Thank you for the video. I have a question: considering put-call parity, if the implied volatilities of out-of-the-money puts exceed the implied volatilities of out-of-the-money calls at similar distances from the current stock price then necessarily the implied volatility of in the money calls should exceed the implied volatilities of in the money puts at similar distances from the current stock price. Is it right? Thank you very much

Yes, correct according to put-call parity. However with volatility smirks (mostly) we've found empirical evidence that the put-call parity might not hold true. This is where behavioral finance comes in to explain some of those concepts. I hope this helps!

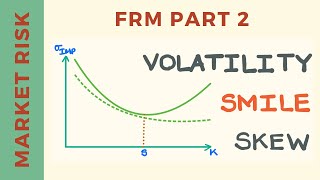

Thanks, the first 10 minutes cleared up volatility skew/smile for CFA level 3

Appreciate

Great effort sir,

Really appriciate your valueable contribution.

You're welcome and good luck on the exam!

This video was excellent. Thank you so much!

Thank you for the video. I have a question:

considering put-call parity, if the implied volatilities of out-of-the-money puts exceed the implied volatilities of out-of-the-money calls at similar distances from the current stock price then necessarily the implied volatility of in the money calls should exceed the implied volatilities of in the money puts at similar distances from the current stock price.

Is it right?

Thank you very much

Yes, correct according to put-call parity. However with volatility smirks (mostly) we've found empirical evidence that the put-call parity might not hold true. This is where behavioral finance comes in to explain some of those concepts. I hope this helps!

Thank you very much!

📙💯