At 14:24, why DXB=0 can deduce DX=0? As B should be a column matrix, we cannot simply to make this deduction. Anyone can make some further explanation about this? Thanks.

The "no multicollinearity" assumption is not needed. With perferctly correlated regressors (eg, when you leave all dummy variables in), the (unique) OLS estimate of any estimable function of the parameters is BLUE under the G-M conditions.

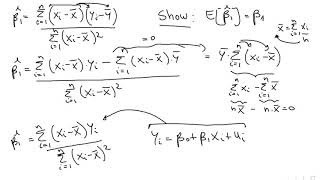

while substituting the expression for beta hat at 10:47, why is there no x transpose? you initially wrote it correct and then ignored the transpose. Am I missing something here?

At 14:24, why DXB=0 can deduce DX=0? As B should be a column matrix, we cannot simply to make this deduction. Anyone can make some further explanation about this? Thanks.

The "no multicollinearity" assumption is not needed. With perferctly correlated regressors (eg, when you leave all dummy variables in), the (unique) OLS estimate of any estimable function of the parameters is BLUE under the G-M conditions.

while substituting the expression for beta hat at 10:47, why is there no x transpose? you initially wrote it correct and then ignored the transpose. Am I missing something here?

It's trivial if you make it transpose or not because eventually it gets cancelled out.

same question.

Where the random sampling assumption at? :)

Well understood ,thank you so much

Nice explanation . thankyou.

Thanks!

Perfect explanation but it’s vry confusing n consideration part

Thanks

senseless approach