crying while watching your lectures before my finance final. Something I did not understand in two months I learned in 8 minutes. thank god for your videos

the quality of these videos and explanations really make me hate my current professor, and the fact that I spent 3 grand just to have to come back to TH-cam to teach myself.

Thank you for the simple and straight forward explanation. One thing I don't appreciated about textbooks that don't belong in the STEM field is how convoluted they make the concepts with bad explanations and unnecessary jargon. All of your videos are great.

I wish I had found your videos at the beginning of the semester. You are a phenomenal teacher! Thanks for helping me grasp difficult topics in corporate finance.

I agree! I did not get it the first time through. I appreciate your delivery of this finance related material. More yet to learn from you, such as C.A.P.M.

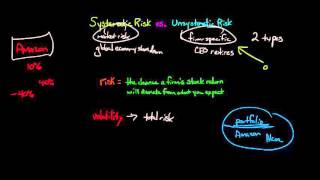

It is possible to get the percentages of a "good" and "bad" economy (but looking at a completed year of which all the stats are available) by checking the past results of a stock index such as the S&P 500 or a Stock Exchange as a whole.

Hello. Thanks for the video. I have 1 question. In my investment research I found 3 ways to calculate Beta and yours is the 4th. The ways I found where using a line regression (in Excel for example), the 2nd was using the formula beta=Covar(Returns, Market returns) / Var(Market returns) and the 3rd was beta=Covar(Returns - Rfr, Market returns - Rfr) / Var(Market returns - Rf). And now with yours counts 4. Which one is correct or which one should be used when? Thanks in advance. JM

There are multiple ways to calculate beta, which get you to the same place. For example, when you run a regression, the beta you obtain is the same as if you divided the covariance by the variance.

@@Edspira Hello, thanks for the reply. That is correct, line regression and the covar / var give the same value, but yours doesn't. When should I use yours instead of the line reg? Thanks. JM

In this video I just provide a simple example with a single company. My goal is not to show you how to calculate beta but to show how to understand what beta is. In this example, the beta is 2.5, which means the company is two and a half times riskier than the market portfolio. If you are trying to calculate the beta of a company in real life, I suggest regressing the monthly (or daily) excess returns of the company on the monthly ( or daily) excess returns of the market portfolio (e.g., the S&P 500).

very well explained...but how to get directed to next following video after this i don't get it... please let me know...if anyone know's it..ill appreciate it.

crying while watching your lectures before my finance final. Something I did not understand in two months I learned in 8 minutes. thank god for your videos

the quality of these videos and explanations really make me hate my current professor, and the fact that I spent 3 grand just to have to come back to TH-cam to teach myself.

I spent $1800 for a review course and still have to come reference his videos

Thank you for the simple and straight forward explanation. One thing I don't appreciated about textbooks that don't belong in the STEM field is how convoluted they make the concepts with bad explanations and unnecessary jargon. All of your videos are great.

I had just finished the final exam, and all of your teaching videos have helped me a lot. I just wana say: Thank you so much! and again

No problem, I'm glad you're doing well!

thank you so much!!

I wish I had found your videos at the beginning of the semester. You are a phenomenal teacher! Thanks for helping me grasp difficult topics in corporate finance.

You should teach professors who teach the art of teaching.

never commented on anything but YOU ARE THE BEST! my prof explained this for 3 courses i didn't get that but i just got it in 10 mins....

Thank you my friend!!

Your explanation is very lucid. It shows that you have thorough understanding of the topic you explain. Many thanks for your videos!

the dude's a professor so of course he understands

Nicely and professionally explained! Can't thank you for making it easy to grasp! Bless you

Greetings from Austria. I have my final exam in corporate finance in few hours. Your videos helped me alot. Just wanna say thank you very much!

You made my understanding of Finance and Accounting, so much easier! THANKS ALOT!

Well done sir. This is the way people should teach. I got it on the first take.

Thanks Moto! Good luck with your studies.

Thank you so much! Your approach to teaching is what I have been searching for.

Awesome. Glad you found the channel!

THANK YOU FOR SAVING MY LIFE BEFORE FINAL

you're a lifesaver! thank you for your videos, your teaching style is simply amazing :)

Glad you think so!

Awesomely explained. Got it first time round. You're gifted!!! As thank you for your time and effort I subscribed and gave a thumbs up :)

I agree! I did not get it the first time through. I appreciate your delivery of this finance related material. More yet to learn from you, such as C.A.P.M.

As always... a great video! Literally got through college be because of you! Thank you 🙏🏼

Shocking how incredible you are compared to my professors. Once again TH-cam saving my grades 🤷♂️

The example was easy to follow but if I wanted to invest in a company where would I find the good and bad economy percentage?

Agree

It is possible to get the percentages of a "good" and "bad" economy (but looking at a completed year of which all the stats are available) by checking the past results of a stock index such as the S&P 500 or a Stock Exchange as a whole.

hey that's some pretty nifty percentage arithmetics around 6:05! I'm 4 years through an engineering degree and I'm intrigued! How'd you do that? :D

oh lol that's just invisible parentheses missed it >

Hello. Thanks for the video. I have 1 question. In my investment research I found 3 ways to calculate Beta and yours is the 4th. The ways I found where using a line regression (in Excel for example), the 2nd was using the formula beta=Covar(Returns, Market returns) / Var(Market returns) and the 3rd was beta=Covar(Returns - Rfr, Market returns - Rfr) / Var(Market returns - Rf). And now with yours counts 4. Which one is correct or which one should be used when? Thanks in advance. JM

There are multiple ways to calculate beta, which get you to the same place. For example, when you run a regression, the beta you obtain is the same as if you divided the covariance by the variance.

@@Edspira Hello, thanks for the reply. That is correct, line regression and the covar / var give the same value, but yours doesn't. When should I use yours instead of the line reg? Thanks. JM

In this video I just provide a simple example with a single company. My goal is not to show you how to calculate beta but to show how to understand what beta is. In this example, the beta is 2.5, which means the company is two and a half times riskier than the market portfolio. If you are trying to calculate the beta of a company in real life, I suggest regressing the monthly (or daily) excess returns of the company on the monthly ( or daily) excess returns of the market portfolio (e.g., the S&P 500).

Hello. Ok, thanks. JM

Very helpful, thank you very much.

This video was so helpful. Thank you so much! :)

Thank you so much!! I appreciate your work

Thank you!

very well explained...but how to get directed to next following video after this i don't get it... please let me know...if anyone know's it..ill appreciate it.

thank you !!

Thanku...

Really explained well..

Most welcome 😊

I like ur explanation very clear 😍

Thank you this was so helpful!! I hope I ace my exam

do Beta values change every day for stocks?

thanks! Great explanation!'

What app do you use?

I feel I can learn anything from you!

Wonderful

Thanks Neha!

thank you sir

We need more videos !!!!

You've helped so much!

i love you man

Where did you get that 30 and 50 percent is that only an estimation?

eisle gomez that is historical data

Remember to hold yourself accountable

Legend !!