Learning From Financial Disasters (FRM Part 1 2023 - Book 1 - Chapter 9)

ฝัง

- เผยแพร่เมื่อ 14 ก.ค. 2024

- For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: analystprep.com/shop/unlimite...

AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams

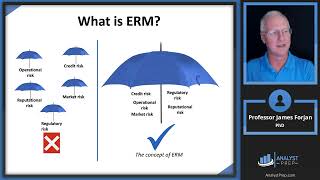

After completing this reading, you should be able to analyze the key factors that led to and derive the lessons learned from case studies involving the following risk factors:

- Interest rate risk, including the 1980s savings and loan crisis in the US

Funding liquidity risk, including Lehman Brothers, Continental Illinois, and Northern Rock

- Implementing hedging strategies, including the Metallgesellschaft case

Model risk, including the Niederhoffer case, Long Term Capital Management, and the London Whale case

- Rogue trading and misleading reporting, including the Barings case

- Financial engineering and complex derivatives, including Bankers Trust, the Orange County case, and Sachsen Landesbank

- Reputational risk, including the Volkswagen case

- Corporate governance, including the Enron case

- Cyber risk, including the SWIFT case

0:00 Introduction

1:07 Learning Objectives

1:38 Savings and Loans (S&Ls) Associations

12:34 Lehman Brothers

20:27 Northern Rock

21:22 Funding Liquidity Risk: Lessons

23:08 Hedging Strategies

26:30 Metallgesellschaft

30:23 The Niederhoffer Put Options

35:47 The London Whale

43:24 Orange County

44:38 Sachsen Landesbank

46:31 Volkswagen Repuational Risk

48:38 Enron Corporate Governance

51:03 The SWIFT Case Cyber Risk

Sir ,some doubt regarding contango and backwardation I think so that you have mixed contango and backwardation

hey Professor Forjan, thanks for uploading these videos. tks also for the whole AnalystPrep team.

Do you guys make any money out of this? I watch these lectures so much, and sometimes I even feel bad about not having to pay for any of this.

Hi Mayron. Yes, to get access to all video lessons (Part I & Part II), plus study notes, practice questions, mock exams, and formula sheets, you can purchase one of our packages here: analystprep.com/shop/unlimited-package-for-frm-part-i-part-ii/

26:13 that's contango, isn't it?

Thanks for the fast 2020 update professor. I am currently considering purchasing the FRM part 1, part 2 full package at Analyst prep website. Turns out that your lecture videos and the simple format of study material suited well for me. However, I was curious if the FRM part 2 videos will also be posted on Analyst prep or you tube later on? Anyways thanks for the great lectures and wish you the best!

Thank you for those kind words. We will keep posting FRM part 2 video lectures on TH-cam until we have completed them. Once completed, we'll put them on the AnalystPrep website.

Repsected Professor, just a small question.

What can we expect of the FRM L1 paper in Nov 2020 to be on the same deadlines or can we expect a small postponement .

Thanking you for your revert :)

We expect it to be on the November date announced earlier this month, which gives you another 6 months to study for the exam.

Dear Professor,

Thanks for uploading the lecture. I have one doubt about the Niederhoffer case. You illustrated that if somebody owns an out-of-the-money put option, he would tell the seller (Niederhoffer) that he (buyer) wants to by S&P 500. My doubt is, the buyer of put option would exercise his right to sell S&P instead of buying it.

Yes, correct. Sorry for the confusion. The buyer of the put can SELL the S&P 500 and the seller (Niederhoffer) of the put option has unlimited downside risk in case the S&P 500 keeps losing value (which it did in this case).

Thank you professorr! I have a question about S&L case. when interest rates rised , why S&L didn't raise their interest rates for new mortgages and offset the effect of the higher interest rate of funds? I know they had mortgages issued but it was possible to increase interest risk for new mortgages? Thank you again!

@Zean Li in that case if s and l don't have new opportunities then why he was borrowing at increment highr rate

Dear Sir,

I liked your video very much. However, I have one confusion. You defined backwardation as a situation when futures price is above the spot price, while you have termed contango as a scenario in which futures price goes below the spot price. However, in this GARP 2020 book it has been defined just the opposite. Even in chapter 7 of the book Futures and Options, and chapter 2 of Essentials of Risk Management it has been defined similarly. Kindly elaborate.

Hey, so yeah I think too that sir made a mistake in that part because backwardation is when the price is lower than the spot price. But what he said was correct, the firm made a profit due to backwardation and it is obvious cause they were paying less than what the market was moving at.