I already protect myself by buying an otm call by making a bear call spread and building a bull put spread on the other side. What is the difference of defending myself by buying the underlying? Great video thanks .

just wonder in what type of market movement would MM start to hedge their written calls with futures (eg. ES for SP500) vs SPY ETF shares for index types operation?

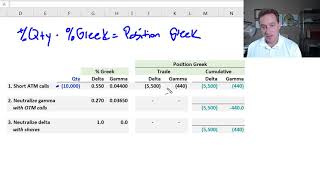

This is good info but represents only one side of the equation. The full picture for any MM is neutralizing calls AND puts not just calls. When the open interests of the calls and the puts are un-equal ATM and or shifted across strike prices this becomes a very interesting exercise for the MMs.

When the price moves up or down the Delta changes (of that specific call). If that is the case, wouldn't you say that the MM needs to keep adjusting its hedge for every $1 stock move? For example, if the stock moves up $1 and Delta went up too, they need to buy more stocks. If the price went down $1 the delta went down and they can sell the change back to the market.

I’m still learning so forgive me if my question is overly basic. When the stock price moves wouldn’t delta change so we’re no longer perfectly delta hedged? Does delta actually have a $0 impact or are you implying that the delta at the original point is hedged and the new delta created through gamma is the expense in the gamma column?

Why do you think the majority of trading is automated? Mm delta hedging. MMs don't take losses, they simply adjust long/short exposure tick by tick to account for their short p/c positions. Every high p/c environment ends in a short term spike eod while mm cover hedges as contracts close/expire

how can MM hedge against whipsaw movement ? seem like MM can only hedge one direction but when the Underlying reverse creating a whipsaw movement . the MM is out of luck. Or is there a way MM can hedge when the underlying make a u-turn? my best guess is they dumping the shares so they can be delta neutral again? But when will they dump the shares? at what trigger point?

Thank you so much for the visuals and breakdown! I have just started my studies in this area, and was wondering what the difference would be using the binomial pricing model, and could you also please explain the significance to MMs of 1 Delta? From what I have found thus far it appears to be the future price of the underlying. Awesome job, David, and thanks again!

Do MM always hedge? Or do they keep track of winning and losing traders? I see Unusual options activity all the time but MM hedge only a small percentage of them. Why would that be?

"MM hedge only a small percentage of them" - how do you know this? "Unusual activity" on a particular strike may be partially hedged by the contracts on the other side of the option chain, i.e. puts if the UA is on calls. It is one massive, dynamic system that encompasses many inputs and outputs including the moneyness/delta of the strike. OTM contracts hedged less due to lower delta, etc.

How would you be possibly knowing which part of the open interest the MM is short or long? Because without that information you will never know their true exposure

Also there’s a retail investor making a NOPE index to roughly calculate the delta exposure of MM by using Vol times delta and summarizing all strikes with all expirations. Clearly it’s very misleading isn’t?

wow, this is probably the most insightful options hedging video i've seen. subscribed!

This is gold! Thank you for posting this.

I already protect myself by buying an otm call by making a bear call spread and building a bull put spread on the other side.

What is the difference of defending myself by buying the underlying?

Great video thanks .

Damn this helped me visualize and understand it very wel

just wonder in what type of market movement would MM start to hedge their written calls with futures (eg. ES for SP500) vs SPY ETF shares for index types operation?

This is good info but represents only one side of the equation. The full picture for any MM is neutralizing calls AND puts not just calls. When the open interests of the calls and the puts are un-equal ATM and or shifted across strike prices this becomes a very interesting exercise for the MMs.

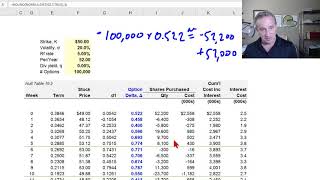

When the price moves up or down the Delta changes (of that specific call). If that is the case, wouldn't you say that the MM needs to keep adjusting its hedge for every $1 stock move? For example, if the stock moves up $1 and Delta went up too, they need to buy more stocks. If the price went down $1 the delta went down and they can sell the change back to the market.

Excellent!!! How does a change in IVol affect these calculations?

I’m still learning so forgive me if my question is overly basic. When the stock price moves wouldn’t delta change so we’re no longer perfectly delta hedged? Does delta actually have a $0 impact or are you implying that the delta at the original point is hedged and the new delta created through gamma is the expense in the gamma column?

Yes, Market Maker will have to re-hedge their position, they can adjust day by day or week by week so long as they're in a comfortable zone of delta

Why do you think the majority of trading is automated? Mm delta hedging. MMs don't take losses, they simply adjust long/short exposure tick by tick to account for their short p/c positions.

Every high p/c environment ends in a short term spike eod while mm cover hedges as contracts close/expire

how can MM hedge against whipsaw movement ? seem like MM can only hedge one direction but when the Underlying reverse creating a whipsaw movement . the MM is out of luck. Or is there a way MM can hedge when the underlying make a u-turn? my best guess is they dumping the shares so they can be delta neutral again? But when will they dump the shares? at what trigger point?

Thank you so much for the visuals and breakdown! I have just started my studies in this area, and was wondering what the difference would be using the binomial pricing model, and could you also please explain the significance to MMs of 1 Delta? From what I have found thus far it appears to be the future price of the underlying. Awesome job, David, and thanks again!

Crystal clear

The Excel spreadsheet with the link provided is not available. Could you help where to download it?

How can can the position delta be zero if the gamma is changing? Gamma affects delta no?

I thought gamma is greatest closest to the money, why is it then the MM delta increase as the stock price moves further from the money??

Another good one David. Thank you.

Thank you for the support!

hi, it says xls in dropbox was deleted... do you have another link? thanks alot. !!!!!!!!!!!!!! liked and subscribed !

So taking this year last few months, with the high volatiliy of tech stocks , is it fair to assume that the MM were probably making loses?

Compensated by Vega?

Do MM always hedge? Or do they keep track of winning and losing traders? I see Unusual options activity all the time but MM hedge only a small percentage of them. Why would that be?

"MM hedge only a small percentage of them" - how do you know this? "Unusual activity" on a particular strike may be partially hedged by the contracts on the other side of the option chain, i.e. puts if the UA is on calls. It is one massive, dynamic system that encompasses many inputs and outputs including the moneyness/delta of the strike. OTM contracts hedged less due to lower delta, etc.

Why interest is divided by 250 but not 365 days a year?

Here to make more sense of the Gamma squeeze on $GME haha

10:30 very cool indeed

If only SellerOptions's James Cordier had seen your video beforehand....

Mitch Richard Cordier had no hedging in his hedge fund.

thank you.

How about dynamic delta hedge, how would loses be with that strategy?

surely 60shares not 0.6 shares - as 1contract is for 100 shares

nope, it's not illustrating a contract, it's just illustrating one option (I don't say contract anywhere). The one option can be scaled by any number

@@bionicturtle i was confused too... Thanks for clearing things up with this comment.

@@bionicturtle That is confusing but makes sense because the price of the call is also for one and not multiplied by 100.

Looks like the spreadsheet has been deleted

How would you be possibly knowing which part of the open interest the MM is short or long? Because without that information you will never know their true exposure

Also there’s a retail investor making a NOPE index to roughly calculate the delta exposure of MM by using Vol times delta and summarizing all strikes with all expirations. Clearly it’s very misleading isn’t?

this is called robbery 😂

Stocks move a lot, so trying to delta hedge sucks basically.

2:05

My smooth ape brain no understand. Need sleep. Come back on a few try again.

Gme anyone ??