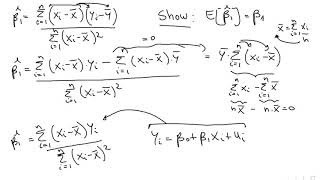

OLS unbiased

ฝัง

- เผยแพร่เมื่อ 11 ก.พ. 2025

- Understanding why and under what conditions the OLS regression estimate is unbiased.

This video screencast was created with Doceri on an iPad. Doceri is free in the iTunes app store. Learn more at www.doceri.com

![โกดำ - วสันต์17 x ไม้เมือง [Official Music]](http://i.ytimg.com/vi/OUg2L4Sx1TY/mqdefault.jpg)