I have to do a lecture on this myself as a grad student TA. Taking notes on his organization of the material. I also like the way he effectively utilizes board space which is something I have yet to get the hang of. He is obviously a master lecturer - the kind that made me motivated to study physics in the first place.

If i am not mistaken : Prof used the formula Var(X) = Sum of {each X Squared multiplied by its Probability } minus (Mean of X Squared) . True for all J Here the subscript is J, J could be 1 to what ever but each time probability remains 0.5 and each outcome value always ends up as positive 1 ( after squaring too for the initial -1 X values) , so in total always 0.5 time 1 plus 0.5 times 1 ,adding upto 1 .

if you think that discrete times k_i+1, k_i are not adjacent like 10s, 4s, you may could solve this problem. if k_i+1, k_i is adjacent time, k_i+1-k_i implies 1

@@pavankumarpolisetty872 i think you mean Var(M_i+1 - M_i). Var(M_i+1 - M_i)= , k is increment index in time btw i+1 and i. Obiously X_k^2 =1 for all k and < X_i X_j > = kronekerdelta ij ( because X is iid). so Var(M_i+1 - M_j) is proportinal to time(= number of increments). This is characteristic behavior of brownian motion

@@안또잉-x9f Var(M_{k_{i+1}}-M_{k_{i}})=Var(sum(X_{j}) = sum(Var(X_{j}) (where j runs from k_{i} to k_{i+1}) using the fact variance of sum of independent random variable is just the sum of variances.

Does Brownian Motions predictive power within the financial domain lie in its ability to be scaled continuously? Is there a difference of prediction power between very large and very small time scales?

but is the market has a fair experiment like coin toss , No there're many biases envoles such as Market Regulators (goverments, Central banks ...) economic status , and more other variables leads to a bias in period t and t+n So I guess the modeling of market random walk need to be more accurate . thank you anyway for sharing this knowledge

My Professor actually take his notes from here😹, I’m done going to his class

Once you have found the IIT lecture you have found the source 😄

Please make more videos Professor.

The way you explain theoretical concepts are just amazing.

This man is brilliant ! !Thank You !

I have to do a lecture on this myself as a grad student TA. Taking notes on his organization of the material. I also like the way he effectively utilizes board space which is something I have yet to get the hang of. He is obviously a master lecturer - the kind that made me motivated to study physics in the first place.

phenomenal, this is 10x better my professor

24:05 Quadratic Variation and variance

- Great lecture

- Subtitles are available

10/10

Very good professor.

Bhagwan apko lambi umar de bhai

This is brilliant. Thank You!

17:09 Could anyone explain how he calculated the variance?

If i am not mistaken :

Prof used the formula Var(X) = Sum of {each X Squared multiplied by its Probability } minus (Mean of X Squared) .

True for all J

Here the subscript is J, J could be 1 to what ever but each time probability remains 0.5 and each outcome value always ends up as positive 1 ( after squaring too for the initial -1 X values) , so in total always 0.5 time 1 plus 0.5 times 1 ,adding upto 1 .

if you think that discrete times k_i+1, k_i are not adjacent like 10s, 4s, you may could solve this problem. if k_i+1, k_i is adjacent time, k_i+1-k_i implies 1

@@안또잉-x9f but how it comes to var(K_i+1,K_i) comes to K_i+1-K_i at 17:03 of this video???

@@pavankumarpolisetty872 i think you mean Var(M_i+1 - M_i). Var(M_i+1 - M_i)= , k is increment index in time btw i+1 and i. Obiously X_k^2 =1 for all k and < X_i X_j > = kronekerdelta ij ( because X is iid). so Var(M_i+1 - M_j) is proportinal to time(= number of increments). This is characteristic behavior of brownian motion

@@안또잉-x9f Var(M_{k_{i+1}}-M_{k_{i}})=Var(sum(X_{j}) = sum(Var(X_{j}) (where j runs from k_{i} to k_{i+1}) using the fact variance of sum of independent random variable is just the sum of variances.

These tutorials are so elaborate and easy to understand that I don't want to read those complex books anymore. I'll definitely recommend my peers here

does anyone has the pdf of the notes prof is following ?

THANK YOU PROFESSOR I DONT UNDERSTAND WHY nt is integer

How can I communicate with this man

Thanks it's very nice

We have enough maths, we need something else as humans. May be we need to a random walk as a civilization.😅

He is saying exponential for E . I think it's expectation

He immediately corrected himself though

Excellent sir

Does Brownian Motions predictive power within the financial domain lie in its ability to be scaled continuously? Is there a difference of prediction power between very large and very small time scales?

You are great sir ...

14:40

So its Carthesian.. linear

I disagree 8:44 100%

but is the market has a fair experiment like coin toss , No there're many biases envoles such as Market Regulators (goverments, Central banks ...) economic status , and more other variables leads to a bias in period t and t+n

So I guess the modeling of market random walk need to be more accurate .

thank you anyway for sharing this knowledge

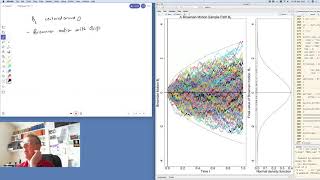

That's a random walk with a drift or a trend. One can model the drift as another mean process

Nice explanation prof

Hall Anthony Thomas Angela Anderson Gary

he is excellent except his looking the notes. yes prof.????

im 12'