import pandas_datareader.data as web x = web.DataReader ('lmt', 'yahoo', '2013-01-01', '2015-01-01') And after that, use "x.Close" instead of just "x". I had to deal with this filter, figured it out and now can say that the video is a lil bit misleading. Kalman filter does require user provided inputs that may completely change the result: observation covariance and transition covariance. Idk why they used 1 and 0.01 in the video, but try changing these values and you'll see. Commenting just to save your time.

I had to deal with this filter, figured it out and now can say that the video is a lil bit misleading. Kalman filter does require user provided inputs that may completely change the result: observation covariance and transition covariance. Idk why they used 1 and 0.01 in the video, but try changing these values and you'll see. Commenting just to save your time.

4:45 Where is defined the function *get_pricing()*

I tried to run the notebook and got an error

import pandas_datareader.data as web

x = web.DataReader ('lmt', 'yahoo', '2013-01-01', '2015-01-01')

And after that, use "x.Close" instead of just "x".

I had to deal with this filter, figured it out and now can say that the video is a lil bit misleading. Kalman filter does require user provided inputs that may completely change the result: observation covariance and transition covariance. Idk why they used 1 and 0.01 in the video, but try changing these values and you'll see. Commenting just to save your time.

Hi , the links of the notebooks are not working now , could you please have a look into it

+1 would be greatly appreciated

I had to deal with this filter, figured it out and now can say that the video is a lil bit misleading. Kalman filter does require user provided inputs that may completely change the result: observation covariance and transition covariance. Idk why they used 1 and 0.01 in the video, but try changing these values and you'll see. Commenting just to save your time.

@@DragonGiveMeFire How to optimize this parametrization of R (noise covariance) and delta?

Also, in the example given around 5:30, how far back does the Kalman filter measure data points to create its estimation?

the first 20 data points of the spread

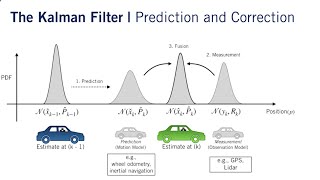

Nice intuitive intro to Kalman filters

Good explanation

Thank you so much for the nice video. Would you pls tell us what software is used here to generate the results and graphs?

It is some sort of custom jupyter notebook instance and to generate the graphs he propably used the python module matplotlib I guess

@@ralf7131 The Kalman filter is implemented in the Python library pykalman.

nice