- 13

- 124 364

Easynomics

United States

เข้าร่วมเมื่อ 6 เม.ย. 2020

This channel covers content related to Econometrics.

Proof that sample mean is unbiased

In this video we show that the sample mean is an unbiased estimator for the population mean. This is a very simple proof that uses some important properties of the expectation operator.

มุมมอง: 4 586

วีดีโอ

Proof that R squared is 0 if slope b1 is 0 (R2=0 iff b1=0)

มุมมอง 4.8K3 ปีที่แล้ว

In this video we show that the coefficient of determination (R squared) is equal to zero if b1 is equal to zero.

Proof that annihilator matrix M is symmetric

มุมมอง 1.3K4 ปีที่แล้ว

In this video we show that the annihilator matrix M is symmetric.

Omitted variable bias, long and short regression

มุมมอง 5K4 ปีที่แล้ว

In this video we derive the formula for omitted variable bias and the relationship between the short regression and the long regression.

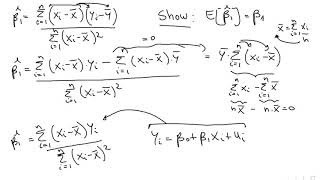

Proof ols estimator is unbiased

มุมมอง 48K4 ปีที่แล้ว

In this video we show that the Ordinary Least Squares estimator for beta 1 (the slope) is unbiased.

Proof that r squared is correlation coefficient squared

มุมมอง 20K4 ปีที่แล้ว

In this video we show the proof that the r squared can be written as the correlation coefficient squared.

Proof that total sum of squares = explained sum of squares plus the sum of squared residuals

มุมมอง 17K4 ปีที่แล้ว

In this video we show the proof that the total sum of squares can be decomposed into the explained sum of squares and sum of squared residuals.

Panel data fixed effects regression within transformation

มุมมอง 2.3K4 ปีที่แล้ว

In this video we show the proof for the within transformation in a fixed effects panel data regression.

Proof of simple Ordinary Least Squares properties

มุมมอง 2.9K4 ปีที่แล้ว

This video shows the proofs for three simple Ordinary Least Squares properties: 1) The sum of the fitted residuals is zero 2) The fitted residuals are uncorrelated to X 3) The fitted residuals are uncorrelated to the predicted Y

Showing that the regression line passes through the mean of X and the mean of Y (EASY PROOF)

มุมมอง 16K4 ปีที่แล้ว

In this video we show that the regression line always passes through the mean of X and the mean of Y.

How to derive the Ordinary Least Squares coefficients EASY

มุมมอง 1.5K4 ปีที่แล้ว

In this video we show how to derive the Ordinary Least Squares coefficients in the sample by solving the corresponding minimization problem.

Setting up the Ordinary Least Squares problem

มุมมอง 2874 ปีที่แล้ว

In this video we set up the Ordinary Least Squares problem and explain the intuition behind it.

How to derive the population regression coefficients (EASY)

มุมมอง 1.3K4 ปีที่แล้ว

In this video, we show how to derive the population regression coefficients in the simple linear regression model.

woolridge book says that R=ey(hat)y. That means ey(hat)y=exy?? why???

RSS/TSS

Thank you very much for this very detailed explanation. It helped a lot in my studies in Econometrics

You made something impossible look easy. thank you!

Incredibly helpful, thank you so much!

Top notch good sir!

i understand the math well enough to get the idea. im studying for a CMA/ management accountant) do i need to add more algebra to my education to be good at my new career?

thanks

why did we get Beta square when taking it out ? coz variance ( a X ) = A^2 variance ( X)

Great video. Cheers!

Thank you!

thank you so much

Thank you so much, bless you

this video literally carried me on one of the questions on my econometrics exam lol

why beta_0 is not a random variable?

Thanks

Thanks so much!!

Awesome explanation. But SSE=(yi-y_hat i)^2 and SSR=(y_hat I - y_bar)^2 and not the other way round.

Var of Beta not Hat possess var of Beta 1 hat .solve this problem plz?

Aoa can u Hepl me in one problem?

Thanks a lot !

Brother can you make a video on derivation of ARMA model, difference equation in time Series Econometrics derivation and it's solutions and numericals also,Ardl Bound test derivation and differential equation in time Series Econometrics derivation.

THANK YOU, I HOPE YOU HAVE A GREAT YEAR

thankyou!!

what was that first order business? I didn't understand that. How it is summing to zero?

If you take the partial derivative of the loss function by vector of errors, you'll see that it equals zero only if the sum of errors is equal to zero too

R^2 = 1 - SSE/SST, not = SSE/SST

Thanks for this lecture. It was very helpful.

Very easily explained

Really good proof!

Very well explained! Thank you.

Does this proof hold for n = 1?

if sum of xi and xbar =0 whats the point of solving everything is zero then........................why care solve anything we can put everything zero as per convience. THIS SOLUTION IS JUST A LIE LOL

man thank god for all the guys like you out here

Thanks for this! It really helped

i still don't get it, can please you explain why Ui hat times Yi hat equal to zero? Thanks

Crazy video, but I am still confused after watching this...

Hi, I have an econometric question, is there a way for me to ask it to you ? Thanks !

thanks!

Explanation is too fast and not clear

Did not understand why (xi -x bar) is not conditional on x... Please help

Easynomics>my lecturer🚶♂️

Damn! You're a lifesaver. You decomposed everything to my understanding. Thanks🙏

Thanks for the nice video! One Question Sir, your first equality, does Var(y-y_hat) =?= Var(y) - Var(y_hat) ? y and y_hat independent?

pleas help me

thank you so much, becuase of you I was able to do my homeworkd

what about the multiple linear regression??

Thanks

Thanks!

Can someone explain me where I went wrong here: If we know that ESS = 0, doesn't that imply that RSS/TSS = 1? And that implies that RSS can not be equal to zero. And the formula for RSS = Sum(Yi - Yi-bar)^2 then Yi can't be equal to Yi-bar. However with the formula for Beta^1 being Beta^1 = Cov(X,Y)/Var(X), and Cov= Sum(Xi - Xi-bar) * (Yi - Yi-bar). And we know that Yi - Yi-bar can not be equal to zero, then under the assumption that Var(X) = 0, the cov(x,y) can not be equal to zero and with that Beta^1 can not be zero either.

THANK YOU SO MUCH YOU HELPED ME WITH MY PROBLEM SET:)) WISH YOU THE BEST