Properties of Options (FRM Part 1 2025 - Book 3 - Chapter 13)

ฝัง

- เผยแพร่เมื่อ 27 ธ.ค. 2024

- For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: analystprep.co...

AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams

After completing this reading, you should be able to:

Identify the six factors that affect an option’s price.

Identify and compute upper and lower bounds for option prices on

non-dividend and dividend paying stocks.

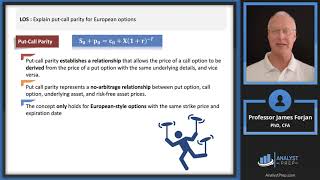

Explain put-call parity and apply it to the valuation of European and

American stock options, with dividends and without dividends, and

express it in terms of forward prices.

Explain and assess potential rationales for using the early exercise

features of American call and put options.

sir at time of lower bound, how do you get arbitrage of $2. Please tell and explain at time of expiration.

@14:09 the Professor says, that in order to determine the lower bound of the call option we can think of buying the stock after we had bought the call option. And all of the sudden we end up subtracting the PV of strike price (what actually is that, how do you interpret PVing the strike price) from the stock price to reach the lower limit.

This is just completely abstract to me. Why would I buy the stock when I'm having the call option already? With what amount of money (K, or K - C, or any other value)? And what does it have to do with anything about the price of a call option I had already bought?

sir why deep ITM can sell less than their actual value

sir i guess your PV for lower bound call option is not correct (40/(1+10%)^-0.5=38.13.... not 36.36