so far the best lognormal of price and relation of returns explained! Thanks a lot! Two Questions please: 6:42 1) so first the simple return delta_S/S is Normal, and the Log(ST/S0) the log-return is also normal? Both return forms are normal? 2) is it typo that variance is always delta_t, it should be scaled to match T in your two logrithm equation right? Thank you for advice!

@11:00 why do we need to introduce volatility into return? If bsm assumes mean return as risk free rate u(mu), then shouldn't it be 'risk free'? Why should it be affected by volatility?

first, mu isn't necessarily the risk-free rate. its the expected arithmetic mean of the change in stock price over time. second, i think subtracting volatility is just a clever way to transform from arithmetic to geometric mean. i imagine it just comes out of the math of trying to equate the two approaches.

@@SpindicateAudio thanks for reply. I am talking about mu from bsm pov. In bsm model assumption, isn't mu geometric mean for risk free rate 'r'? My question is it sounds counterintuitive to call it risk free rate and adjust it with volatility.

This mysterious half sigma squared has nothing to do with BSM . It is actually coming from ITO lemma. This lemma helps us to switch btw different stochastic processes. For example if a stock follows SDE (also known as GBM process) we can switch to process log(stock) by applying the lemma. Just think about this lemma as a Taylor expansion, when we cancel all very-very small terms. Basically what is left after that is this drift mu and minus half vol squared. All the other terms are negligible. But the thing is if someone offers a very simple derivative : you pay me X usd today and I will pay you the price of Amazon in three months (just price of the stock, very simple. No conditions, no question asked etc). And you try to value such derivative today, then strangely enough you will get a price LESS than the price of Amazon today (thank to this minus half vol squared). Of course this is a total absurd.

If you have not found a response to the inquiry; the quickest method to create the formulas in Excel is by using the INSERT->Equation menu option. The best way is to use LaTeX. I love LaTex; I began using it over two decades ago, at NASA, as a summer intern, when it was just TeX.

can you please request in our forum, here is the thread for this videowww.bionicturtle.com/forum/threads/t4-10-lognormal-property-of-stock-prices-assumed-by-black-scholes.22469/

so far the best lognormal of price and relation of returns explained! Thanks a lot!

Two Questions please: 6:42

1) so first the simple return delta_S/S is Normal, and the Log(ST/S0) the log-return is also normal? Both return forms are normal?

2) is it typo that variance is always delta_t, it should be scaled to match T in your two logrithm equation right?

Thank you for advice!

You're welcome! Thank you for watching :)

Thank you so much. This video clarified a lot of confusion around lognormal dist'n!

Great video, David, as always!

Although, your audio output was only in the left speaker.

Yeah, I find that out today as well, then I thought my mac is broken, but it works fine when playing other channel's video

9:00 this is empirically determined n the Fame French model

@11:00 why do we need to introduce volatility into return? If bsm assumes mean return as risk free rate u(mu), then shouldn't it be 'risk free'? Why should it be affected by volatility?

first, mu isn't necessarily the risk-free rate. its the expected arithmetic mean of the change in stock price over time.

second, i think subtracting volatility is just a clever way to transform from arithmetic to geometric mean. i imagine it just comes out of the math of trying to equate the two approaches.

@@SpindicateAudio thanks for reply. I am talking about mu from bsm pov. In bsm model assumption, isn't mu geometric mean for risk free rate 'r'? My question is it sounds counterintuitive to call it risk free rate and adjust it with volatility.

This mysterious half sigma squared has nothing to do with BSM . It is actually coming from ITO lemma. This lemma helps us to switch btw different stochastic processes. For example if a stock follows SDE (also known as GBM process) we can switch to process log(stock) by applying the lemma. Just think about this lemma as a Taylor expansion, when we cancel all very-very small terms. Basically what is left after that is this drift mu and minus half vol squared. All the other terms are negligible. But the thing is if someone offers a very simple derivative : you pay me X usd today and I will pay you the price of Amazon in three months (just price of the stock, very simple. No conditions, no question asked etc). And you try to value such derivative today, then strangely enough you will get a price LESS than the price of Amazon today (thank to this minus half vol squared). Of course this is a total absurd.

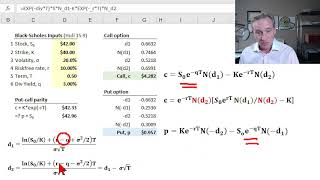

Thank you for the video. Question: shouldn’t be σ^2T the variance of ln(ST/S0) and of ln ST?

so the y axis says that the mean return is 16%? thanks

Thanks for the lecture sir. How did you get those equations ? Is there any video on that. ?

If you have not found a response to the inquiry; the quickest method to create the formulas in Excel is by using the

INSERT->Equation menu option.

The best way is to use LaTeX. I love LaTex; I began using it over two decades ago, at NASA, as a summer intern, when it was just TeX.

What do the symbols (Phi) in the equation represent?

How do you show that a random variable is log normally distributed if the log ratio of it is normal?

hi great video again, but I couldn't the link to the excel though?

can you please request in our forum, here is the thread for this videowww.bionicturtle.com/forum/threads/t4-10-lognormal-property-of-stock-prices-assumed-by-black-scholes.22469/

great video

Thank you for watching!

My right ear is lonely :/

my left ear did

Mistakes:

variance is sigma square x T not delta t.

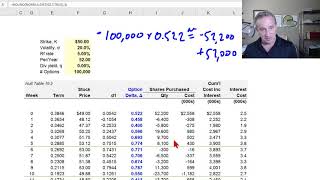

The excel sheet formaula there is extra sigma.