thank you very much, I did a comparative research between vasicek model (equilibrium) and ho lee model (no arbitration) and this explanation helped me understand more

You'll need to numerically implement your chosen model (for example, using binomial trees), pick appropriate values of the model's parameters (for example, k, theta, sigma for Vasicek model) and then using your implementation price zero coupon bonds of progressively longer maturities. These model implied bond prices can be inverted to calculate spot rates for different maturities i.e. your model implied term structure.

@@finRGB Hi, Can we determine the model parameters for any term structure model like vasicek through a simple min sum of squared error method between actual yield and derived yield?

thank you very much, I did a comparative research between vasicek model (equilibrium) and ho lee model (no arbitration)

and this explanation helped me understand more

Glad you found the video helpful, Fabian.

Nicely explained. Thanks a lot !!

Thanks for the appreciation, Brijesh.

Amazing explanation

Thank u for the appreciation, Nitin.

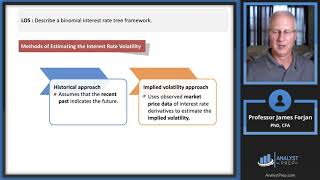

How does one build a term structure from a short-rate model like Vasicek or CIR?

You'll need to numerically implement your chosen model (for example, using binomial trees), pick appropriate values of the model's parameters (for example, k, theta, sigma for Vasicek model) and then using your implementation price zero coupon bonds of progressively longer maturities. These model implied bond prices can be inverted to calculate spot rates for different maturities i.e. your model implied term structure.

@@finRGB Hi, Can we determine the model parameters for any term structure model like vasicek through a simple min sum of squared error method between actual yield and derived yield?