Hi Ulzil. Can I recommend that you watch the next episode (Episode 13) where I hopefully answer your question in quite a lot of detail. You can find it here: th-cam.com/video/sjm60E3IXms/w-d-xo.html Hope this helps

Having to optimize 4 parameters, (if I understood) it is better to do two optimizations with two parameters at a time. Parameters: A (A1-A10) B(B1-B10) C(C1-C10) D(D1-D10) Therefore, first optimization A and B, and second C and D. Example first scan best result A3 B9, the second scan in order to optimize C and D will be done with the parameters of first scan A3 and B9. Is it correct? Of course doing a walk forward optimization TF5m 4mounth+1 I'll repeat it for 5 times (forward 1 month per time) as your webinar WFO. Is it correct?

Great stuff...u Say un one of tour videos that one shouldn't optimizw more than at most 3 parameters...but what happens ir i'm teeting a strategy which has Lot of parameters...more than 10...moreover what happens i'm the scenario un which i'm looking for the Best combinación of múltiple strategies...with fixed parameters...

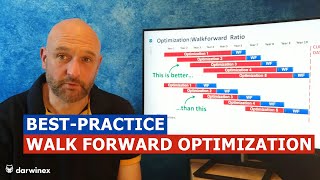

Great content. What does it mean if the walk forward (out-sample) performance is better than optimized (in-sample) performance? Similarly, what if each phase seems to improve? I would expect performance to degrade over time. Thank you for this!

Wouldn't it also be viable to have a long optimization phase and having a system which is adjusted all market conditions? Suffering lower returns short term seems like a good trade-off for a system that can perform well regardless of market conditions. Curious is all. Thanks for the vids!

Hi Luke. I think I understand what you mean. So during the longer opt period, your system would have an ability to adapt real-time based on what the market is doing, right? If so then yes, absolutely. This is a very viable approach. But if your system doesn't do this , then WFA is a great alternative to stay in tune with conditions. Hope this helps. Cheers, Martyn

In the other hand... I think the opposite, I strongly believe, that any model specifically designed for a market condition (I.E ranging market) that trades on that specific condition is healthier for the equity curve rather than having a model that trades at any market condition, that way you can design another model for example, designed for momentum trading, and *bring up the concept of diversification up a little bit better...* I don't remember where I've heard that trying to design a model with great performance in all market conditions is just innocent and such model should not be attempted to achieve. Speaking of... Martyn Tinsley here have made a few videos about how important "Diversification" is! Check 'em out!

Clear and useful.

As always, thanks for the feedback Leon

This great work. Thank you for this.

What is best period interval for novice algo traders?

Hi Ulzil. Can I recommend that you watch the next episode (Episode 13) where I hopefully answer your question in quite a lot of detail. You can find it here: th-cam.com/video/sjm60E3IXms/w-d-xo.html

Hope this helps

impossible to be clearer

Having to optimize 4 parameters, (if I understood) it is better to do two optimizations with two parameters at a time.

Parameters: A (A1-A10) B(B1-B10) C(C1-C10) D(D1-D10)

Therefore, first optimization A and B, and second C and D.

Example first scan best result A3 B9, the second scan in order to optimize C and D will be done with the parameters of first scan A3 and B9.

Is it correct? Of course doing a walk forward optimization TF5m 4mounth+1 I'll repeat it for 5 times (forward 1 month per time) as your webinar WFO.

Is it correct?

Great stuff...u Say un one of tour videos that one shouldn't optimizw more than at most 3 parameters...but what happens ir i'm teeting a strategy which has Lot of parameters...more than 10...moreover what happens i'm the scenario un which i'm looking for the Best combinación of múltiple strategies...with fixed parameters...

Great content. What does it mean if the walk forward (out-sample) performance is better than optimized (in-sample) performance? Similarly, what if each phase seems to improve? I would expect performance to degrade over time. Thank you for this!

Can i do it in metastock? Has metastock's system tester included Walk-Forward Analysis in its backtesting and optimization?

Where can I get the excel walk-forward file?

This would be hard to do on the daily timeframe because of the low historical data. I trade on the daily timeframe because it’s the best timeframe

Wouldn't it also be viable to have a long optimization phase and having a system which is adjusted all market conditions? Suffering lower returns short term seems like a good trade-off for a system that can perform well regardless of market conditions. Curious is all. Thanks for the vids!

Hi Luke. I think I understand what you mean. So during the longer opt period, your system would have an ability to adapt real-time based on what the market is doing, right? If so then yes, absolutely. This is a very viable approach. But if your system doesn't do this , then WFA is a great alternative to stay in tune with conditions. Hope this helps. Cheers, Martyn

In the other hand... I think the opposite, I strongly believe, that any model specifically designed for a market condition (I.E ranging market) that trades on that specific condition is healthier for the equity curve rather than having a model that trades at any market condition, that way you can design another model for example, designed for momentum trading, and *bring up the concept of diversification up a little bit better...* I don't remember where I've heard that trying to design a model with great performance in all market conditions is just innocent and such model should not be attempted to achieve. Speaking of... Martyn Tinsley here have made a few videos about how important "Diversification" is! Check 'em out!