💾 Download Free Excel File: ► Grab the file from this video here: ryanoconnellfinance.com/product/probability-of-default-pd-and-loss-given-default-lgd-excel-template/ 🔑 Join this channel to get access to perks & support my work: th-cam.com/channels/Akyj2N9kd0HtKhCrejsYWQ.htmljoin

I was questioning my concepts when you said that the "YTM would be higher than 6%" @2:39 but then my anxiety came down when I saw the computed YTM was less than 6% because the PV>FV Great video! Edit: typo

I didn't mean to spook you with that one haha! I appreciate the feedback. I try to do these videos in 1 take and sometimes miss little slip ups like that lol

This video was extremely helpful in understanding how a bank deals with expected credit loss for a corporate bond where a company potentially defaults. Would the same method apply for an individual client?

Very useful, thank you. Can you please explain dependency of PD on RR, once RR increases (credit positive), PD increases (credit negative) - did not get this one. Thank you 🙏

My pleasure! The CFA Institute highlights, "To balance a higher recovery rate, there's a need for an increased default probability. Typically, when looking at the same price and credit spread, there's a direct correlation between the assumed probability of default and the recovery rate." Let's break this down: Consider the credit spread as a barometer of risk, factoring in both recovery rate and default probability. Now, when the context mentions "for a given price and credit spread," imagine two bonds priced similarly with equivalent risk, but Bond (A) has a greater likelihood of default than Bond (B). So, which bond, (A) or (B), offers a better recovery rate? Bond (A) would likely have the superior recovery rate. This is because, to maintain an identical spread as Bond (B), there must be greater assurance of recuperating more funds in case of a default. Hence, as the default rate surges, the recovery rate must also rise to preserve that consistent "price and credit spread." I hope that sheds light on the concept. If you have further queries or need more clarity, feel free to ask!

@@RyanOConnellCFA thank you so much for your swift response. I was just looking and if we have RR of 80% and spread 1,2%, PD would be e.g. 6% and equivalents CCC+ rating, which is somehow to much for a client/bond with such a high RR ratio.

@@Penelopa13 You bring up a good point. If we consider a Recovery Rate (RR) of 80%, it does suggest a relatively low-risk scenario since a significant portion of the funds can be recovered in the event of default. A spread of 1.2% combined with a Probability of Default (PD) of 6% translating to a CCC+ rating might seem stringent for a bond with such a promising RR. However, it's essential to note that while RR is a critical component, other factors influencing the rating include the overall health of the issuer, industry dynamics, macroeconomic factors, and historical default rates for similar bonds. Even with a high RR, if other parameters paint a risky picture, the PD might be adjusted accordingly.

@@RyanOConnellCFA thank you so much! You confirmed my thoughts, and helped me a lot! Firstly, mathematically thinking with such a high RR spread to be relatively low and secondly, as you mentioned, rating to capture other parameters as well. I am considering, this way of PD calculation, when you do not have other data is very useful (like was my case), but in general rating should incorporate other parameters. Thank you again 🙏

@@selimc3347 Yes, there are a lot of other good programs you can use for data analysis but I find Excel to be the most simple and easy. Google sheets is similar and free but likely lower quality. Then for automation, Python and R are both very good free options that take more skill to learn PROGRAMMING LANGUAGES

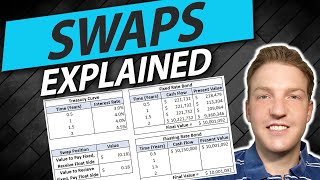

one thing I dont understand that in corporate bonds you simply mentionedYTM without calculation i.e 7 percent but in risk free bind you calculated it ? why? am i missing something

The yield to maturity (ytm) of a corporate bond will be based on the risk of the bond. You can characterize it as corporate ytm = risk free rate + risk premium where the risk premium is a reflection of how much risker the corporate bond is than the risk free bond

To estimate the recovery rate in a finance problem related to credit risk, you typically analyze historical data on defaulted loans or bonds to determine the average percentage of the loan amount that was recovered post-default. This involves examining factors like the seniority of the debt, the quality of the collateral, and the overall financial health of the borrower.

To estimate the recovery rate in a finance problem related to credit risk, you typically analyze historical data on defaulted loans or bonds to determine the average percentage of the loan amount that was recovered post-default. This involves examining factors like the seniority of the debt, the quality of the collateral, and the overall financial health of the borrower.

@@RyanOConnellCFA I found historical recovery rates from Moody's to be helpful. Page 5: www.moodys.com/sites/products/defaultresearch/2006600000428092.pdf

💾 Download Free Excel File:

► Grab the file from this video here: ryanoconnellfinance.com/product/probability-of-default-pd-and-loss-given-default-lgd-excel-template/

🔑 Join this channel to get access to perks & support my work: th-cam.com/channels/Akyj2N9kd0HtKhCrejsYWQ.htmljoin

in six minutes you have solved a problem am searching for 2 hours

thank you for your effort

That is what I love to hear! Thank you for the feedback

Very instructive and informative video. Thank you so much for sharing

I appreciate the feedback and thank you for watching William

I was questioning my concepts when you said that the "YTM would be higher than 6%" @2:39 but then my anxiety came down when I saw the computed YTM was less than 6% because the PV>FV

Great video!

Edit: typo

I didn't mean to spook you with that one haha! I appreciate the feedback. I try to do these videos in 1 take and sometimes miss little slip ups like that lol

Thanks for sharing, this helped with my revision!

You're very welcome Matthew!

Hi Ryan, can you show EL computation for loans?

Hello you can see the Expected Loss (EL) calculation at @5:06

Great video 🎉🎉🎉🎉

This video was extremely helpful in understanding how a bank deals with expected credit loss for a corporate bond where a company potentially defaults. Would the same method apply for an individual client?

This is awesome thanks!!!

My pleasure Peter!

Very good video. It helps me a lot.

Glad to hear that!

Great video!

Much appreciated Keenan!

Great Video

Thank you sam

Linking first semester & this semester with one chart is mathgod levels.

Haha thank you!

Very useful, thank you. Can you please explain dependency of PD on RR, once RR increases (credit positive), PD increases (credit negative) - did not get this one. Thank you 🙏

My pleasure!

The CFA Institute highlights, "To balance a higher recovery rate, there's a need for an increased default probability. Typically, when looking at the same price and credit spread, there's a direct correlation between the assumed probability of default and the recovery rate."

Let's break this down:

Consider the credit spread as a barometer of risk, factoring in both recovery rate and default probability.

Now, when the context mentions "for a given price and credit spread," imagine two bonds priced similarly with equivalent risk, but Bond (A) has a greater likelihood of default than Bond (B). So, which bond, (A) or (B), offers a better recovery rate?

Bond (A) would likely have the superior recovery rate. This is because, to maintain an identical spread as Bond (B), there must be greater assurance of recuperating more funds in case of a default. Hence, as the default rate surges, the recovery rate must also rise to preserve that consistent "price and credit spread."

I hope that sheds light on the concept. If you have further queries or need more clarity, feel free to ask!

@@RyanOConnellCFA thank you so much for your swift response.

I was just looking and if we have RR of 80% and spread 1,2%, PD would be e.g. 6% and equivalents CCC+ rating, which is somehow to much for a client/bond with such a high RR ratio.

@@Penelopa13 You bring up a good point. If we consider a Recovery Rate (RR) of 80%, it does suggest a relatively low-risk scenario since a significant portion of the funds can be recovered in the event of default. A spread of 1.2% combined with a Probability of Default (PD) of 6% translating to a CCC+ rating might seem stringent for a bond with such a promising RR.

However, it's essential to note that while RR is a critical component, other factors influencing the rating include the overall health of the issuer, industry dynamics, macroeconomic factors, and historical default rates for similar bonds. Even with a high RR, if other parameters paint a risky picture, the PD might be adjusted accordingly.

@@RyanOConnellCFA thank you so much! You confirmed my thoughts, and helped me a lot!

Firstly, mathematically thinking with such a high RR spread to be relatively low and secondly, as you mentioned, rating to capture other parameters as well.

I am considering, this way of PD calculation, when you do not have other data is very useful (like was my case), but in general rating should incorporate other parameters.

Thank you again 🙏

@@Penelopa13 Absolutely, that makes sense! And it is my pleasure. Hopefully talk to you again soon!

Thank you for your video, that is very good. can you say that if there is any program to calculate this value or risk ? For example R, E-views...

Hey Selim, could you rephrase the question? I'm not sure I understand it

In this video, you explained everything in excel. Is there any other program like Excel which we can use for estimate risk and analyse ?

@@selimc3347 Yes, there are a lot of other good programs you can use for data analysis but I find Excel to be the most simple and easy. Google sheets is similar and free but likely lower quality. Then for automation, Python and R are both very good free options that take more skill to learn PROGRAMMING LANGUAGES

one thing I dont understand that in corporate bonds you simply mentionedYTM without calculation i.e 7 percent but in risk free bind you calculated it ? why? am i missing something

The yield to maturity (ytm) of a corporate bond will be based on the risk of the bond. You can characterize it as corporate ytm = risk free rate + risk premium where the risk premium is a reflection of how much risker the corporate bond is than the risk free bond

How do you calculate the recovery rate

To estimate the recovery rate in a finance problem related to credit risk, you typically analyze historical data on defaulted loans or bonds to determine the average percentage of the loan amount that was recovered post-default. This involves examining factors like the seniority of the debt, the quality of the collateral, and the overall financial health of the borrower.

Could you share the excel sheet? Thanks

The link to download the file automatically is in the description of the video Kais

Thank you!

How to estimate the recovery rate? That seems to be the difficult part.

To estimate the recovery rate in a finance problem related to credit risk, you typically analyze historical data on defaulted loans or bonds to determine the average percentage of the loan amount that was recovered post-default. This involves examining factors like the seniority of the debt, the quality of the collateral, and the overall financial health of the borrower.

@@RyanOConnellCFA I found historical recovery rates from Moody's to be helpful. Page 5: www.moodys.com/sites/products/defaultresearch/2006600000428092.pdf

Why not just multiply EAD and Credit Spread to arrive at EL?

You can definitely do that and get the same answer