finance and econometrics with me. Thank you Sayed Hossain from Hossain Academy. Please join below and post your question.facebook.com/groups/hossainacademy/

Thank you. I would like to invite you to join Hossain Academy Facebook Group (Data Analysis) at below link and join our group discussion about modelling. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Hi sir, Thank you so much for your lectures they are so clear and helpful to many of us on distance learning programs. I ran the VEC model but now my question is where does granger causality come into effect. Should i run the granger causality test separately soon after VECM or I should consider the causality based on VECM. Thank you in advance

Dear Weston, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Dear Amina, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Hello. Thank you very much for the tutorial. My question is: I'm working with 5 variables (all are non-stationary at level and stationary at first difference). When I run the cointegration test, only 3 are cointegrated. Can I still do VECM with all of them? Thank you

Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/ REPLY

hai sir, if my data is already stationary at level, meaning i cant proceed with Johansen test right? So, what other test can I conduct in order to observe the cointegration?

Dear Nurul, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Hi Sir, I did the unit root test using Phillip Perron and ADF and both my series were I(1) but now when i follow this video to run the VECM, when i did the correlogram, the other variable does not show stationarity at all (at level and at both 1st and 2nd difference). So can you help here so that i can run my VECM?

That is always a common problem. Results will vary from testing method to testing method. You better take one method as your benchmark to decide result.

Sayed Hossain Hello Sir, Sir i need to ask this, when carrying out a Johansen Cointegration Test and assuming there is no deterministic trend in the data ( because it is the only that gives me results that there is cointegration) say option 1, does this mean i have to use the same option when estimating VAR? And will the results still be desirable?

Hello Sir, the video was really helpful. However, when I run the co-integration test the none, at most 1, at most 2 are rejected. Only in at most 3 I can accept the null hypothesis. What should I do and what does this mean?

Hello, The problem I have is that I have only 25 data points for 7 time series. I only have annual data when quarterly would be better. With this data EViews is telling me I am unable to check lag criteria beyond lag=3 due to insufficient data. However, I find this problematic because from the standpoint of theory a higher lag order would be better. Can you assist me?

hi sir, i m working on the VECM for the yield in government debt market for which i have identified 10 dependent variables like reporate, inflation, moneysupply etc. but the problem here comes is some of my variables are stationary at 1st difference and some at level . does this mean that these variables are not in same order. i ran lag selection criteria process and it shows around 27(which i guess is too high and not approved by my teacher). how to make them in same order n complete my project.please help

I guess I said that if the error correction term is negative and significant meaning that there is a long run causality running from independent variable to dependent variable. You can see my error correction model in this regard

Dear Taha, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

hi sir, your videos are very helpful for me, but i have one question which i always cannot understand. can you tell us, how to make TSP or DSP in ADF Test? if one variable of 4 is trend stationary, how can I do in the next step? thanks a lot!

i mean if there are 4 variables, one is trend stationary, and the other three are I(1), how can I do with the 4 variables in the next step, for example can i do johansen test and vecm with the 4 variables?

Really Sir, you are the real hero of this digitalized century. For this expensive software running scheme, your tutorial is the best guide for the students of LDCs for whom buying a computer is also a herculian task.................................................................I'm learning eviews from your site and in the future if I will be settled in my career then, undoubtedly, I will meet you to honour your such type of miraculous social awareness and human captical campaign basically in this (educational) field. Hats up to you Sir, you are actually making a revolution in your field....

Dear Paudel, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Good on ya Sayed. Incredibly helpful, cheers!

I do not have Microfit software to run ARDL Model. Logit, Probit and Two Stage least Square model I have plan in future to make video. Thank you for visiting Hossain Academy

thank you Sir this was a helpfull video

Dear Sir, my variables become stationary in the second difference and not at first difference, can i proceed with the johansen test of co integration?

Dear collegues

I am currently stuck on testing PPP for long run effect between France and Germany during post-Bretton Woods period (April 1973-December 1990). I need to check for cointegration (Johansen test) among Fr/Ger exchange rate, Fr CPI and Ger CPI. Taking logarithms, basically, the equation looks like ln(Ger/Fr)=ln(Ger CPI)-ln(Fr CPI). Preliminary, we should test for unit root, and there is the most interesting thing: utilizing ADF(with constant and trend) and Perron's Procedure I got Ger/Fr = I(1), CPIs are both I(2). The question is how can I perform cointegration test if ranks of integration are different? Is it eligible to take the difference concerning CPIs to derive I(1) process and proceed with Johansen test?

Regards

But what if i get cointegration in Trace statistics but not Max eigen value statistics? can we proceed to the VECM model?

why do you use the correlogram and not an ADF or PP in unit root test function in Eviews to test for non-stationarity. The reason i ask is because after lag four in difference on correlogram i can still reject the null hypothesis.

All methods are equally good. But so many lags is not preferred. I would take the decision of SC suggesting one lag....You use the same number of lags for all models such as Johansen, VAR, VECM etc after lag selection....

Hi Sir, allow me ask you a quite trivial question.

Econometric theory states two series integrated of order zero and order one i.e. I(0) and I(1) can't be Cointegrated. Is it necessary to go ahead and run the Johansen test of Cointegration?

My second query is about the lag selection criteria. Normally, after carrying out the various criteria like AIC, LR, SC, HQ and FPE, some people subtract 1 from the answer they get. E.g if the criteria say the optimal lag is say 4, then they subtract one so that the lag to be used in Cointrgration test is 3. The idea is that series to be tested for Cointegration are always in first difference so we need to subtract one from the optimal lag indicated by the lag selection criteria! What is your opinion on this Sir? And what should be my next step now that one of my two series is I(0) while the other is I(1)?

Thanks'

Kigosa Nathan.

In first case you can not run Johansen test as both variables are not I(1). I have not heard about the lag selection criteria that you have mentioned but it sounds new to me. I shall think about it.

Thank you so very much Sir. You're really godsend.

hi sir,

start from 2.17 , when we open the estimate VAR , all variables is key in at the Endogenous Variable column only (like what u do)? or i need to key in my independent variables at Exogenous Variables column ?

Yes you can put some variables are exogenous also...

Hi sir, I ran the VEC model but now my question is where does granger come into effect now. Should run the granger causality test soon as well after VECM or I should consider the causality based on VECM.

Hi,I would like to know that are our variables must have one unit root? In that way, all variables are none-stationary at level and stationary at 1st difference?

Thank you. I would like to invite you to join Hossain Academy Facebook Group at below link and join our group discussion. Thank you. Sayed Hossain from Hossain Academy.

hi Prof Hossain, i'm very appreciate for your tutorials...it's really helpful..can i know in 18:29 minutes, you choose the option 3 (intercept no trend model) why we choose option 3 but not option 1 or 4? correct me if i'm wrong..because i din't learn about Lag selection yet..Thank you =)

Option 3 we have chosen as we assume that our model is like option 3 features..

Sir Kindly upload complete lecture such as : ARDL, Logit & probit model and two stage least square

Hello Sir, can you help me to understand when it is possible to do not add the constant in OLS?

Hi Sir, I'm again back with two burning issues;

1. If two series are I(0) and I(1), do I use the level data when running the test for optimal lag or I have to use the first difference data of the non-stationary variable?

2. If one of the variables has to be transformed to first difference, is that automatically done in VECM, VAR, and when running the test for optimal length or I have to manually /physically do it?

In case of lag selection, you use the data that you have directly whether it is I(0) or I(1). In case of VECM, data automatically convert to first difference but in case of VAR, you need to convert data to first difference manually..

Thanks Mr. Hossain.

I used this method to pick the optimal lag, but the best results from AIC and SC are quite different. AIC suggest 7 lag SC suggest 1. which one should i pick? Im running a johansen model with daily observations so I included 30 lags to test. When I narrow the lag down to 8, both criteria results jump to 1 lag. SO is there something wrong the model? or the lag i picked? how to pick the appropriate lag to run the var model?

Assalamuwalekum Sir,

For lag selection criteria variables will be at level 1(0) or first difference 1(1)

Sir ,is 25years data reliable for testing long run relation through cointegration?

Depends on frequency of your data. If it's quarterly/monthly/daily then yes that is enough. However, if annual you may want to add more years because you only have 25 observations.

Vice informative videos sir... I want to know whether the data entered in the eview is raw data or log of variables ? please help me ?

night Sir , i'am rizky , I was a college student would like to ask how the selection and use of the value of lambda max and lambda trace the Johansen cointegration test , if both of the numbers of cointegration vectors formed is different. eg in lambda trace cointegration vectors are 3 and lambda max cointegration are 2 , then I have to choose which one?

Dear Rizky, Thank you. I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

what if one variable is stationary is level..can go ahead and do johasen cointergration test

If we find that even the 1st difference also cannot accept the null hypothesis so we cannot use the data to run cointegration ? What if we need to test for the long-run relationship. Do you have other options to test for long-run relationship ?

Thank you.

Dear Fah, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

Hello prof hossain.. i saw your tutorials vidéos in youtube , i am so happy for that.. because i need like those vidéos i want to thank you so much. . And i have a question i hope that i find her answer.. plz when we study a stationary of two time séries and we found one stationry at level and other stationary at first différence. . What do we do? I need your solution. . We can't apply cointegration méthode are there any solution Thank you

Dear Nina, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

Dear Sir..

i really impressed with your lectures and your knowledge. here i have some issues that if we have a model having 4 variables in which our 2 variables are stationary at level and 2 are stationary at 1st difference. then what method should we choose?

+Zeeshan Shah

Thank you. I would like to invite you to join Hossain Academy Facebook for greater interaction about economics, finance and econometrics with me. Thank you Sayed Hossain from Hossain Academy. Please join below and post your question.facebook.com/groups/hossainacademy/

2:22 sir why you choose unrestricted VAR?

Hello, what should I do if two of my variables are at 2nd difference and 4 of them are at first difference?

Thank you. I would like to invite you to join Hossain Academy Facebook Group (Data Analysis) at below link and join our group discussion about modelling. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

sir AIC suggest my optimum lag as 8, should I go with it?

Hi sir, Thank you so much for your lectures they are so clear and helpful to many of us on distance learning programs. I ran the VEC model but now my question is where does granger causality come into effect. Should i run the granger causality test separately soon after VECM or I should consider the causality based on VECM. Thank you in advance

Dear Weston, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

Count me in sir

, we choose the number of lagged in the VECM model before or APRET the défferenciation

dir sir

Dear Amina, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

Hello. Thank you very much for the tutorial. My question is: I'm working with 5 variables (all are non-stationary at level and stationary at first difference). When I run the cointegration test, only 3 are cointegrated. Can I still do VECM with all of them? Thank you

nalpergromus You have to run co-integration test by taking all 5 variables, not three.

+nalpergromus hi there I have a similar results, may I know what test did you do in the end?

What if Trace test indicate At most 1 while Max-Eigen test indicates At most 2, which one should be followed?

Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

REPLY

شكرا بزاف

Welcome

hai sir, if my data is already stationary at level, meaning i cant proceed with Johansen test right? So, what other test can I conduct in order to observe the cointegration?

Dear Nurul, Thank you. I would like to invite you to join Hossain Academy Facebook at below link and post your question there. If I know the answer I shall certainly respond. Thank you once again, Sayed Hossain from Hossain Academy. facebook.com/groups/hossainacademy/

If your variables are stationary at levels, there cannot be any cointegration by definition (only I(1) series can be cointegrated)

Hi Sir,

I did the unit root test using Phillip Perron and ADF and both my series were I(1) but now when i follow this video to run the VECM, when i did the correlogram, the other variable does not show stationarity at all (at level and at both 1st and 2nd difference). So can you help here so that i can run my VECM?

That is always a common problem. Results will vary from testing method to testing method. You better take one method as your benchmark to decide result.

Sayed Hossain Thank you very much sir you are doing such a commandable job we appreciate. Will get back with more questions when needed.

Sayed Hossain Hello Sir,

Sir i need to ask this, when carrying out a Johansen Cointegration Test and assuming there is no deterministic trend in the data ( because it is the only that gives me results that there is cointegration) say option 1, does this mean i have to use the same option when estimating VAR? And will the results still be desirable?

Hello Sir, the video was really helpful. However, when I run the co-integration test the none, at most 1, at most 2 are rejected. Only in at most 3 I can accept the null hypothesis. What should I do and what does this mean?

Hello,

The problem I have is that I have only 25 data points for 7 time series. I only have annual data when quarterly would be better. With this data EViews is telling me I am unable to check lag criteria beyond lag=3 due to insufficient data. However, I find this problematic because from the standpoint of theory a higher lag order would be better. Can you assist me?

My question is also why it is telling me I have insufficient data to estimate lag length beyond three...?

KraussHelmut In that case you need quarterly data so that sample size gets increased. You can take more lags now.

hi sir,

i m working on the VECM for the yield in government debt market for which i have identified 10 dependent variables like reporate, inflation, moneysupply etc. but the problem here comes is some of my variables are stationary at 1st difference and some at level . does this mean that these variables are not in same order. i ran lag selection criteria process and it shows around 27(which i guess is too high and not approved by my teacher). how to make them in same order n complete my project.please help

Hi Mittal....Yes they are not in the same order...Lag 27 is not practical at all....try again...

Sayed Hossain

please guide me how should i approach to data of different order variables. thank you

The result may vary between this two tests.

Hi, can you explain how to use the error correction term to explain the lead-lag relation?

I guess I said that if the error correction term is negative and significant meaning that there is a long run causality running from independent variable to dependent variable. You can see my error correction model in this regard

hi sir,

what if two of the variables are stationary at the second difference while the third is stationary at the first difference

So what is the problem if it happens?

Can I proceed to cointegration and causality tests

You can not proceed with Johansen test as variables are integrated of different order. So can not run VECM but you can run VAR model.

can anyone tell is 25 years reliable for testing long run relationship through cointegration ?

Dear Taha, I would like to invite you to join Hossain Academy Facebook at below link to discuss about economics, econometrics and statisti cal models using EVIEWS, STATA, R, SPSS, Minitab, Microfit, Lingo, and Excel. Thank you, Sayed Hossain from Hossain Academy.

facebook.com/groups/hossainacademy/

hi sir, your videos are very helpful for me, but i have one question which i always cannot understand. can you tell us, how to make TSP or DSP in ADF Test? if one variable of 4 is trend stationary, how can I do in the next step? thanks a lot!

i mean if there are 4 variables, one is trend stationary, and the other three are I(1), how can I do with the 4 variables in the next step, for example can i do johansen test and vecm with the 4 variables?

I have not done TSP or DSP, so unable to comment.

Hi Sir, in the case of stationary test, can i use ADF test instead ?

+xxxbeth yeol would it give the same results of correlogram

+xxxbeth yeol Correlogram is another way

+aaa c Yes ADF test is the best for stationary testing.

+Sayed Hossain You can also use correlogram for stationarity test.

+Sayed Hossain Results may differ.