Why did you assume \sum(x_i - x_bar) = 0 in @5:00 but then take a conditional expectation of the same variables in @8:00 ? I would have just assumed they both equal to zero and have the \sum(xi-x_bar)^2 cancel. You would be left with beta_1_hat = beta_1. Great video either way. I am just not sure why you didn't assume \sum(x_i - x_bar) = 0 for both cases.

I am not sure I understand your question ? Are you asking if the proof applies to multivariate regression ? For multivariate regression, there is a similar proof but using Matrix algebra.

@@RemiDav Hi, have made any video to apply this method for multivariate regression, for example, 2 variables regression? I think we need to use matrix like your suggestion, but it is too complicated to me to make the calculation. Thank you

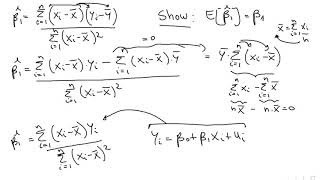

Thank you for this video, really helpful. Just a small doubt, in the video summation of (xi - xbar) is constant because for the condition on x (which has a constant value, say C), (xi - xbar) = (c - xbar) and thus we are left with E[u|x].

I don't understand your question. You would have to tell me which elements exactly you are referring to. Note that if you are a Bayesian statistician, everything can be considered a random variable.

@@RemiDav I mean that in general case every observation from random sampling is random variable; so at counting can we consider observations as random variables?

I genuinely love you for this

I love all your videos. I have been struggling with some concepts

Why did you assume \sum(x_i - x_bar) = 0 in @5:00 but then take a conditional expectation of the same variables in @8:00 ? I would have just assumed they both equal to zero and have the \sum(xi-x_bar)^2 cancel. You would be left with beta_1_hat = beta_1.

Great video either way. I am just not sure why you didn't assume \sum(x_i - x_bar) = 0 for both cases.

Why the sum of (xi-x(bar)) is constant? Here, xi takes different values!!

And why you take conditional expectation?

Does this apply to multivariate regressions as well as univariate? Thank you, great videos!

I am not sure I understand your question ? Are you asking if the proof applies to multivariate regression ?

For multivariate regression, there is a similar proof but using Matrix algebra.

@@RemiDav Hi, have made any video to apply this method for multivariate regression, for example, 2 variables regression? I think we need to use matrix like your suggestion, but it is too complicated to me to make the calculation. Thank you

@@TheVista255 I didn't make any matrix version, sorry.

Thank you for this video, really helpful. Just a small doubt, in the video summation of (xi - xbar) is constant because for the condition on x (which has a constant value, say C), (xi - xbar) = (c - xbar) and thus we are left with E[u|x].

6:12 How Do you get to the last line from the previous one? What is the operation?

distribute the 1/sum(...) in the parenthesis and simplify.

@@RemiDav Thanks for that! It was under my nose really! Just got it 5 minutes ago after a closer look.

I really enjoy your videos!

Cheers!

can we consider elements in quatation of estimator b1 as random variables?

I don't understand your question. You would have to tell me which elements exactly you are referring to.

Note that if you are a Bayesian statistician, everything can be considered a random variable.

@@RemiDav I mean that in general case every observation from random sampling is random variable; so at counting can we consider observations as random variables?

@@RemiDav i meant exactly what this guy did on his video th-cam.com/video/5tMMESxjDBg/w-d-xo.html :)

you made me understand, thank you...do you have any Video on LM statistics to shARE PLEASE

Are you talking about the Lagrange Multiplier test ?

yes sir

Why the sample y is equal to the population Y

Please indicate a time in the video